Key takeaways

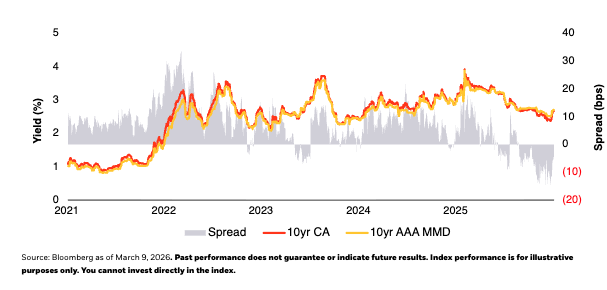

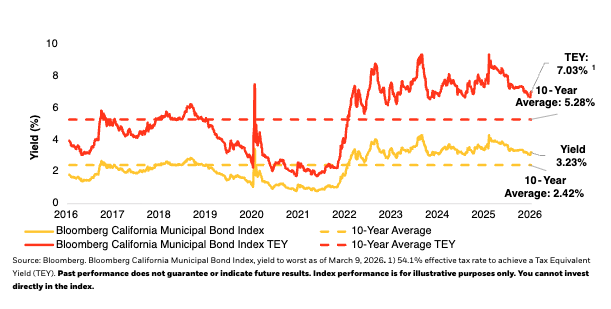

- Municipal bond yields have reset higher, creating compelling value. This is especially true for California residents who stand to benefit most from the municipal tax exemption.

- BlackRock’s Municipal Analyst team continues to highlight distinct opportunities and emerging risks across the California municipal landscape.

-

BlackRock California Municipal products are designed to help investors capture these opportunities while navigating a dynamic market backdrop.

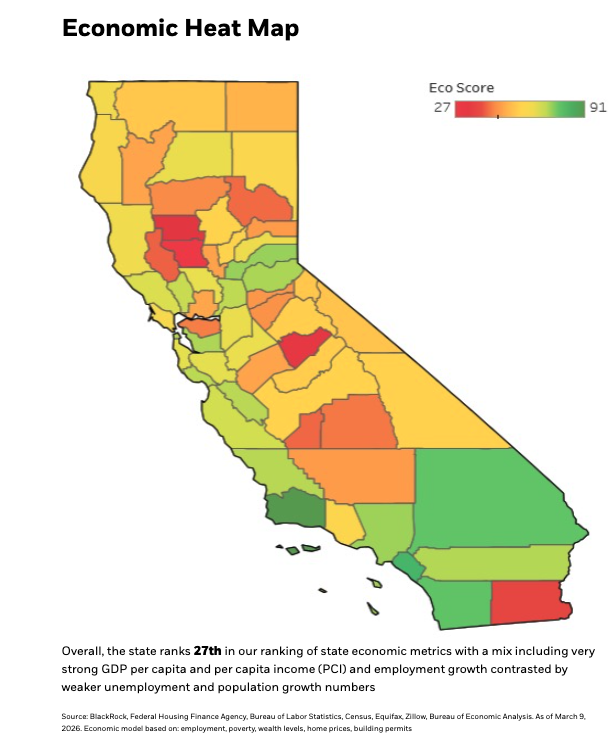

Boom or bust economy

-

California remains the largest state economy in the U.S., now at $4.2T Gross Domestic Product (GDP), retaining its position as the 4th‑largest economy globally.

-

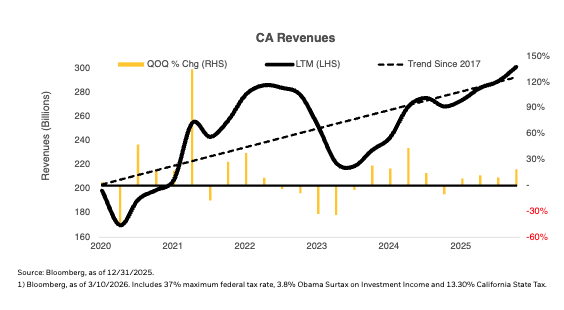

Revenue performance in FY 2025–26 has outpaced expectations, with collections ~8% above forecast, easing the use of reserves.

-

The state's fiscal outlook has stabilized relative to the volatile 2022–23 period but still faces long‑term structural pressures tied to income‑tax reliance.

-

National context: State and local governments across the U.S. saw revenue softness in late 2025, but California benefited from a stronger‑than‑expected rebound in high‑income personal income tax (PIT) receipts.

California continues to demonstrate fiscal resilience, supported by strong liquidity balances and the absence of projected cash‑flow borrowing through FY 2026–27. However, Medicaid cost pressures, a progressive tax structure highly sensitive to equity market swings, and constitutional spending constraints remain key differentiators between California and other large states.

