Market adjustments and yields: Fixed income markets have absorbed significant geopolitical and economic developments in recent months, particularly since the escalation of the Iran conflict. Treasury yields have risen sharply, reflecting a combination of higher growth expectations, elevated term premia, and a notable repricing of monetary policy.

Inflation and economic resilience: Yet this adjustment has occurred without a breakout in long-term inflation expectations or a collapse in economic data. This dynamic suggests that a substantial portion of potential bad news — higher-for-longer rates, persistent but contained inflation pressures, and geopolitical risk — may already be embedded in current pricing.

Fed policy and duration outlook: Investors appear to have recalibrated their views on the terminal rate for this cycle and the neutral fed funds rate, moving closer to more hawkish Federal Open Market Committee (FOMC) members’ perspectives. At the same time, stable inflation expectations give the Federal Reserve (Fed) the flexibility to remain on hold rather than react preemptively. This environment supports a cautious — but not outright bearish — outlook for duration, with yields likely past peak levels.

Recent Yield Movements Amid Geopolitical Tensions

Since the onset of the Iran conflict (through last Friday’s close), the U.S. Treasury curve has experienced a meaningful bear flattening with front end yields rising more than back-end yields. The 10-year Treasury yield has increased by approximately 60 basis points (bps), while the 2-year yield has risen by 77 bps. These moves represent a swift repricing that incorporates several factors: rising inflation expectations tied to energy price volatility, an increase in compensation demanded for uncertainty (known as term premia); and a fundamental reassessment of the path for short-term policy rates.

That the increase in yields is not solely a function of inflation fears is important (as discussed later). Market participants have also layered in expectations for stronger real growth in the near term, possibly supported by ongoing investment in the artificial intelligence buildout. Simultaneously, geopolitical risks and fiscal concerns have contributed to higher term premia, reminding investors that rate volatility could remain elevated.

Importantly, these yield increases have been orderly. Despite the geopolitical catalyst, liquidity in core fixed income markets has held up, with no evidence of acute stress in funding markets or forced selling. This resilience underscores that the market is processing information in a measured and efficient way.

Read more: Tariffs Re-Enter the Spotlight

To Hike, or Not to Hike, That is the Question

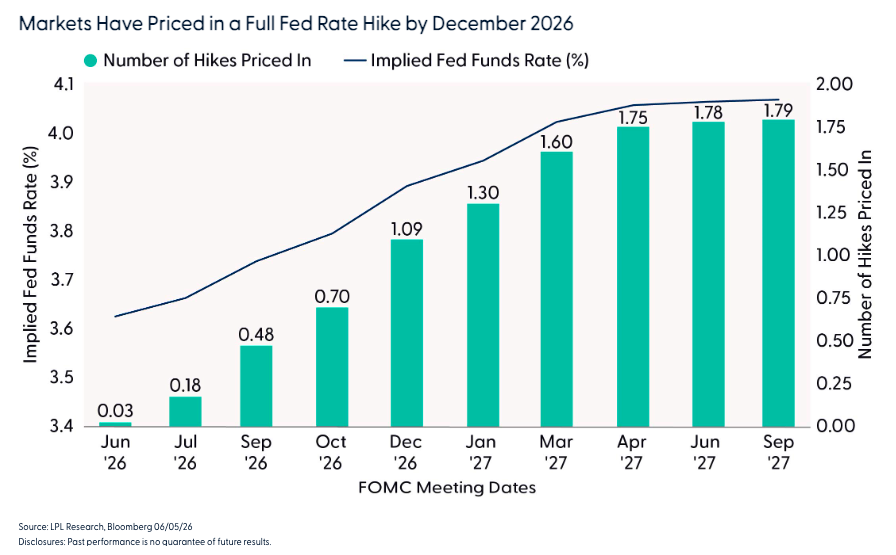

One of the most striking developments has been the rapid shift in expectations for Fed policy. After last Friday’s stronger than expected jobs report, markets are now pricing in roughly a 100% probability of a rate hike sometime this year, with a 67% chance of two hikes by June 2027. This marks a sharp reversal from earlier in 2026, when investors were expecting multiple rate cuts.

The implied neutral fed funds rate has been revised higher to around 4%, bringing market pricing closer in line with more hawkish FOMC member views than with the previous median expectation. Even Fed Governor Chris Waller, often viewed as a relative dove, has publicly acknowledged that a rate hike may be warranted under certain conditions. This signals that the Fed’s policy optionality is flexible: policymakers retain the ability to hike if data warrant it, but it is not compelled to do so unless the inflation outlook deteriorates.

