Chasing performance by deviating from a benchmark has long been the hallmark of active managers. But it may be time for a rethink. Our research suggests that investors allocating to core equities should consider refreshing the criteria they use to identify portfolio managers that can consistently beat their benchmarks.

Active equity managers continue to face scrutiny. In concentrated markets, it’s become increasingly difficult to outperform because portfolios that diverge too far from index weights in the US mega-caps pay a heavy performance penalty. The mathematics of benchmark risk have raised high hurdles for stockpickers to generate alpha, or risk-adjusted excess returns versus an index. Volatile style rotations have created additional obstacles to reliable returns.

Read more: Five Timely Opportunities in Today’s High-Yield Market

Shifting to passive is the popular solution. But despite the benefits of passive portfolios, we think active strategies still have a role to play in equity allocations. The challenge today is to identify managers that possess real active advantages and can help investors seeking more balanced return patterns through changing environments.

High Tracking Error Is a Red Herring

To do that, the first step is to take a critical look at classic measures of active investing. Tracking error (TE) is first up, because it’s widely seen as a badge of active investing effort. After all, TE is perhaps the easiest way to gauge whether an active manager is really doing their job by working hard on behalf of clients to invest independent of a benchmark.

Technically defined as the standard deviation of excess returns, TE measures a portfolio’s active return minus the return of its benchmark. In other words, it answers the question, “How closely does this fund follow its benchmark?”

The answer to that question is important, because asset owners don’t want to pay active management fees for a portfolio that hugs the benchmark (as many do). Yet although high TE theoretically creates opportunity for outperformance, it doesn’t tell you anything about the portfolio manager’s skill.

An Exercise in Active Manager Selection

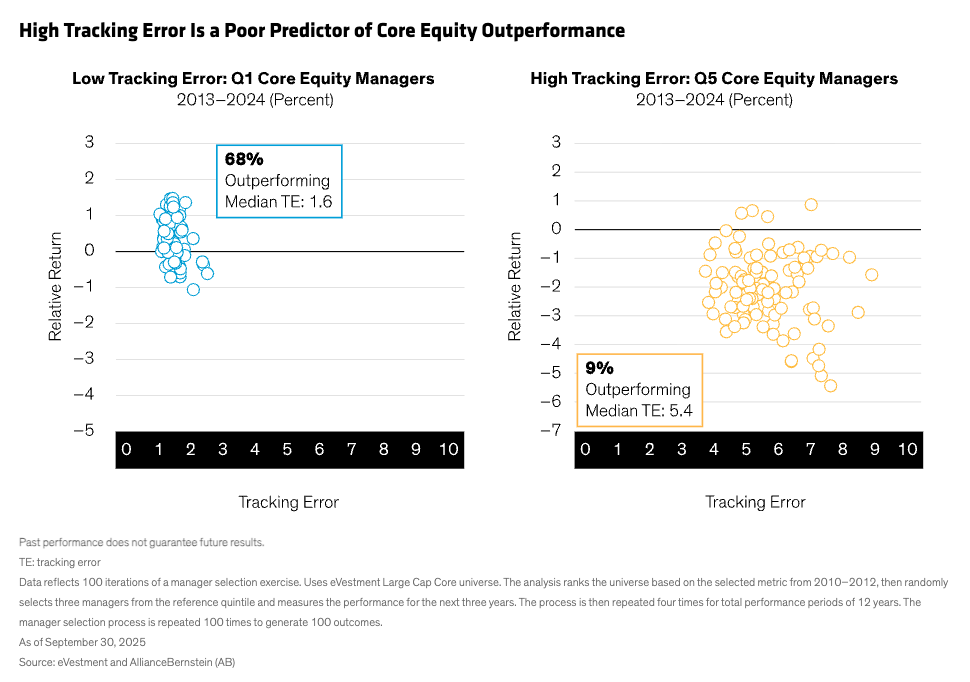

In fact, our research shows that low relative risk managers delivered more consistent excess returns. Starting in 2013, we sorted managers by their TE and looked at their forward three-year relative return. We repeated this process through 2024 to capture 12 years of returns. We then randomly selected core equity managers within different TE quintiles, repeating the process 100 times. In the lowest TE quintile, 68% of managers outperformed (Display). In contrast, only 9% of the highest TE quintile managers beat their benchmarks. While that doesn’t mean every high TE manager is unskilled, it does mean that investors shouldn’t place too much emphasis on TE when choosing a manager.

