The robotics space is entering earnings season with positive momentum, as solid performance in Q3 has continued into October. This note recaps the key themes and performance drivers from the quarter for investors, while previewing Q3 results. It also reviews new additions to ROBO Global Robotics and Automation Index (ROBO) and their role in the ongoing robotics evolution.

ROBO Q3 Performance Snapshot

ROBO saw +9% performance during the third quarter with eight of the eleven subsectors positive. This quarter saw significant strength and a recovery, with a rebound in traditional as well as burgeoning new markets impacting core ROBO subsectors Manufacturing & Industrial Automation, Logistics and Autonomous Systems.

The latest quarter reinforced one point clearly: the next phase of robotics and automation is being led by companies that combine energy efficiency, physical intelligence, and precision engineering at scale. The robotics economy continues to extend its reach from manufacturing to mobility and from data infrastructure to edge systems and everything making it happen in between.

ROBO’s positioning captures this evolution. The strategy focuses on real-world robotics and automation across manufacturing, logistics, and enabling technologies that power motion, precision, and sensing. These are the systems translating digital intelligence into physical outcomes, and they are now accelerating again after a period of normalization.

-

Manufacturing & Industrial Automation (+21.1%) saw strong performance from Celestica (+57.8%), Teradyne (+49.5%), and Hon Hai Precision (+34.1%) as end-market demand strengthened.

-

Actuation (+12.8%) benefited from exposure to power systems in data centers and global electrification, led by Delta Electronics (+96.4%) and Han’s Laser (+70.0%).

-

Autonomous Systems (+24.8%) continued to expand in size, now representing 6.5% of the index. Joby (+51.7%), Tesla (+39.5%), and XPeng (+29.7%) all delivered robust gains.

- Smaller subsectors such as Food & Agriculture and Healthcare lagged due to tariff pressures and slower policy-driven recoveries.

Q2 Earnings Season in the Rearview & Q3 Expectations

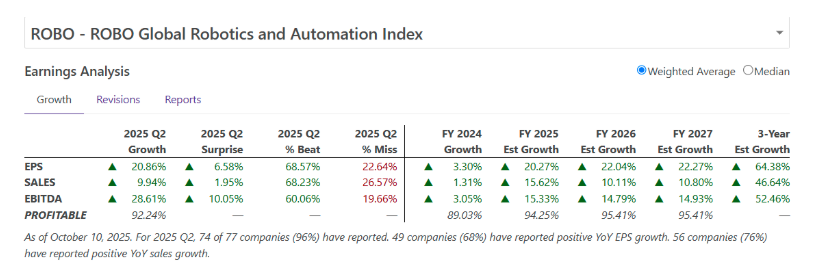

ROBO companies reported sales growth of 9.9% and EPS growth of 20.9% during the prior earnings season.

Tariff concerns that weighed on sentiment earlier in the year have largely translated into accelerated automation investment rather than demand destruction. The impact of tariffs has been minimal compared to original fears. The sector enters the third-quarter earnings period with stronger conviction and improving forward estimates.

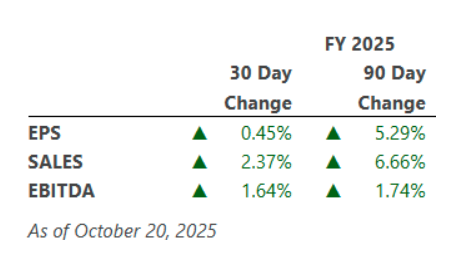

Over the past 30 and 90 days, weighted-average sales and EPS estimates have moved higher across the portfolio, according to FactSet.

New Additions Powering the Next Wave

Every quarter, the ROBO index rebalances based on the research team’s efforts covering the space applied to the index methodology, which scores and evaluates companies across multiple criteria such as thematic revenue purity, market and technical leadership, investments, growth opportunities, and financial strength.

This quarter, Coherent (COHR), Infineon (IFNNY), and UBTECH (UBTA) were added, while ServiceNow (NOW) and Toyota Industries Corp were removed. The goal remains consistent: maintain exposure to the frontier of robotics infrastructure and applications and to the blue-chip pioneers redefining how energy is moved, transformed, and used to power machines efficiently.

Robotics applications are inherently energy-bound and modality-constrained. Systems that improve the efficiency of energy use, whether in data centers, powertrains, or conversion, align closely with ROBO’s core automation theme.

