Key takeaways

-

Structural shifts vs. cyclical moves: Debt-funded AI capex may ultimately become a secular driver of risk premia, but any such transition is likely to unfold over years – leaving cyclical forces firmly in control of market dynamics in the interim.

-

The recent rise in longer-dated U.S. Treasury yields isn’t really about AI: The back-up in yields since late February reflects shifting policy expectations far more than any meaningful repricing of the term premium tied to AI.

-

Cyclical factors still support the hedging role of bonds: Even against a backdrop of larger deficits and prospective AI-driven borrowing, higher starting yields reinforce bonds’ ability to cushion portfolios and enhance total return potential – especially in a growth slowdown.

-

For now, AI’s footprint is concentrated in hyperscalers’ long-dated spreads: In contrast to the broader non-financial corporate market, spreads on hyperscalers’ long-dated bonds have widened – largely a function of heavier issuance, particularly in the 30-year segment.

AI is a transformative technology with both near-term and long-term implications for the economy. For investors, while the debt-funded AI buildout has the potential to become a secular driver of risk premia, we believe any such shift would only play out through a multi-year adjustment and would not override the cyclical forces that affect markets.

For that reason, the idea that the year-to-date surge in AI-related debt issuance has been a contributor to the recent rise in long-dated U.S. Treasury yields appears overstated. Instead, the move seems driven primarily by shifting policy expectations and a repricing of the Federal Reserve’s expected rate path, not by a meaningful rise in AI-induced term premium or related indigestion about duration (interest rate risk).

