A growing share of central bankers argue that artificial intelligence will ultimately push neutral interest rates higher. Intuitively, if AI boosts productivity and lifts long-run growth, then households have less incentive to save, pushing up the real neutral rate. This view has become increasingly embedded in policy discussions, with some observers pointing to the late 1990s when higher productivity growth coincided with rising estimates of the neutral rate.

This is a crucial discussion for monetary policy, as the real neutral rate – though theoretical and unobservable – often serves as a guidepost: It’s the rate that neither stifles nor stimulates economic growth. Economists call it r* or r-star.

However, existing empirical evidence offers little support for the popular narrative around AI. Rather than rising, long-dated real and nominal yields have tended to fall around major AI-related news. Looking specifically at market reactions to large AI model releases since 2023, the cumulative change in forward rates suggests that investors are revising neutral rate expectations down, not up. Even if one is skeptical of event-based analysis, it is notable that there is no consistent evidence that rates have risen in response to AI developments.

Read more: Can AI Deliver Lasting Growth?

The neutral rate and the five-year, five-year-forward

As mentioned above, the real neutral rate is a focus for central bankers because it sets a useful marker as to whether the policy rate is restricting the economy or accelerating it. A widely used definition of r* is the real short-term interest rate that would prevail when the economy is at full employment and inflation is stable. By definition, it’s a long-run concept, and it abstracts from temporary shocks when the central bank might need to adjust its actual policy above or below neutral.

Because r* tends to evolve along with slow-moving structural economic forces – including demographics, productivity, and savings/investment trends – central banks must understand not only cyclical economic dynamics, but also how r* evolves to effectively set policy. The issue is that because r* is unobservable, it must be estimated, and its estimates are subject to a lot of uncertainty.

One way to proxy (rather than estimate) r* is to use market-implied rates. Specifically, the 5-year, 5-year-forward rate (5y5y) is a useful proxy because it’s the market-implied rate expected to prevail once short-term cyclical effects have faded. The 5y5y forward embeds investor expectations of the average overnight rate in the far future, plus a term premium (compensation for the risk of locking in a fixed payment in the future as opposed to investing in a short-dated bond and continuously rolling at maturity).

Event studies looking at changes in 5y5y forward real and nominal rates offer a useful benchmark for how the market responds to releases of new AI models. Since expectations for these models tend to be priced in advance, the market reaction on the release date reflects how well the new model exceeded or fell short of those expectations.

AI: a source of productivity and uncertainty

Event studies that measure changes in forward rates around significant model releases suggest that, rather than rising – as would be consistent with market expectations of AI contributing to higher r* – long-dated real and nominal yields have tended to fall around major AI-related news.

