While markets have been focused on the expected trajectory of short-term interest rates through Federal Reserve (Fed) rate cut expectations, the Fed’s balance sheet has recently come into focus as well. In his speech last week, Fed Chair Jerome Powell signaled the central bank may stop shrinking its balance sheet in the coming months to preserve liquidity in overnight funding markets.

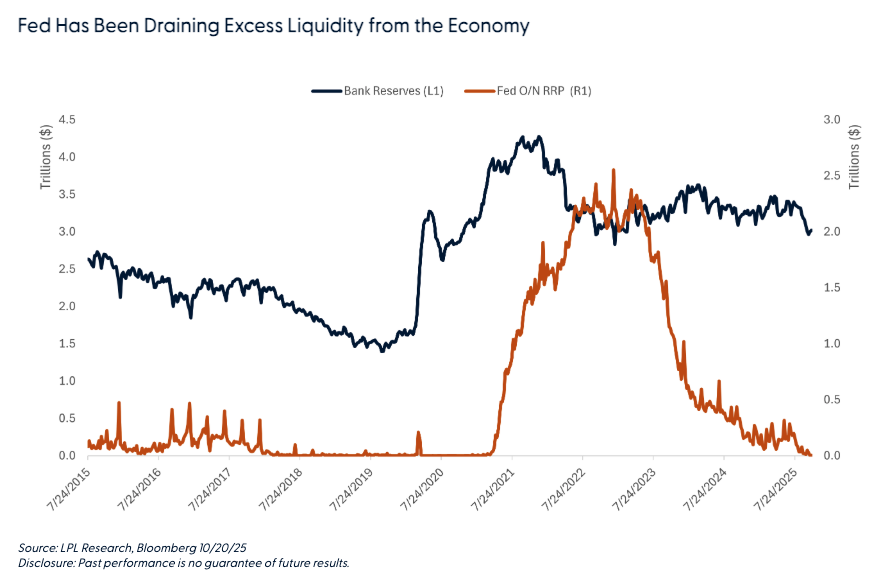

The Fed has been reducing its balance sheet by allowing bonds to mature without replacement in an effort to drain excess liquidity from the economy (colloquially called quantitative tightening, or QT). The Fed has shrunk its balance sheet by over $2 trillion, which has come mostly from a corresponding reduction in the Fed’s overnight reverse repo program (O/N RRP). At $4 billion, O/N RRP is at its lowest level since 2021. The Fed has noted that as that facility approaches $0, the Fed will likely need to reassess its ability to drain excess liquidity from the economy without potentially disrupting short-term funding markets. Moreover, as the O/N RRP drops to $0, further balance sheet runoff will have to come directly from the reduction in bank reserves, which recently fell below $3 trillion.

The challenge for the Fed is that no one is entirely certain when too much liquidity is removed, and you go from an ample reserve environment (which is now) to a scarce reserve environment. The last time the Fed shrunk its balance sheet was in 2019, and they went too far, and repo rates spiked to close to 10%. Reserve requirements are likely higher now, so estimates are that the lowest comfortable level of reserves is in the $2.7–3.0 trillion range, but given the uneven distribution of reserves among banks, that number could be higher.

Related, Fed officials would like the balance sheet to be composed primarily of Treasury securities. Recent comments and data releases suggest that Fed officials would like the share of mortgage-backed securities (MBS) to decline to around 10% of the total portfolio over the next decade. Moreover, all principal payments from MBS securities are being reinvested into Treasury securities, and principal payments from Treasury securities are reinvested into new Treasury securities at auction. When the portfolio resumes growth, reserves management purchases are conducted only in Treasury securities — consistent with the Committee’s intention to return to a portfolio composed primarily of Treasury securities.

However, due to the meaningful increase in mortgage rates and the slow pace of prepayments, the composition of MBS holdings is primarily in longer maturity securities with the largest allocation in MBS bonds that mature in 2051. As such, assuming the Fed wants to meaningfully reduce its MBS holdings, either a) mortgage rates will have to come down dramatically to entice existing homeowners to abandon their low-rate mortgages (mortgage rates tend to price off of the 10-year Treasury yield) or b) the Fed will have to outright sell MBS. There’s been no indication from the Fed that they will sell MBS outright, but it remains a risk to MBS spreads.

The bottom line is that as the O/N RRP gets to $0, short term funding markets could get volatile, which means QT probably doesn’t have many months left. As QT ends, the Fed will go back to buying bonds to maintain excess reserve balances, which on net should be beneficial to fixed income markets.

Lawrence Gillum, CFA, guides the fixed income view for LPL Financial Research and has over 20 years of investing experience.

A message from Advisor Perspectives and VettaFi: Stay ahead of market changes with our daily updates on key market and economic indicators. Visit the AP Charts and Analysis site for our expert insights.