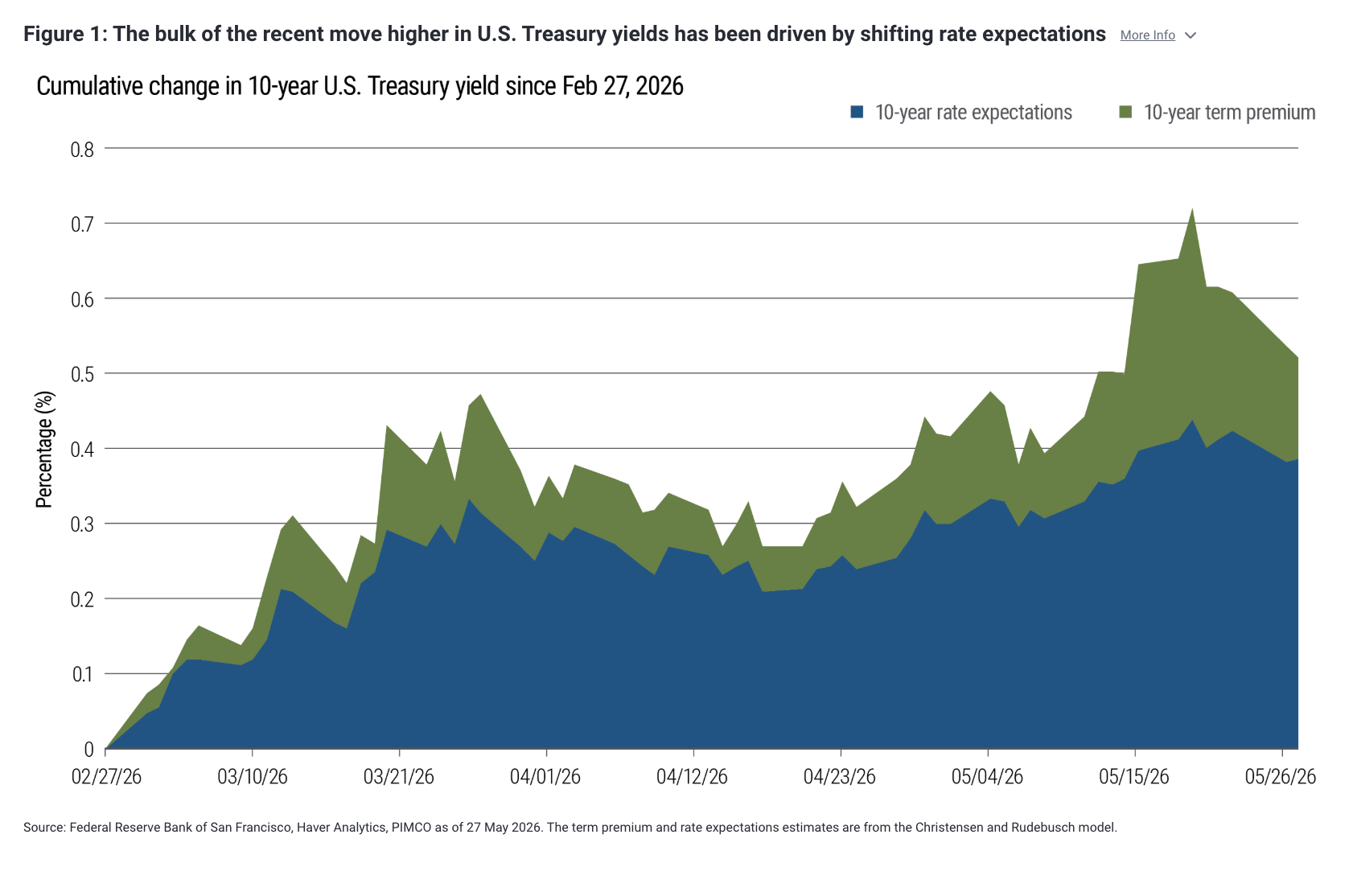

A simple decomposition of the 10-year U.S. Treasury yield move since the start of the Iran conflict makes the point: Most of the increase has come from the rate expectations component rather than the term premium. Since 27 February (the last business day prior to the conflict), 10-year Treasury yields have risen by roughly 51 basis points (bps), of which 38 bps reflects shifting rate expectations and just 13 bps a higher term premium (see Figure 1).

