Midyear is a useful moment in investing—not because it tells us where we are going, but because it offers a clearer view of how little we truly knew at the start. Six months is often enough time for confident forecasts to meet reality, for consensus narratives to fray, and for the distinction between what sounded plausible and what proved durable to come into focus.

If the first half of 2026 has reinforced anything, it is that the most widely held expectations are often the least reliable foundation for investment decisions. Entering the year, the consensus outlook appeared reasonably well defined: moderating inflation, a more cooperative Federal Reserve, supportive fiscal conditions, and continued leadership from a narrow group of dominant companies. Instead, what unfolded was something more familiar—and more instructive. Growth proved resilient, inflation proved stubborn, policy uncertainty increased with the arrival of a new Fed chair, and markets were forced to adapt to a path that diverged meaningfully from the one investors had sketched out in advance.

The result was a quarter that felt unsettled. But discomfort and disorder are not unusual in markets; in fact, they are often the environment in which the most important adjustments take place. Investors tend to associate progress with calm, yet markets do not require tranquility to advance. They require only that fundamentals, expectations, and valuations find a workable equilibrium. When the noise level rises, as it did this quarter, the task is not to react to each new development, but to determine which developments matter.

In that sense, much of 2026 has presented opportunities to confuse volatility with insight. Yet beneath the shifting narratives, the primary driver of returns has remained unchanged: the ability of businesses to generate earnings over time. That may sound obvious, but it is often obscured when attention is drawn to policy debates, macro forecasts, or short-term market movements.

While markets whipsawed around headline shocks such as Liberation Day and the Iran conflict, underlying earnings growth—the fundamental anchor for equity valuations over time—kept driving prices higher. If there has been a meaningful surprise in 2026, it has been the persistence of corporate earnings strength. By the end of June, the S&P 500 total return index was up 10.21% year to date, reflecting a market that has continued to advance despite periodic setbacks in sentiment.

See more: A Brief History of Volatility and Recovery

Earnings Bucking the Trend

This year’s earnings story has been one of the most pleasant and important positive surprises for markets. In a typical year, analysts start out optimistic and then trim their numbers as reality sets in; whether you look at long-term history, the post-2000 period, or the last decade, the pattern is usually one of expectations drifting lower as the year unfolds.

That behavior makes sense: corporate managements have every incentive to guide expectations down over time, so the hurdle is easier to clear when results are reported. Most years, the game is about lowering the bar and then stepping over it.

