As expected, the Federal Reserve (Fed) cut interest rates last week to take the fed funds rate down to 4.25% (upper bound). Moreover, through the release of the updated dot-plot, the Committee signaled that two more interest rate cuts could be appropriate this year, which would take the fed funds rate down to 3.75% (upper bound). The cut was the first rate reduction since last December and the continuation of the rate-cutting campaign that began last September, which has so far seen an unusual reaction out of the Treasury market.

When the Fed delivered its first 50 basis point rate cut last September, bond markets responded in a way that defied four decades of precedent. Instead of falling as expected, the 10-year Treasury yield surged, creating one of the most counterintuitive market moves in recent memory. The progression was relentless: 45.5 basis points higher after 25 days, 78.6 basis points after 50 days, and 93.7 basis points after 100 days. The 10-year Treasury yield ultimately rose by over 100 basis points from its then September lows.

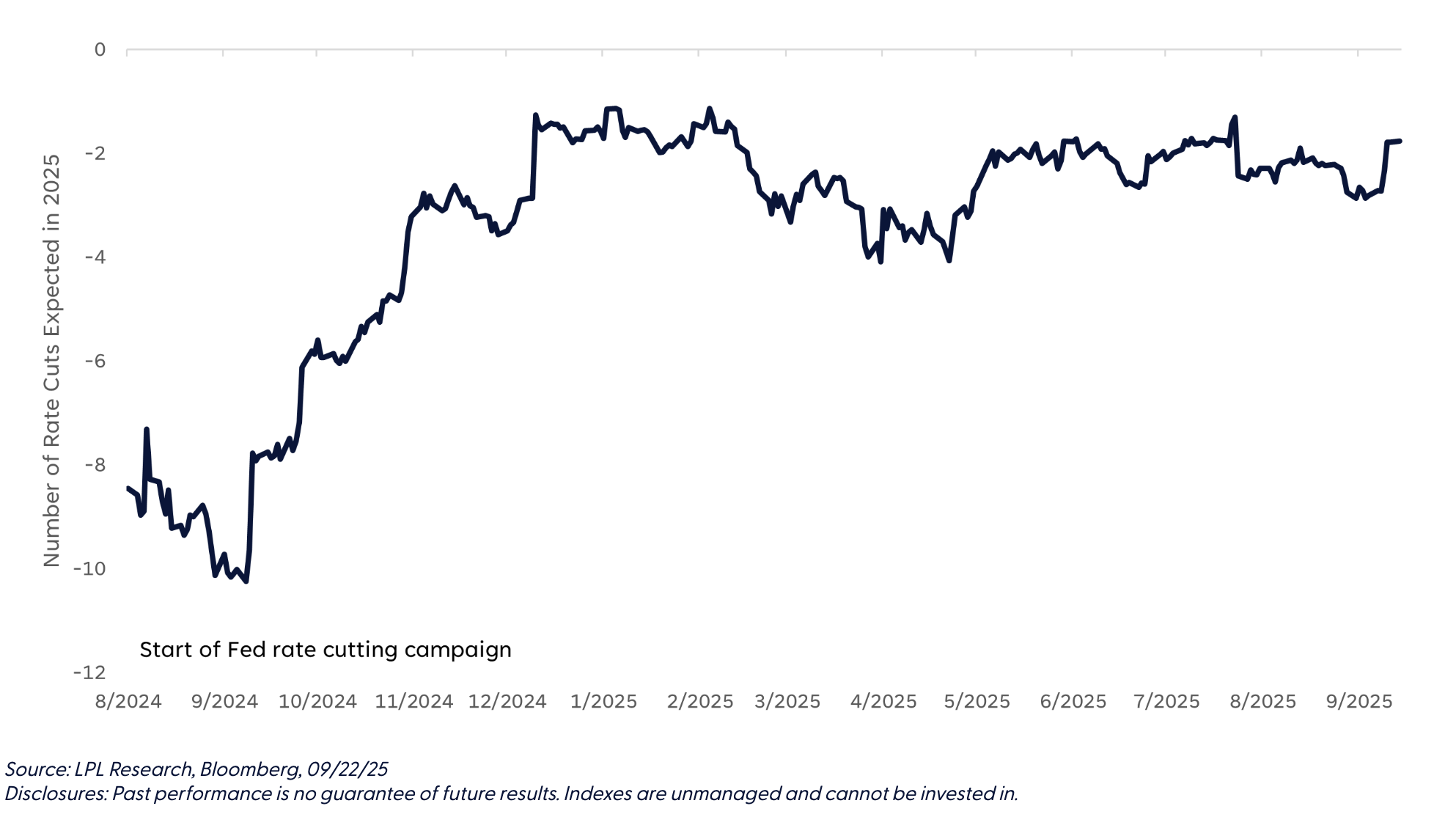

This move was remarkable not just for its magnitude, but for breaking historical patterns. In the previous five Fed cutting cycles dating back to the 1980s, the 10-year Treasury yield declined, on average by nearly 1% within 100 days of the first rate cut. Part of the explanation lies in how aggressively markets had positioned for cuts before the Fed acted. By September 2024, markets had priced in 10 rate cuts before the end of 2025 — a level of easing that proved wildly optimistic. When slowing economic conditions fell short of these extreme expectations, bonds sold off sharply.

Markets Priced In 10 Rate Cuts Before the Fed Cut Once

Why This Time Could Be Different (Or the Same as History)

While the market’s reaction last September was far from ordinary, this most recent rate cut could be less interesting, at least relative to history. Now, markets have priced in, in our view, a more realistic rate-cutting campaign through 2026. Currently, markets have priced in two more rate cuts this year and then roughly 2.5 cuts in 2026. If market expectations are realized, the fed funds rate will end 2026 around 3% (upper bound). Absent a recession and with inflationary pressures still above the Fed’s 2% target, a 3% fed funds rate is much more realistic – albeit on the low end of our expectations – than what was priced in to start the rate-cutting campaign last year. For the fed funds rate to get much lower than what is priced in, the economy would likely need to contract (not our base case), or inflationary pressures would need to fall back to around 2% by year-end 2026 (also not our base case). So, with current market pricing and a 10-year yield trading around 4.15%, we think a 4.0% to 4.5% range is appropriate throughout 2025. In other words, we don’t think we’re in for another historically defying sell off in the rates market post Fed rate cut. No guarantees, of course.

Lawrence Gillum, CFA, guides the fixed income view for LPL Financial Research and has over 20 years of investing experience.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #800290

Read more commentaries by LPL Financial