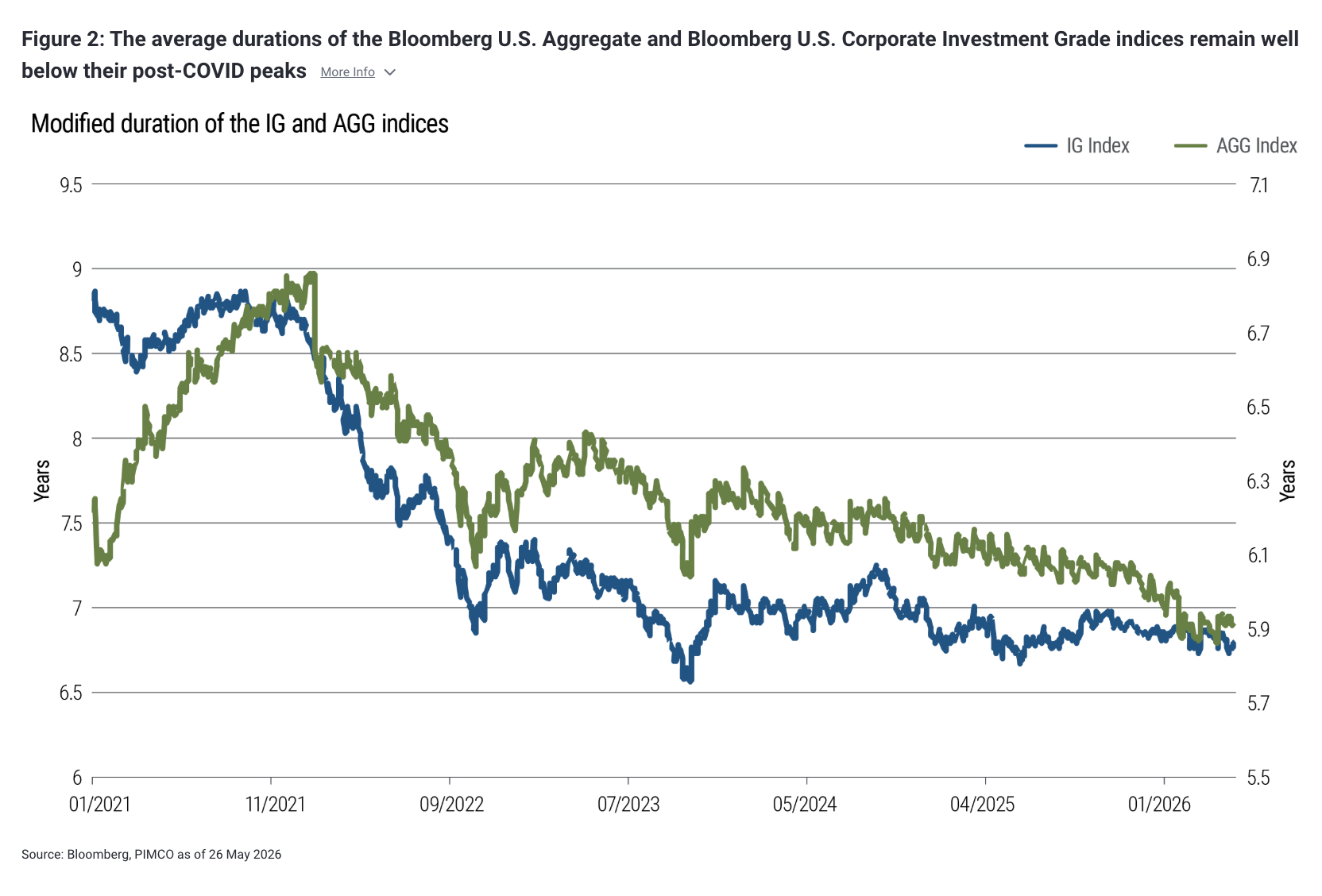

Just as important, the duration supply shock has not fully arrived. Measures such as the average duration of the Bloomberg U.S. Aggregate and Bloomberg U.S. Corporate Investment Grade indices remain well below their post-COVID peaks, suggesting the market has not yet had to absorb the full long-duration footprint that a sustained, debt-funded AI capex cycle could eventually create (see Figure 2). That risk is real, but it is more likely to build as a slow-moving structural pressure than to explain the recent move in yields.

Read more: Supply Shocks and AI-Related Demand Blur Inflation Signals for the Fed

Distinguishing cyclical market behavior from longer-run concerns

By the same token, AI-related credit expansion, wider fiscal deficits, and persistent external imbalances do not mean that U.S. Treasuries have lost their hedging role in multi-asset portfolios.

While the current fiscal math in a recession scenario is not particularly comforting, cyclical market behavior should be distinguished from longer-run concerns. The two can coexist. Questions about fiscal sustainability may persist, but that does not prevent yields from falling when growth contracts or slows sharply. Further, most recessions entail negative demand shocks that widen the output gap and are therefore disinflationary, a positive for duration.

Tactically, the recent reset higher in bond yields is also doing part of the work for investors. Starting yields are materially higher across core fixed income markets, lifting the forward total return profile. If growth does slow or policy expectations reprice lower, that higher starting yield can provide both a cushion and upside optionality. In other words, the setup for fixed income total returns has become more supportive rather than less.