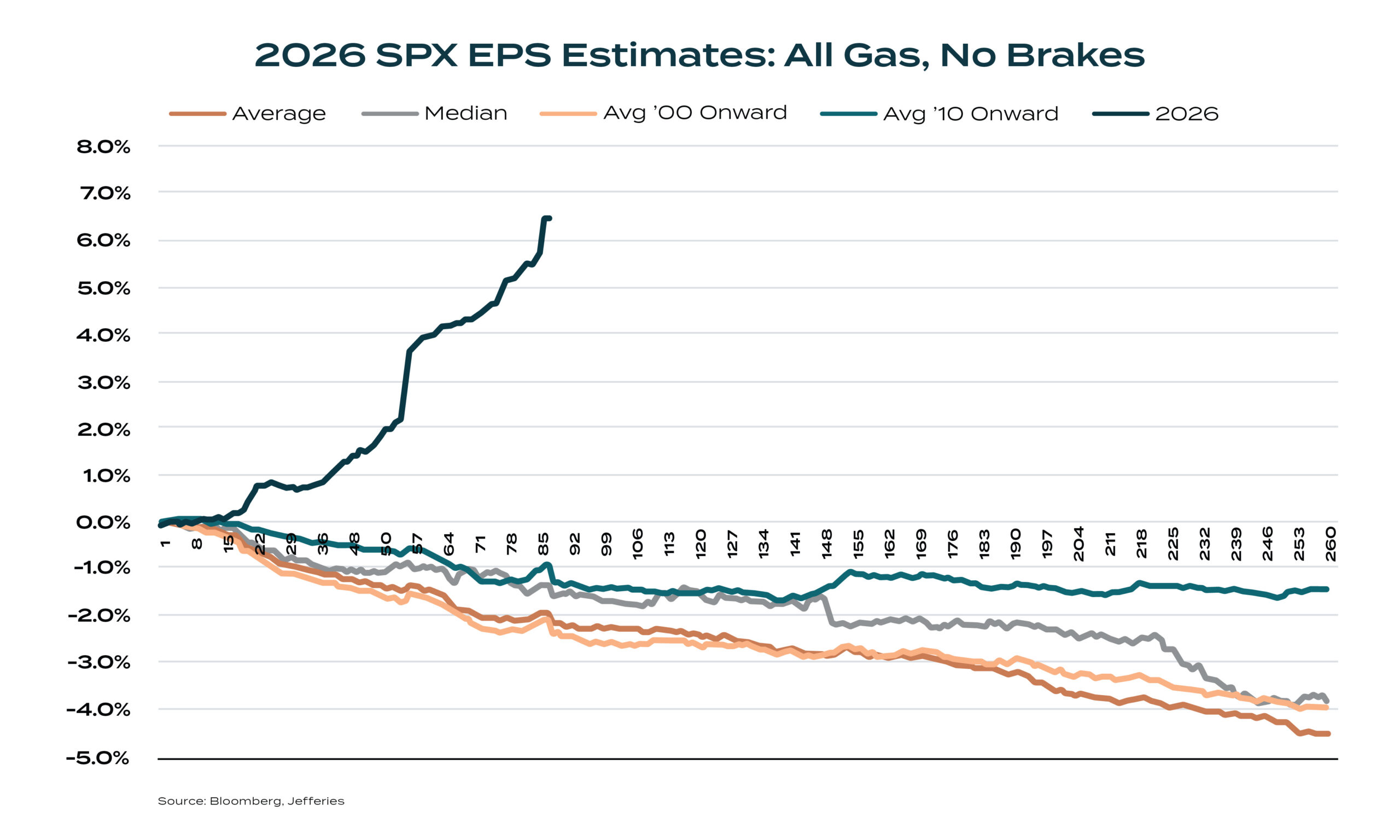

2026 has been different. Rather than the usual gradual markdown, earnings expectations have remained unusually resilient, and in many cases have even been revised higher. Instead of the bar being lowered, it has remained elevated, and companies have still managed to meet it. In our view, that strength in the earnings outlook has been a major reason equity markets have held up as well as they have, despite all the sources of uncertainty investors have had to contend with.

From Narrow Greatness to Broader Strength

Much of this year’s improving earnings expectations stems from the technology complex, but we are finally starting to see signs that this strength is spreading beyond its original home. For a time, almost all of the earnings growth, and a large share of the index’s returns, was concentrated in a small group of U.S. mega cap tech companies, the familiar names that dominated the tape day after day.

That degree of concentration has posed a real challenge for investors, particularly those with sizeable single stock positions. It is one reason Sequoia has developed thoughtful, tax-aware strategies to help clients reduce concentrated positions over time.

The more important development, in our view, is that we may now be in the early stages of a shift from a market powered by a handful of extraordinary businesses to one supported by a broader base of earnings growth. If that story continues to unfold, it will not only leave the market on a healthier footing, but also open up a wider and more durable opportunity set for investors who remain disciplined and diversified. The chart below shows that earnings growth is finally beginning to extend beyond U.S. mega cap technology companies.