Areas of Opportunity:

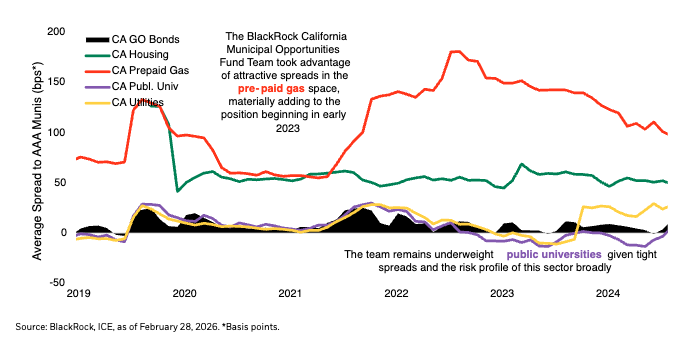

Strong retail demand for California bonds has resulted in tight credit spreads, which traditionally do not reflect the fundamental picture. This means investors are not getting paid for the risk they are taking on by investing in general obligation bonds issued by the state. Instead, the BlackRock Municipal Credit team prefers revenue bonds over tax-backed bonds in the state.

-

Pre-paid energy bonds: Investments across this sector, backed mainly by large banks, offer attractive credit spreads, high yields, and low duration.

-

Sales-tax-supported regional transportation agencies: These credits, such as the Los Angeles County Metropolitan Transportation Authority, continue to show strong margins of debt service coverage protection and conservative use of leverage. In out view, this should make these dedicated-tax bonds a defensive vehicle in the next downturn.

-

Transportation bonds: We prefer large, major transportation assets (airports, bridges, toll roads, seaports) given their prominent position as international gateways to travel and trade.

-

Select California hospitals: We seek entities with proactive, strategic, and disciplined management, a favorable payor mix, solid utilization statistics and scale that can provide leverage in contract negotiations with commercial providers. Given macro pressures around cost inflation, potential changes from Washington and the eventual exchange of commercial reimbursement for Medicare as the population ages, we favor multi-state systems, market leading standalones, and children’s hospitals that have the liquidity cushion to offset these factors.

The state is not without its risks and budgetary complexities. Our goal is to capture value while avoiding the pitfalls that can come with choosing the “wrong” credits. Our dedicated 18-member analyst team remains vigilant in analyzing the risks and opportunities across issuers and credits on behalf of our shareholders to ensure BlackRock portfolios are based on critical thinking and populated with our best ideas.

Active sector rotation creates opportunities

BlackRock Municipal Bond Offerings

- BlackRock offers a variety of solutions to help meet your needs.

- These products include California specific Active & Index ETFs, mutuals funds, and separately managed accounts.

- Invest alongside 40+ years of local municipal expertise, backed by the global reach of one of the world’s largest asset managers.

BlackRock offers a diverse range of actively managed California-specific municipal investment solutions, including the California Municipal Opportunities Fund (MACMX), the iShares Short-Term California Muni Active ETF (CALI), and the MuniHoldings California Quality Fund | MUC. Additionally, investors can find the iShares California Muni Bond ETF (CMF) and customizable separately managed accounts to tailor their California municipal exposure.

For investors seeking to potentially enhance their municipal portfolios with additional high-yield exposure, consider the iShares High Yield Muni Active ETF (HIMU). This active ETF seeks to provide targeted exposure to the municipal high yield market and harvest carry1 through active management.

Historical performance of MACMX

The difference between gross and net expense ratios are due to contractual and/or voluntary waivers, if applicable. Any applicable contractual waiver will be terminable upon 90 days’ notice. BlackRock may agree to voluntarily waive certain fees and expenses, which the adviser may discontinue at any time without notice.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

You should consider the investment objectives, risks, charges and expenses of the fund carefully before investing. The prospectus and, if available, the summary prospectus contain this and other information about the fund and are available, along with information on other BlackRock funds, by calling 800-882-0052 or from your financial professional. The prospectus should be read carefully before investing. Investing involves risks including possible loss of principal.

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities. There may be less information on the financial condition of municipal issuers than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. Some investors may be subject to federal or state income taxes or the Alternative Minimum Tax (AMT). Capital gains distributions, if any, are taxable. A fund's use of derivatives may reduce a fund's returns and/or increase volatility and subject the fund to counterparty risk, which is the risk that the other party in the transaction will not fulfill its contractual obligation. A fund could suffer losses related to its derivative positions because of a possible lack of liquidity in the secondary market and as a result ofunanticipated market movements, which losses are potentially unlimited. There can be no assurance that any fund’s hedging transactions will be effective. A fund concentrating in a single state is subject to greater risk of adverse economic conditions and regulatory changes. The insurance on a bond does not protect against declines in a bonds value. Insurance guarantees are dependent upon financial strength of the insurance company.

Actively managed funds do not seek to replicate the performance of a specified index, may have higher portfolio turnover, and may charge higher fees than index funds due to increased trading and research expenses.

Prepared by BlackRock Investments, LLC, member FINRA.

©2026 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK and iSHARES are trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

© BlackRock

More Municipal Bonds Topics >