The credit story: Hyperscaler curves steepen, others flatten

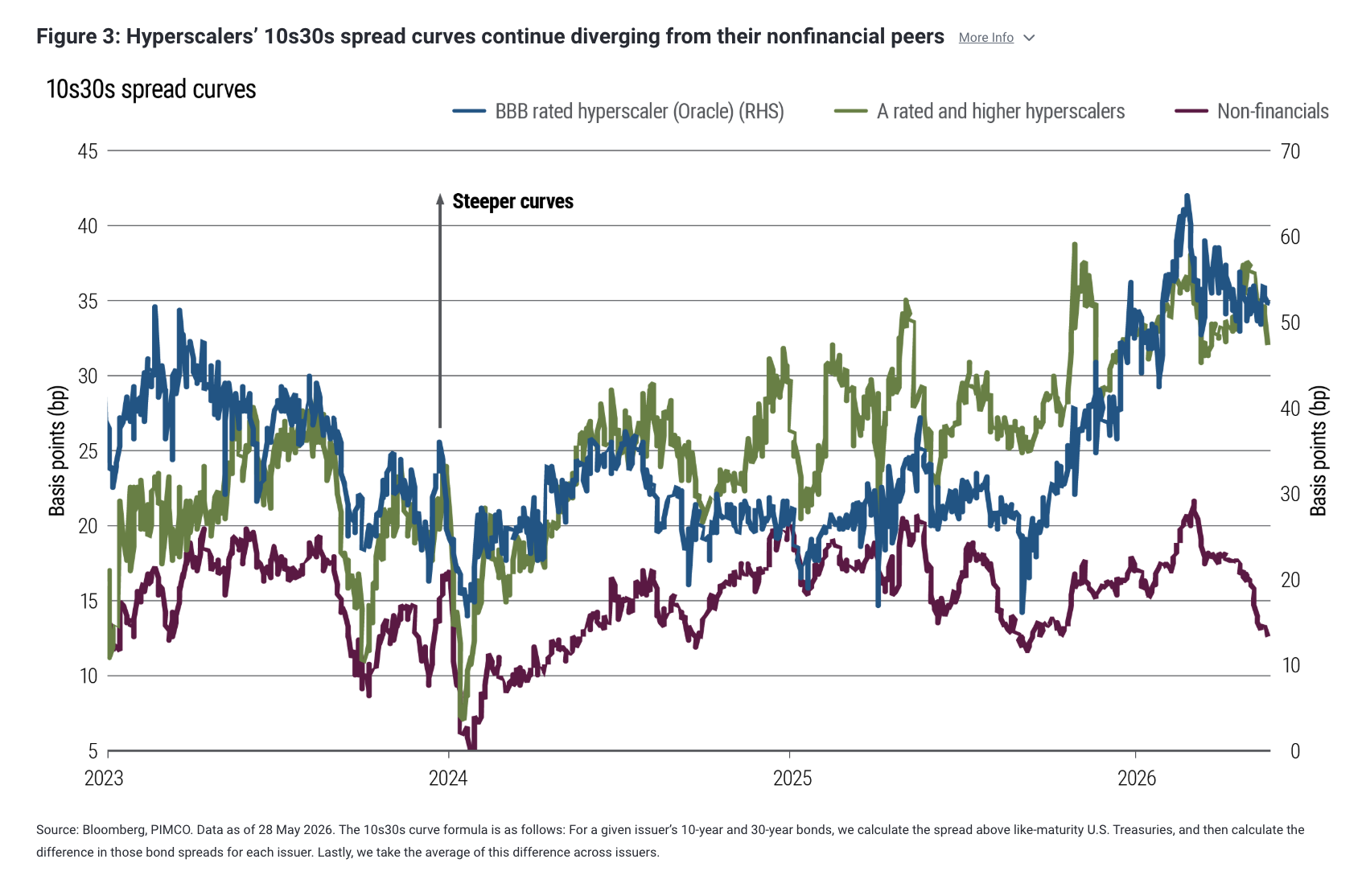

In credit markets, a clear bifurcation has emerged between hyperscaler long-end spread curves and the rest of the nonfinancial universe. (Hyperscalers are the few largest companies providing the cloud computing services that underpin AI, data storage, networking, processing, and other computing.) As Figure 3 shows, nonfinancial 10s30s spread curves have been largely well-behaved, flattening since their local peak at the onset of the Iran conflict at the end of February. The hyperscalers tell the opposite story, with volatile or steepening curves.