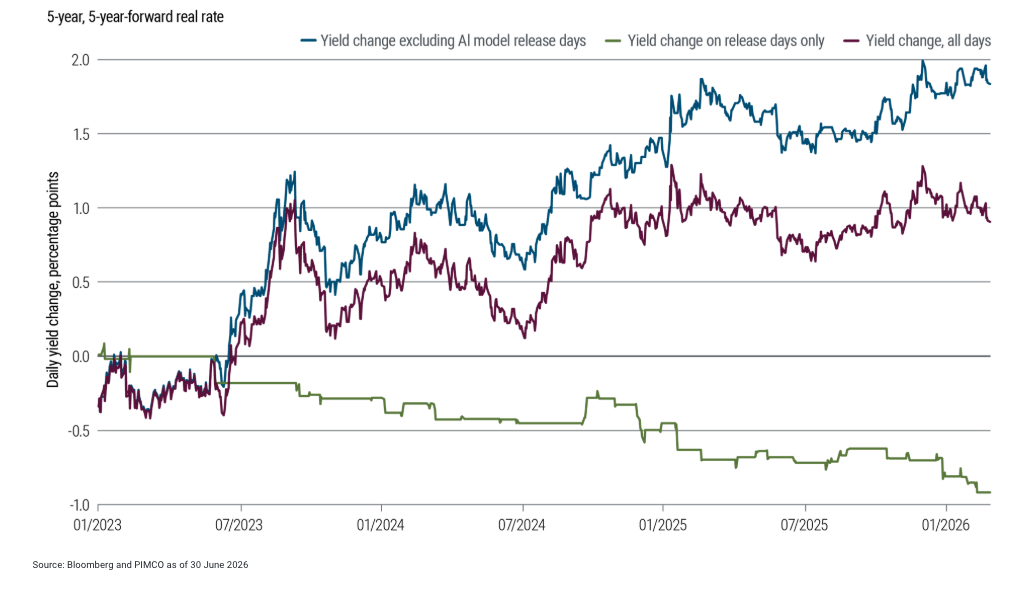

Figure 1 plots the cumulative change in the 5y5y forward real interest rate since January 2023, separately tracking how the forward rate responded on the 43 days that marked significant new model releases from OpenAI, Google, Anthropic, xAI, and DeepSeek. Even though the cumulative change in yields over this period was roughly 100 basis points (bps) higher, the cumulative yield change on model release days was roughly 100 bps lower. In other words, if we exclude the AI release days from the sample, cumulative yields would have risen 200 bps over the period. Researchers from MIT recently presented a more exhaustive study with similar results.Footnote1

Figure 1: AI model release days and cumulative changes in forward rates

This raises an important question: Why might AI lower, rather than raise, neutral interest rates?

One possible explanation is that AI is not purely a productivity boost, but also a source of economic disruption. While the long-run effects may be growth-enhancing, the transition itself introduces uncertainty around labor income and job stability. Households facing greater risk of displacement may increase precautionary savings, boosting demand for perceived “safe” assets and putting downward pressure on neutral rates. In this sense, AI may operate more like a risk shock, even if it ultimately raises potential growth.

This mechanism distinguishes the current episode from the late 1990s technology cycle. The earlier wave of innovation was broadly labor-augmenting and associated with widespread income gains. By contrast, current equity valuations suggest that the potential gains from AI will tend to be more narrowly distributed and disproportionately captured by a subset of capital holders. The resulting concentration of income gains – and the uncertainty surrounding the transition – may amplify precautionary behavior rather than reduce it. Research has also linked a declining r* to the decades-long decline in labor share of income (see our 21 May 2026 Macro Signposts, “AI, Market Power, and Diminishing Labor Share”).

There is also a second potential channel operating through fiscal expectations. Stronger productivity growth raises the long-run tax base and improves projected fiscal sustainability, all else equal. To the extent that markets capitalize higher expected future surpluses, this can compress term premia and support lower long-term yields.

While this framework abstracts from the possibility of offsetting increases in transfer spending, it suggests that AI-related news can cushion government bond valuations on the margin. Researchers from the London Business School and Stanford recently exploredFootnote2 this logic, arguing that because U.S. tax revenues are highly sensitive to long-run productivity growth and spending is much less sensitive, U.S. bondholders effectively have a long position in AI with option-like payoffs. Using a Federal Reserve Board staff modelFootnote3 to estimate term premia and rate expectations, we find that declining term premia explain around half of the overall decline in long-term yields around AI model releases.

Bottom line

AI is widely expected to push neutral rates higher, but we’re seeing market-based evidence that points in the opposite direction. While market reactions could shift over time, these dynamics at a minimum complicate the current policy narrative. Even if AI ultimately raises trend growth, its near- to medium-term impact may be to increase the demand for safe assets, compress term premia, and lower real neutral rates.

In other words, AI may be bond-bullish over the medium term – lowering neutral rates via precautionary savings and improved fiscal expectations – even as it raises longer-run growth potential.

Footnotes:

1Isaiah Andrews and Maryam Farboodi. “Do Markets Believe in Transformative AI?” National Bureau of Economic Research Working Paper 34243 (September 2025). Return to content↩

2Hanno Lustig, Howard Kung, and James Paron. “U.S. Treasury Investors' Massive Bet on AI.” The Two Cents, Substack (April 2026). Return to content↩

3Don Kim, Cait Walsh, and Min Wei. “Tips from TIPS: Update and Discussions.” Federal Reserve Board FEDS Notes (May 2019). Return to content↩

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Disclosures

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

The issuers referenced are examples of issuers PIMCO considers to be well known and that may fall into the stated sectors. References to specific issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold securities of those issuers. PIMCO products and strategies may or may not include the securities of the issuers referenced and, if such securities are included, no representation is being made that such securities will continue to be included.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author] and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

© PIMCO

More Income Topics >