Comprising approximately one-third of household wealth in the United States, the retirement market is massive. Of the $47 trillion currently held in retirement assets, the majority are within IRAs ($18 trillion) and 401(k) plans ($10 trillion).* This is not surprising since the 401(k) has been the dominant employer retirement plan for decades, with rollovers out of plans driving growth in IRAs. For plan participants and IRA owners it’s important to understand how these two retirement savings vehicles differ. Beyond the obvious differences such as contribution limits, ability to take loans and eligibility requirements, here are some other, lesser-known differences many savers may not be aware of.

* Investment Company Institute, June 2026.

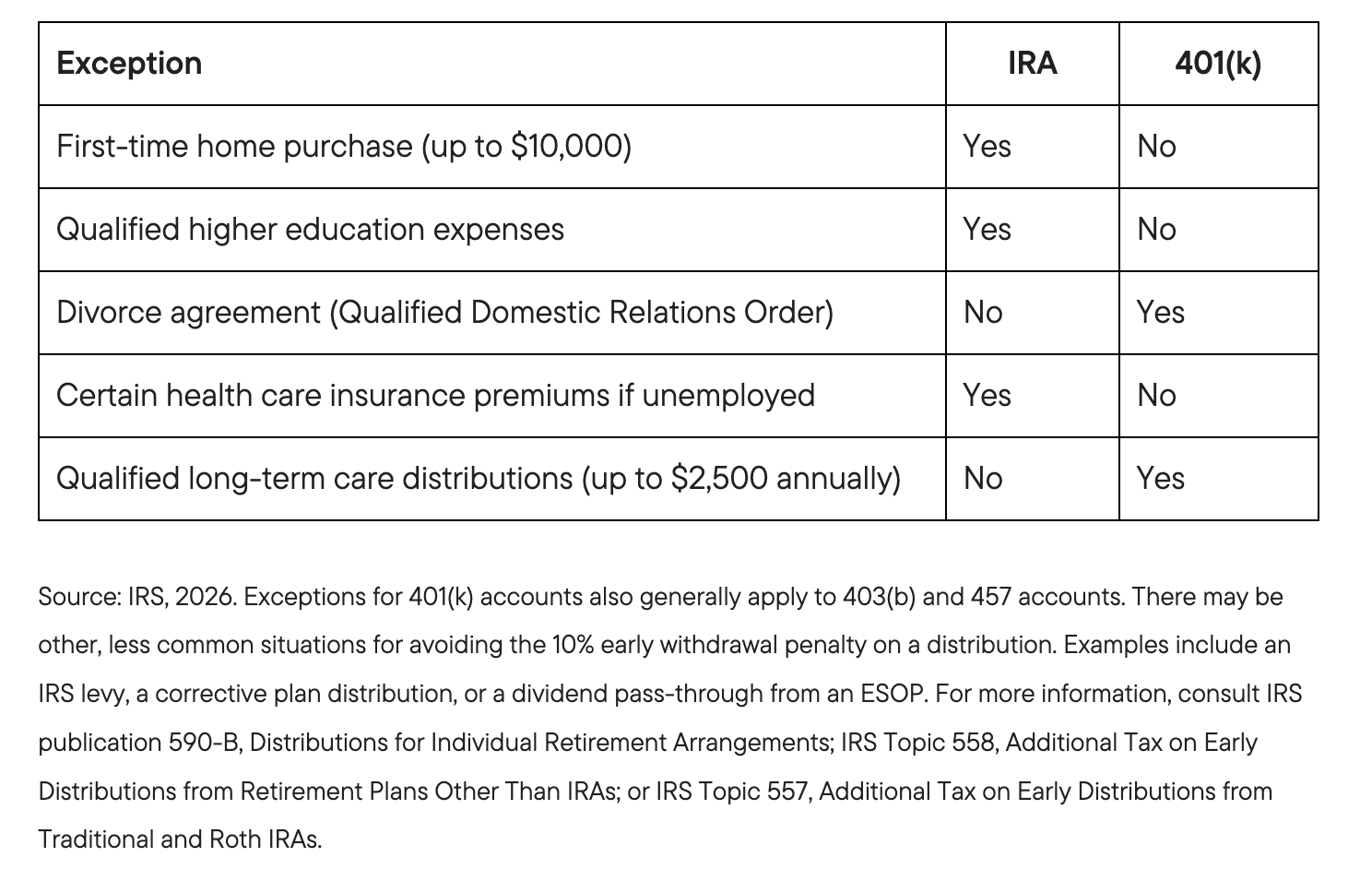

Avoiding Early Withdrawal Penalties

Withdrawal penalties are one of the most confusing areas given the proliferation of more exceptions over the past few years combined with differences in how they apply to IRAs and 401(k) plans. Here are the exceptions that apply to both:

