Labor market fundamentals have improved meaningfully from last year’s near standstill while inflation has moved higher, driven in part by the Iran conflict and the resulting increase in petroleum and gasoline prices. As a result, Federal Reserve (Fed) officials are likely becoming more concerned about the risk of broader inflation pressures, a theme highlighted in this week’s ISM Manufacturing and Services PMI releases.

In addition, the administration’s plan to impose a new round of tariffs on 60 countries could further complicate the outlook for lower rates, as it may add to inflation pressures.

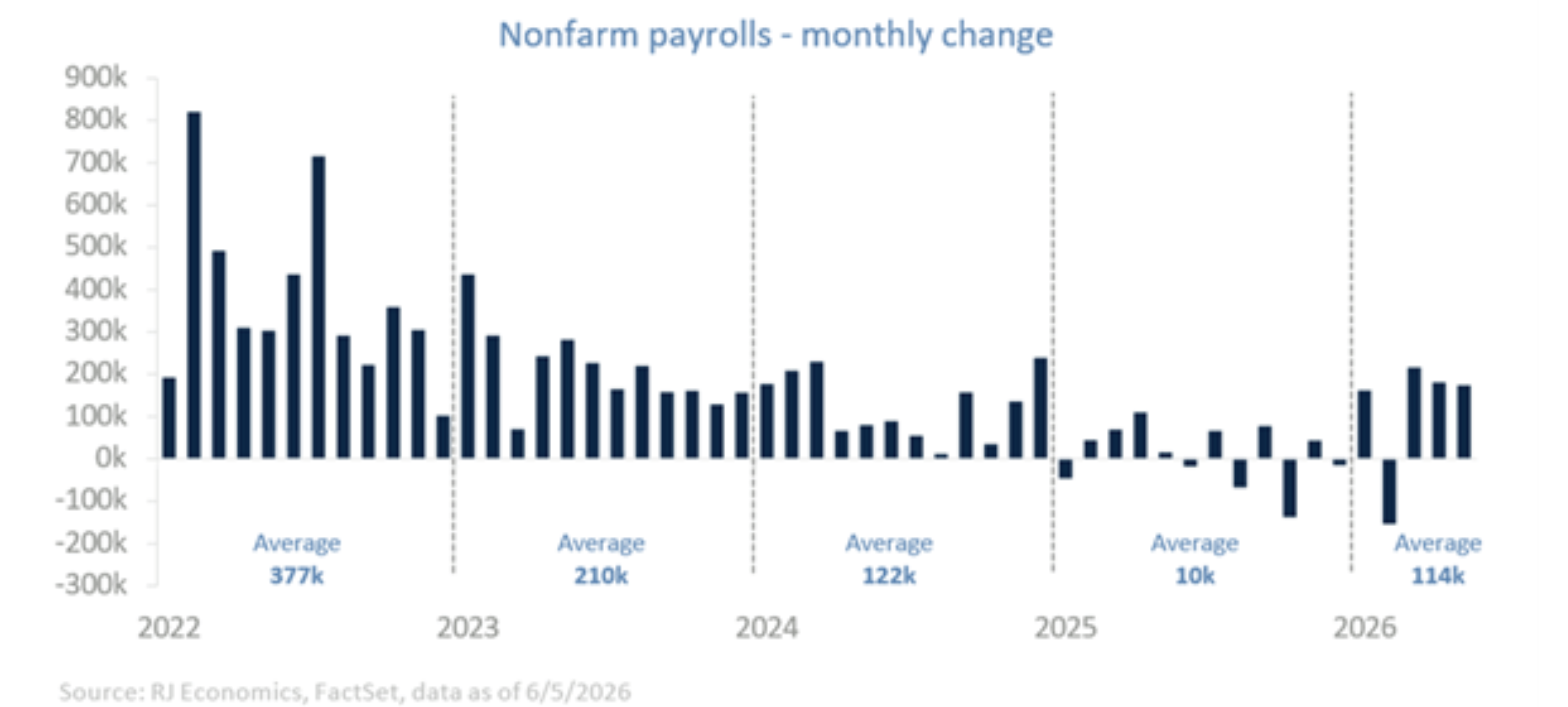

Job growth continues to reinforce this shift. Nonfarm payrolls have risen by an average of 113,800 per month so far this year, a sharp improvement from just 10,000 per month in 2025. Under normal circumstances, this pace of job creation would be expected to push the unemployment rate meaningfully lower, especially given recent research suggesting that the breakeven level of employment growth needed to keep the unemployment rate steady has declined significantly.

Some of this research, including one from the Fed, indicates that “Labor force growth has slowed significantly in the past two years and could be near-zero this year.”

The implications of this are several: “(1) Breakeven employment growth would also be near-zero, such that, if the unemployment rate is relatively constant, then negative job growth would be almost as likely as positive job growth in any given month. (2) Any growth in potential GDP will need to come entirely from labor productivity growth.” ¹ Other estimates place breakeven job growth in a range of 20,000 to 60,000 per month.

Read more: Five Ways Today’s Market Cycle Differs From the Dot-Com Era

However, despite job growth exceeding these levels, the unemployment rate has remained largely unchanged. This suggests that underlying labor supply dynamics may be shifting. One possibility is that the labor force is still growing at a modest pace, potentially supported by adjustments to immigration policy that are helping ease labor shortages in certain sectors. If so, stronger employment gains could be absorbed without a reduction in the unemployment rate.

Another possibility is that higher participation is bringing more workers back into the labor force, offsetting job gains. However, this does not appear to be the case, as the labor force participation rate has been declining since January.

Bottom line

Taking all of this into account, we are removing the final rate cut we previously expected later this year. With inflation moving higher and the labor market improving considerably, the Federal Reserve is unlikely to ease policy in 2026.

We continue to expect one rate cut next year, reflecting our view that economic growth and fiscal support will slow, and that inflation will gradually moderate assuming no additional shock.

1FEDS Notes, “Labor force growth, breakeven employment, and potential GDP growth,” by Seth Murray and Ivan Vidangos, April 02, 2026. Board of Governors of the Federal Reserve System. https://www.federalreserve.gov/econres/notes/feds-notes/labor-force-growth-breakeven-employment-and-potential-gdp-growth-20260402.html

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

Raymond James & Associates, Inc., member New York Stock Exchange / SIPC, and Raymond James Financial Services, Inc., member FINRA / SIPC, are subsidiaries of Raymond James Financial, Inc.

Raymond James® and Raymond James Financial® and power of personal® are registered trademarks of Raymond James Financial, Inc.

Raymond James & Associates Statement of Financial Condition – March 2026 (PDF)

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Raymond James

Read more commentaries by Raymond James