What about past performance? Every investor is familiar with the disclaimer “past performance does not guarantee future results.” And yet, past performance is typically the first thing asset owners look at when evaluating a portfolio and often has an outsized influence on allocation decisions.

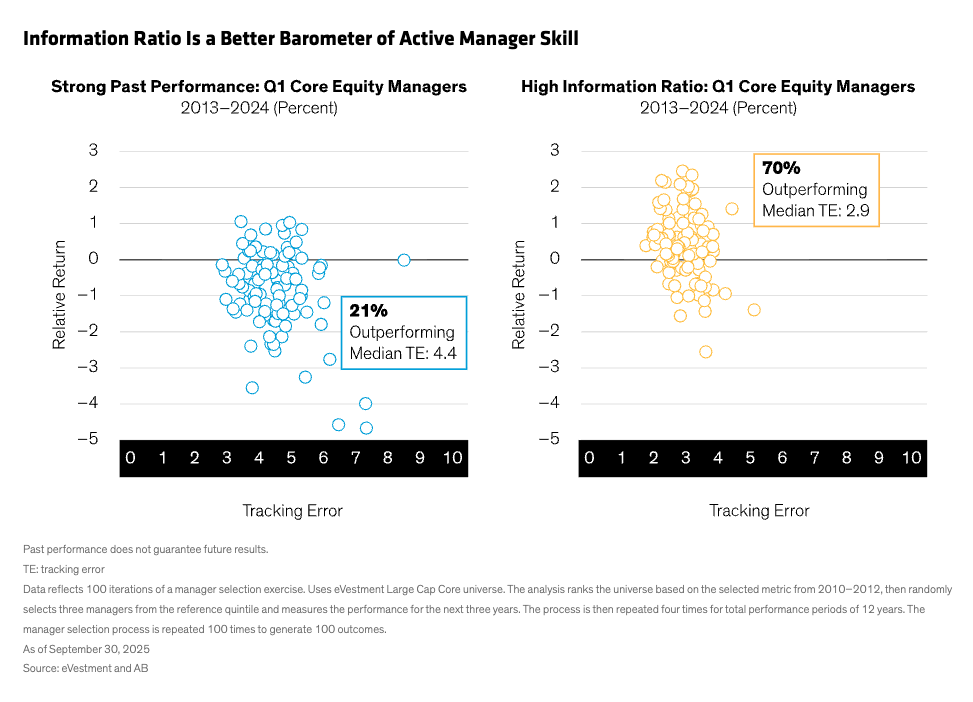

It’s perfectly human to see strong past returns as evidence of skill—but it’s also a perfectly human behavioral mistake. We conducted the same exercise as above, this time looking at how the top performing quintile of core equity managers did over the 12-year period. We found that only a fifth outperformed again—hardly an inspiring result (Display).

Information Ratio Is Much More Informative

So, what’s the best gauge of skill? The information ratio (IR) measures the excess return that a portfolio generates relative to the tracking error. Simply put, the IR tells you how efficient an active manager has been in taking risks. Our research bears that out. We found that 70% of randomly selected, active managers with higher IRs outperformed their benchmarks over the next three-year period.

Of course, when choosing an active manager, much depends on risk tolerance. Investors who have higher tolerance for volatility and seek higher-octane alpha potential might lean into style-driven active portfolios. These strategies can deliver strong results over time, but often with bumps in relative performance along the way. Alternatively, those with a lower risk tolerance may seek strategies that focus on absolute risk, and as a result, Sharpe Ratio, which measures a portfolio’s risk-adjusted performance versus a risk-free asset.

Writing a Recipe for More Reliable Returns

However, for investors with lower risk tolerance who want more consistent alpha from a core allocation, we think the research provides clear direction toward lower TE managers with high IR.

There are different ways to capture consistent return potential. We think the key is to combine broad fundamental research with quantitative tools. Skilled fundamental analysts are great at identifying undervalued securities that can outperform over time. And quantitative controls help manage portfolio risk and neutralize factor tilts. When implemented in a disciplined process, this type of portfolio can deliver moderate but reliable alpha over time.

Translating Active Decisions into Reliable Results

Not all active risk is created equal—and not all investors seek the same outcome. High TE strategies can play an important role for those pursuing differentiated, style-driven alpha.

But for investors who rely on core equity allocations to deliver steadier patterns of excess return, the evidence points in a different direction. Skill is less about how far a portfolio strays from its benchmark, and more about how consistently active decisions translate into results. That places a premium on repeatable approaches that combine deep fundamental insights with disciplined risk management and are designed not just to take risk, but to use it more efficiently.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

More Active Management Topics >