This repricing reflects a maturation of market thinking. Rather than assuming the post-pandemic cycle would mirror previous easing cycles with a low neutral rate, investors now appear to accept a structurally higher rate environment. Resilient labor markets, sticky services inflation, and recognition that productivity gains or demographic shifts may have modestly increased the long-term equilibrium real rate support this view. That said, we’re still of the view that the Fed can potentially cut rates once this year (likely December), but this certainly depends on the depth and duration of the Iran conflict/oil prices, which remain the biggest challenge to cuts. We don’t agree with market pricing suggesting a hike is likely this year as the bar for a hike is much higher than a Fed on hold for an extended period of time. So, with Fed officials generally more hawkish, the question becomes have they increased their hawkish rhetoric to help tighten financial conditions (aimed at staving off a hike) or is there a real chance the next move could be a rate hike? Time will tell, but the Fed arguably isn’t behind the curve, as in 2022.

The Fed Can Be Patient…For Now

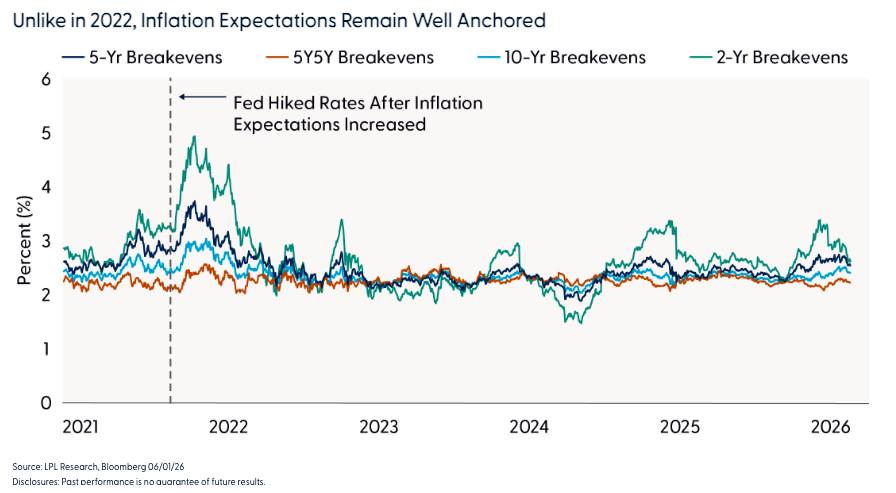

Despite the front-end repricing and near-term inflation risks from energy markets, long-run inflation expectations remain well anchored. This is a critical distinction: near-term inflation pressures from geopolitical events are being viewed as transitory, while structural price stability expectations remain firm.

This anchoring is a key reason why the Fed can remain patient. Unlike the 2022 experience, when the central bank was clearly behind the curve and inflation expectations were rising alongside actual inflation, markets today appear prepared to “look through” temporary price spikes. For example, breakevens have moved modestly higher but remain consistent with modest overshoots of the Fed’s 2% target rather than a sustained shift higher. Forward inflation swaps and longer-dated breakevens reinforce this view.

The Fed’s credibility, rebuilt through its aggressive tightening in 2022–2023 and subsequent data-dependent approach, provides a buffer. As long as expectations stay anchored, the bar for an actual rate hike remains relatively high, even if markets are pricing in some probability of one — reducing worst-case-scenario risks and supporting the case that much of the bad news on inflation is likely already priced in (absent a reacceleration in oil prices).

Higher Yields: A Mix of Inflation and Real Growth Expectations

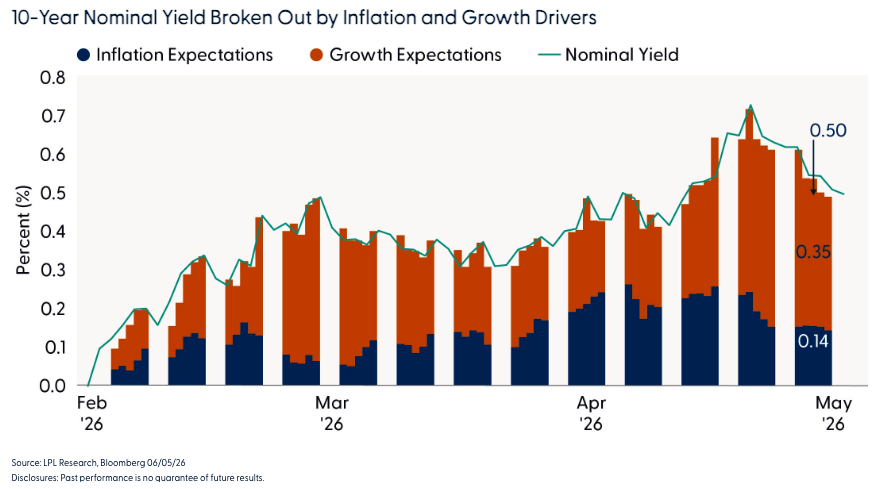

Nominal Treasury yields can be decomposed into components reflecting real growth expectations and inflation compensation. Analyzing the move in the 10-year yield since the start of the Iran conflict shows that the majority of the increase (approximately 35 bps) stems from rising growth expectations, with a smaller portion (only about 14 bps) tied to higher inflation expectations.