- Death

- Disability

- Attain age 59 ½

- Substantially equal periodic payments (i.e. 72(t) distributions)

- Qualified birth/adoption expenses of up to $5,000

- Qualified military reservist distribution

- Unreimbursed medical expenses in excess of 7.5%

- Emergency withdrawal of up to $1,000 annually

- Terminal illness

- Domestic abuse

However, there are some key differences in how early withdrawal penalty exceptions apply:

See more: Size Matters in the Roth IRA Conversion Decision

Separating from Service and the “Rule of 55”

For some 401(k) participants leaving their job, this is an important provision to know. If you leave your job during the calendar year you reach age 55, the 10% early withdrawal penalty does not apply on a distribution from that plan. This feature only applies to the employer plan from which you are separating from service. Additionally, if the funds are rolled into an IRA, this option is forfeited. For some in this situation considering a rollover to an IRA or transfer to another employer plan, it may make sense to leave the funds in the former employer plan until reaching age 59 ½, when penalty-free withdrawals apply to everyone. Not all employer retirement plans offer this provision, so it’s important to review the Summary Plan Description for specific plan rules.

Option to Defer Required Distributions

While required minimum distributions begin at age 73 (or age 75 if you were born in 1960 or later), there is a provision within employer plans like 401(k)s—referred to as the “still working exception”—which allows these to be delayed. The option only applies to the current employer plan and is not allowed for those who own 5% or more of the company. Additionally, the plan must explicitly allow this. Once you separate from service, required distributions must begin.

After-Tax Savings and Roth Conversions

For IRA owners who hold a mix of pre-tax and after-tax (i.e. non-deductible contributions), tax reporting on a Roth IRA conversion can be a bit tricky due to the pro-rata rule. This means that a partial conversion will consist of a pro-rata portion of pre-tax and after-tax funds held in all your IRAs (including SEP and SIMPLE). That is, there is no way to convert only after-tax funds and avoid taxes on a Roth IRA conversion. However, this rule works differently within a 401(k) plan (subject to specific plan rules). 401(k) plans may allow employee contributions in three different account types: pre-tax, Roth, and after-tax. Both pre-tax and after-tax funds are tracked separately and may be converted to a Roth account without being held in aggregate, thus the pro-rata rule would not apply across the pre-tax and after-tax accounts.

The after-tax account, however, may have contributions and earnings in which only the earnings portion is taxable upon distribution or conversion. Conversions of after-tax amounts are pro-rated across the contributions and earnings within the after-tax account balance when completing an in-plan conversion. This is sometimes referred to as the “mega backdoor Roth strategy.”

There is a special provision for eligible rollovers of the after-tax balance from a 401(k) which allows the contributions and earnings portion of the account to be split and rolled over separately to a Traditional and Roth IRA. The contribution portion can be rolled directly into a Roth IRA without tax liability, and the earnings portion can be rolled into a Traditional IRA to avoid immediate tax. If the earnings portion is rolled into a Roth IRA, this would trigger a taxable event.

Beneficiary Distribution Rules

401(k)s and IRAs are essentially subject to the same beneficiary rules, which can be complex. The SECURE Act of 2019 (Setting Every Community Up for Retirement Enhancement) created new classifications of beneficiaries in determining how rapidly distributions are to be taken from retirement accounts. Most non-spouse beneficiaries are now required to empty inherited retirement accounts within 10 years of the death of the account owner, which has sparked new conversations around planning for legacy and tax considerations.

One important note is that employer plans like 401(k)s are often more restrictive than what the law allows and therefore may disallow the use of certain types of beneficiaries such as trusts or charities. An employer plan may also have more restrictive rules regarding the allowable schedule of distributions, and in some cases may force beneficiaries to take a lump-sum distribution after the death of the original account owner. A named beneficiary may be allowed to roll an inherited employer 401(k) plan account into an inherited IRA, so it is important to make sure that the 401(k) has up-to-date beneficiaries on file with any primary and contingent beneficiaries listed.

Seek Guidance

Properly navigating these rules around retirement accounts may make a meaningful difference in avoiding costly mistakes while managing your retirement savings. Consider working with a qualified advisor or tax professional regarding your specific situation.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Any information, statement or opinion set forth herein is general in nature, is not directed to or based on the financial situation or needs of any particular investor, and does not constitute, and should not be construed as, investment advice, forecast of future events, a guarantee of future results, or a recommendation with respect to any particular security or investment strategy or type of retirement account. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies should consult their financial professional.

Franklin Templeton, its affiliated companies, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon, by any such taxpayer for the purpose of avoiding tax penalties or complying with any applicable tax laws or regulations. Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the transaction(s) or matter(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

WF: 1149575

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Franklin Templeton

More Sustainable Investing Topics >