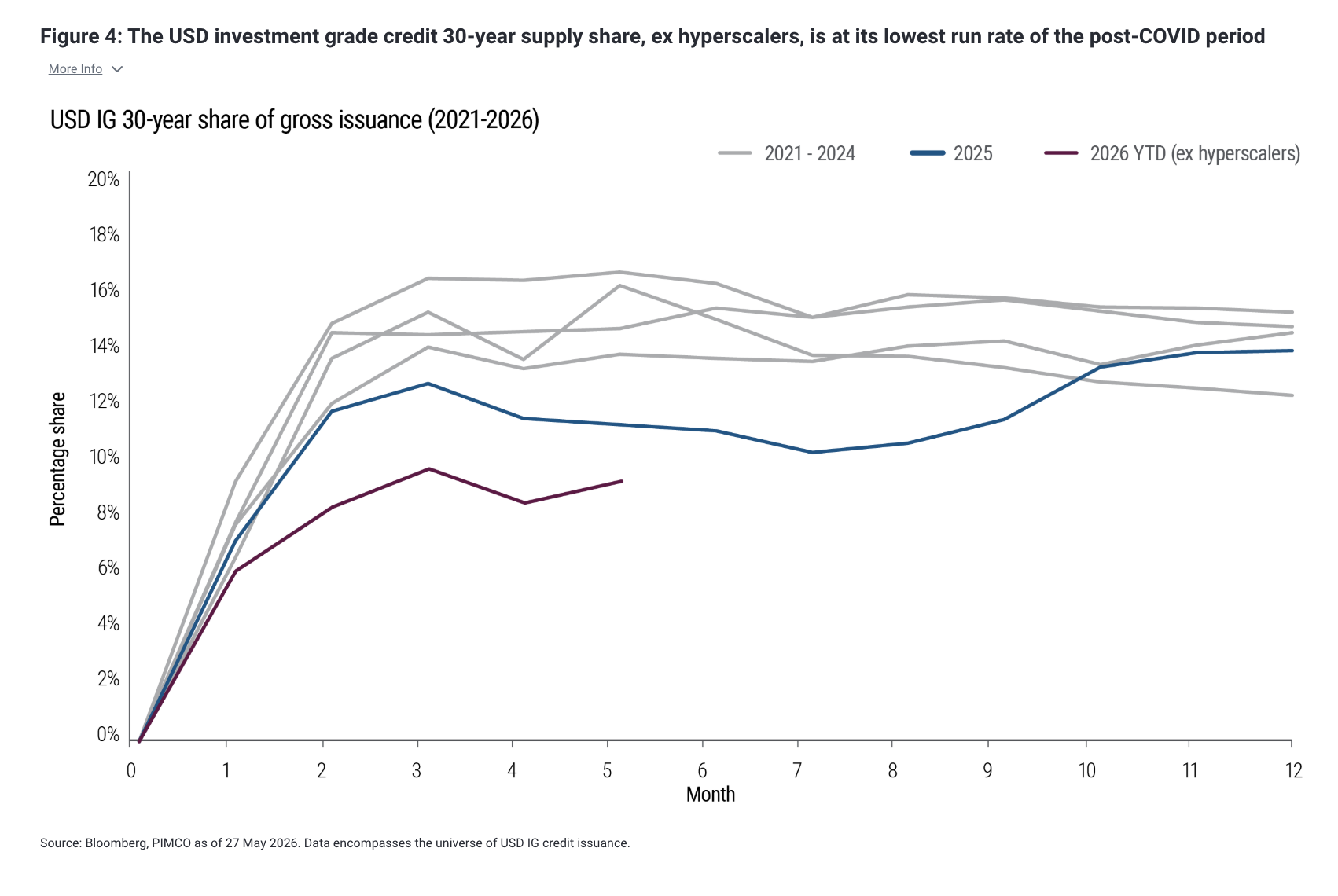

For the broader market, the elevated absolute level of U.S. Treasury yields continues to draw all-in yield buyers into long-dated corporate credit. But there is also a technical tailwind: After stripping out hyperscaler issuance, the gross supply share of U.S.-dollar-denominated (USD) 30-year investment grade (IG) credit is running at its lowest rate in several years – under 10% of overall supply, by our calculations (see Figure 4).