This is an important distinction. The growth-driven component suggests markets are pricing in a “soft landing plus” scenario or at least continued economic resilience rather than outright stagflation. Higher real rates reflect confidence in growth, likely supported by productivity or fiscal stimulus effects.

Consequently, even if oil prices decline after geopolitical uncertainty eases, any meaningful drop in the 10-year yield may be limited unless economic data warrants a deeper than expected rate-cutting cycle. Yields have risen on the back of better-than-feared growth, not runaway inflation — a distinction that matters for the trajectory of rate volatility going forward.

Resilient Data, Steady Demand

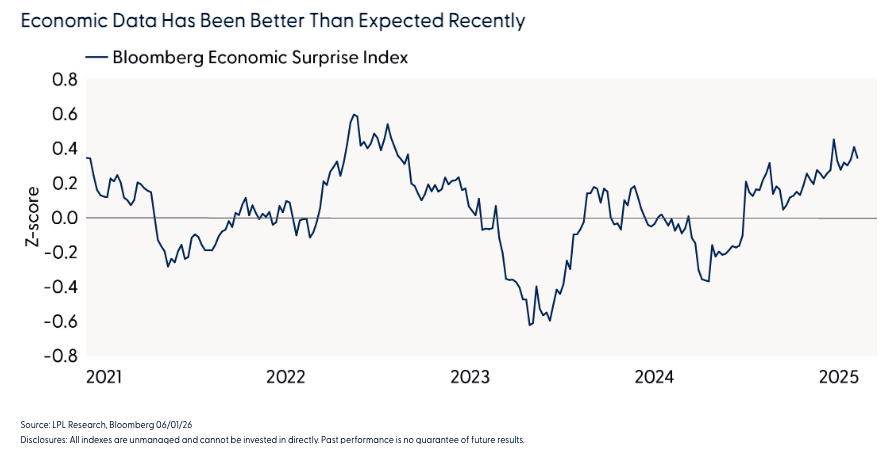

Recent macroeconomic data and Treasury auctions reinforce the view that markets have absorbed bad news well. Incoming data has generally surprised to the upside (per the Bloomberg Economic Surprise Index), demonstrating economic momentum that has exceeded consensus expectations in several areas, helping keep the broader narrative of resilience intact.

Also, recent auctions of 2-year, 5-year, and 7-year Treasuries, totaling $183 billion, were met with adequate demand. While not exceptionally strong, they were far from weak. Foreign participation and domestic investor interest proved sufficient to absorb supply without pushing yields significantly higher intra-auction. This suggests that investors are reasonably comfortable with prevailing yield levels. In combination, both factors underpin the case that current yields reflect a balanced assessment of risks rather than panic pricing. This week’s $119 billion (total) in Treasury auctions of 3-year, 10-year, and 30-year Treasury securities will provide another real time test to determine if yields are sufficient to attract necessary demand.

Conclusion

The Treasury market has priced in a potential rate hike, reset the neutral rate higher, and built in a meaningful term premium — all while long-run inflation expectations remain anchored and macroeconomic data have held up. A substantial amount of bad news appears to already be reflected in prices. Absent a resurgence in oil prices or a sharp acceleration in growth, the recent surge in yields is likely behind us, although longer-maturity Treasury yields should remain elevated near current levels in the near term, in our view.

In summary, fixed income markets have demonstrated remarkable efficiency in incorporating geopolitical shocks and policy repricing. With much of the adjustment likely already behind us, the risk-reward profile for core Treasuries appears more balanced than headline yield moves might suggest.

Asset Allocation Insights

LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) maintains a neutral stance on duration relative to benchmarks. Our proprietary duration models show mixed signals, pointing toward neutral positioning, which strikes the appropriate balance. We would reconsider and potentially add duration if the 10-year yield were to push into the 4.75–5.00% range or if the curve steepened materially from current levels, which would represent an attractive entry point given the anchored expectations backdrop.

The STAAC maintains its recommendation for a tactical equity overweight and fixed income underweight. This reflects an expectation of further easing of geopolitical and commodity supply concerns as a result of the U.S.-Iran conflict, alongside a more cautious outlook for select areas of core fixed income. Overall, our tactical views emphasize a modest equity overweight expressed via a defensive factor tilt, a continued focus on quality bond sectors, caution in rate‑sensitive fixed income sectors, and an ongoing allocation to diversifying strategies and alternatives. Within fixed income sectors, we remain underweight investment grade corporates and mortgage-backed securities (MBS) as spreads remain tight relative to historical standards, diminishing the risk/reward profile of the sectors.

Lawrence Gillum, Chief Fixed Income Strategist, LPL Financial

Brian Booe, Associate Analyst, Research, LPL Financial

Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All investing involves risk, including possible loss of principal.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

The Bloomberg U.S. Economic Surprise Index measures the degree to which U.S. economic data releases surprise to the upside or downside relative to market expectations.

All index data from FactSet or Bloomberg.

This research material has been prepared by LPL Financial LLC.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by LPL Financial