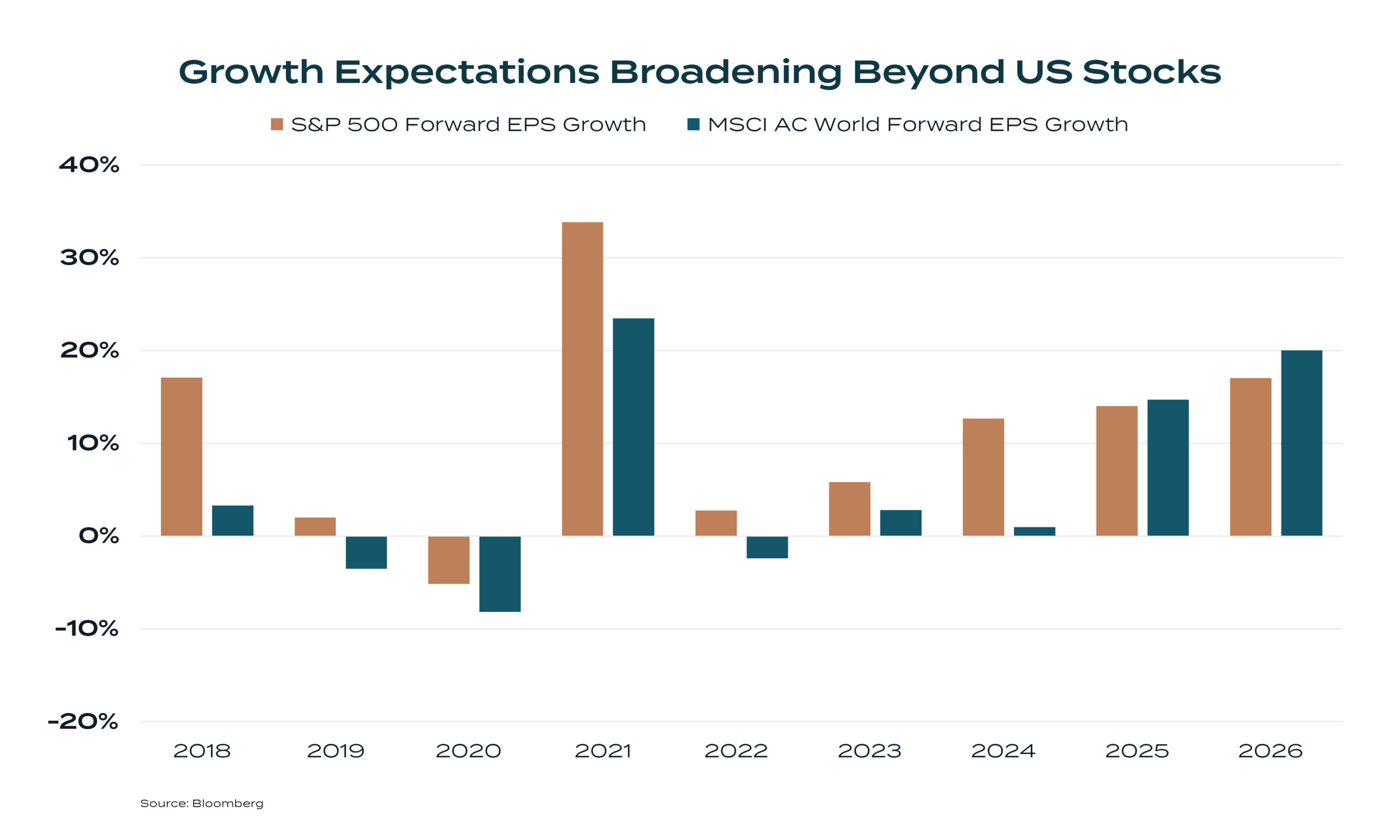

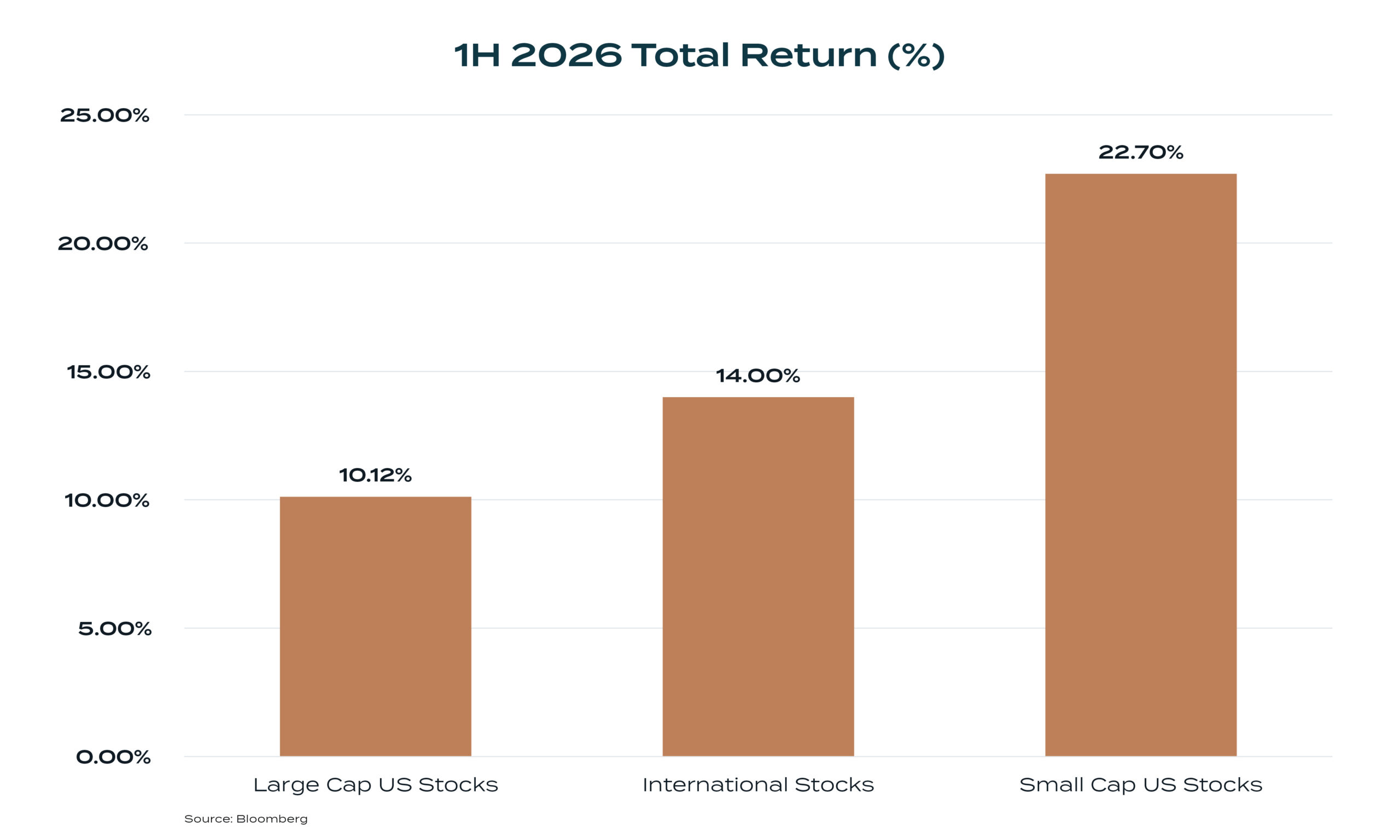

Broadening earnings expectations have begun to show up in performance across the global equity landscape as well. In other words, the improvement in the earnings outlook has been accompanied by a welcome broadening of the sources of equity returns.

As you can see below, large cap U.S. stocks, represented by the S&P 500, have lagged both international equity markets and U.S. small caps. That is not the pattern investors had become accustomed to in recent years, when a narrow group of U.S. giants dominated the scoreboard. In our view, this shift is consistent with the idea that the market is gradually moving from dependence on a few standout companies to a more widely distributed base of earnings strength, and that is a healthier backdrop for long-term, diversified investors.