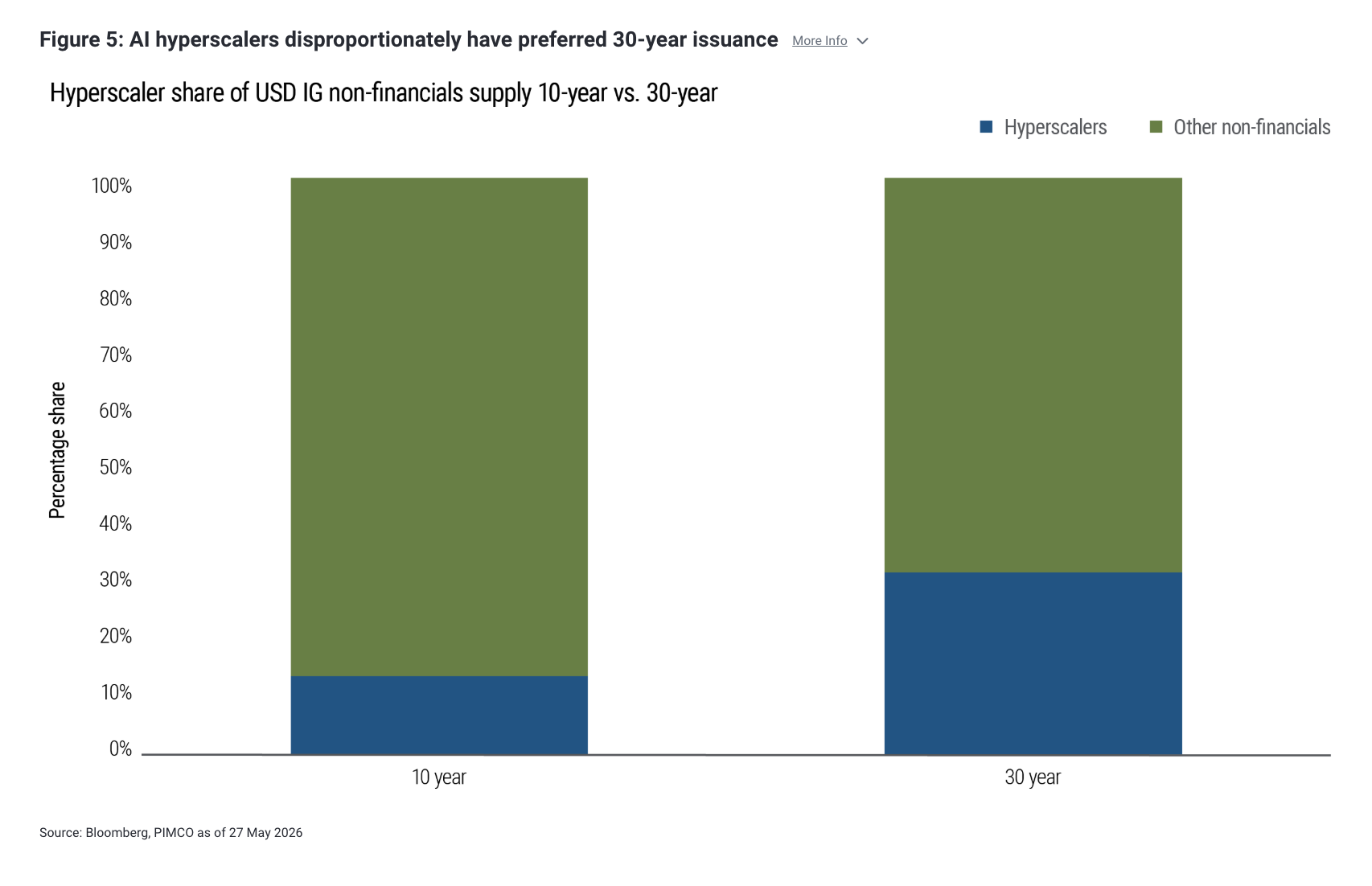

Hyperscalers, by contrast, have shown a strong preference to lock in yields at much longer maturities. Figure 5 shows that while hyperscalers accounted for 13% of year-to-date 10-year supply (approximately $21 billion), they constitute more than 30% of 30-year issuance (approximately $32 billion).

And this isn’t just a phenomenon for USD-denominated debt – it’s been a multi-currency affair. The bond markets denominated in euro (EUR), British pound sterling (GBP), Canadian dollars (CAD), Japanese yen (JPY), and Swiss francs (CHF) have all seen hyperscaler issuance at the 25+ year part of the curve; Alphabet even issued a century bond in GBP in February. While some of these markets are accustomed to longer-dated bonds, for EUR and CHF investors in particular, these maturities are unusual for corporate issuers. We believe they largely reflect a need to diversify across currency benchmarks to mitigate ticker concentration risk within investor portfolios.

The takeaway is straightforward: The steepening in hyperscalers’ long-end slopes is a direct reflection of investors demanding more risk premium exactly where issuance has been heaviest.

Disclosures

Past performance is not a guarantee or a reliable indicator of future results. Statements concerning financial market trends are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

Charts are provided for illustrative purposes and are not indicative of the past or future performance of any PIMCO product. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. It is not possible to invest directly in an unmanaged index.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Certain U.S. government securities are backed by the full faith of the government. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. The current regulatory climate is uncertain and rapidly evolving, and future developments could adversely affect the technology and AI sector.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0529-5535851

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

More Global Markets Topics >