Coherent (COHR): The Photonics Backbone of Automation

Coherent continues to solidify its role as the photonics and laser backbone of automation. Formed from the 2022 merger of II-VI and Coherent, the company combines strengths in compound semiconductors, optics, and laser systems used across manufacturing, communications, and mobility.

-

Networking: About 60% of revenue comes from networking products that power data centers, industrial networks, and next-generation manufacturing systems. Coherent is ramping 1.6T and 3.2T optical transceivers, expanding Indium Phosphide wafer capacity through the world’s first 6-inch line in Texas, and collaborating with NVIDIA (NVDA) on co-packaged optics for high-speed AI, telecom, and factory connectivity.

-

Lasers: Roughly 24% of revenue originates from lasers used in semiconductor, display, medical, and industrial manufacturing. Coherent’s VYPER excimer and industrial laser platforms support cutting, welding, and microfabrication critical to robotics and precision automation.

Coherent provides the connective tissue of the robotics and automation ecosystem through its leadership in photonics, lasers, and materials. Its vertically integrated platform supports the power, data, and precision needs of intelligent manufacturing, industrial connectivity, and electric mobility. It stands as a critical enabler of the ROBO universe.

Infineon Technologies (IFNNY): Powering Intelligent Machines

At roughly $50 billion in market capitalization, Infineon represents a parallel growth story in the physics of power. Robots and AI systems are indifferent to the source of power but depend on its efficiency, transformation, and control. Infineon sits at the center of that equation.

The company is one of the few firms that combines both fab and fabless models, producing gallium-nitride (GaN) and silicon-carbide (SiC) power chips alongside high-voltage transformers used in data centers, automotive platforms, and industrial automation.

Infineon is well positioned to enable multi-modal and multi-form-factor physical automation and intelligence, serving as the foundational power, sensing, and connectivity backbone for autonomous machines, vehicles, and AI-driven edge systems.

-

Automotive (56% of FY2024 revenue): Leadership in vehicle electrification and ADAS.

-

Data centers and connectivity: Rising demand for AI-server power stages and high-efficiency management. The company is transitioning GaN technology to 300 mm wafers, targeting first customer samples in Q4 2025.

-

Automotive Ethernet: Completed the $2.5 billion acquisition of Marvell’s Automotive Ethernet business to support software-defined vehicle architectures.

-

Consumer: XENSIV MEMS microphones and CoolGaN bidirectional switches extend its reach from consumer charging to EV energy infrastructure.

Infineon provides exposure to multiple structural growth areas including electrification, high-efficiency data centers, and industrial automation.

UBTECH Robotics (UBTA): Humanoids Move From Lab to Line

Shenzhen-based UBTECH Robotics develops humanoid and service robots for industrial, commercial, and public-sector use. The company recently secured a $1 billion credit facility to support large-scale deployments in the Middle East and expand global production capacity. UBTECH has seen a strong increase in humanoid robot orders, driven by its Walker S platform’s performance in logistics, hospitality, and inspection settings.

UBTECH brings scalable humanoid robotics, combining full-stack design in mechanics, servos, control systems, and AI software with a vertically integrated manufacturing base. Its platforms are built for repeatable, high-volume production and are moving from prototype to real-world deployment across factories, warehouses, and public environments.

Index Removals

-

ServiceNow (NOW) is facing slower growth and reduced competitive advantage as software automation evolves. ServiceNow had been a ROBO constituent since Q2 2020.

-

Toyota Industries Corp was removed following Toyota Motors’ acquisition confirmation. Toyota Industries had been a constituent r since Q3 2020.

Other Portfolio News:

For more on AI, join our upcoming webcast on November 10 at 11 a.m. ET, “Now & Later: Phases of AI and Its Real-World Applications.” Register here.

Looking for regular updates? Subscribe here for weekly insights on robotics, AI, and healthcare technology, delivered straight to your inbox.

ROBO is the underlying index for the ROBO Global Robotics & Automation ETF (ROBO), the L&G ROBO Global Robotics and Automation UCITS ETF (ROBO.LN), and the Global X ROBO Global Robotics & Automation ETF (ROBO.AU).

VettaFi is the index provider for the ROBO ETFs, for which it receives an index licensing fee. However, the ROBO ETFs are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi and its affiliates have no obligation or liability in connection with the issuance, administration, marketing, or trading of the ROBO ETFs.

For more news information and analysis, visit the Disruptive Technology Content Hub.

Originally published on ETF Trends

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

More Robo Advisors Topics >