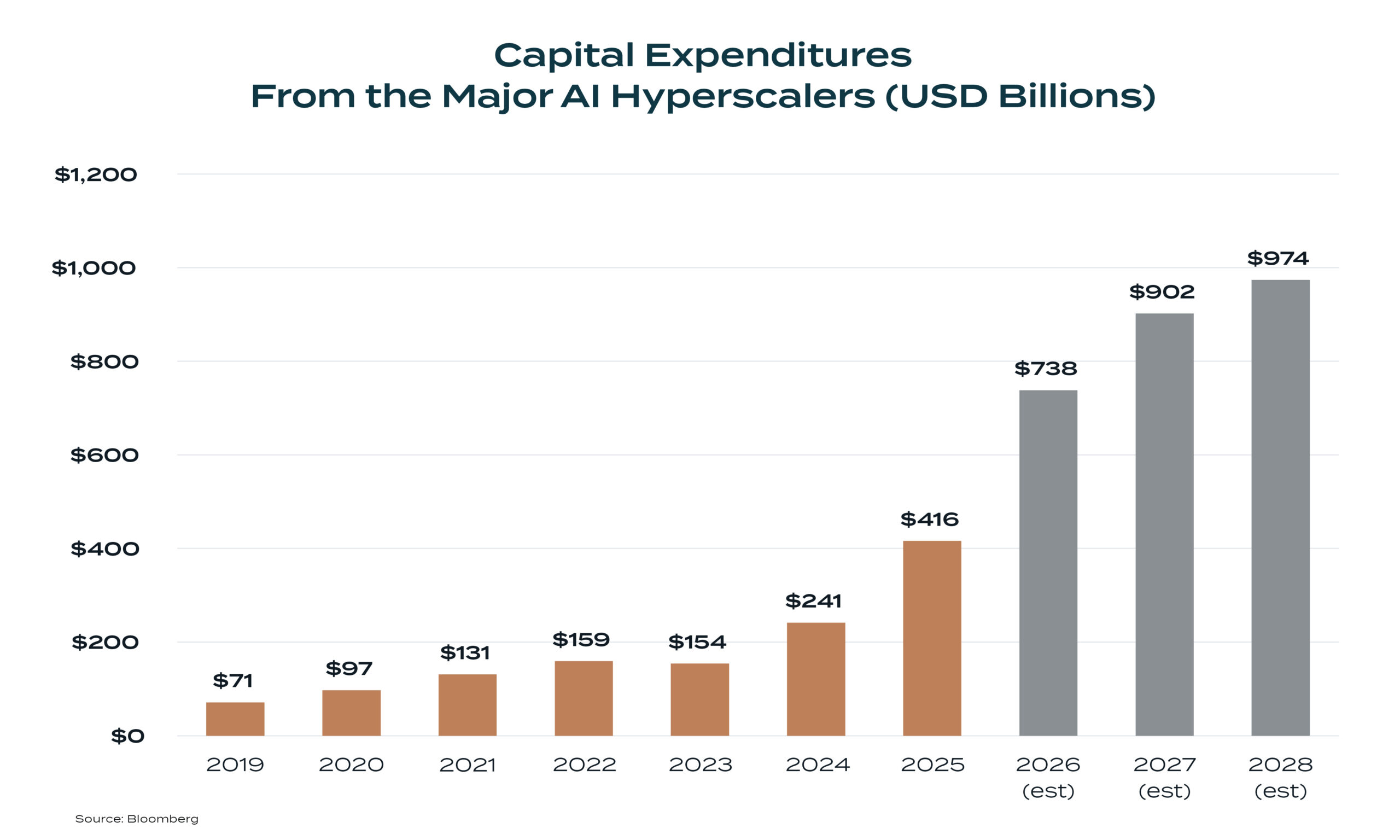

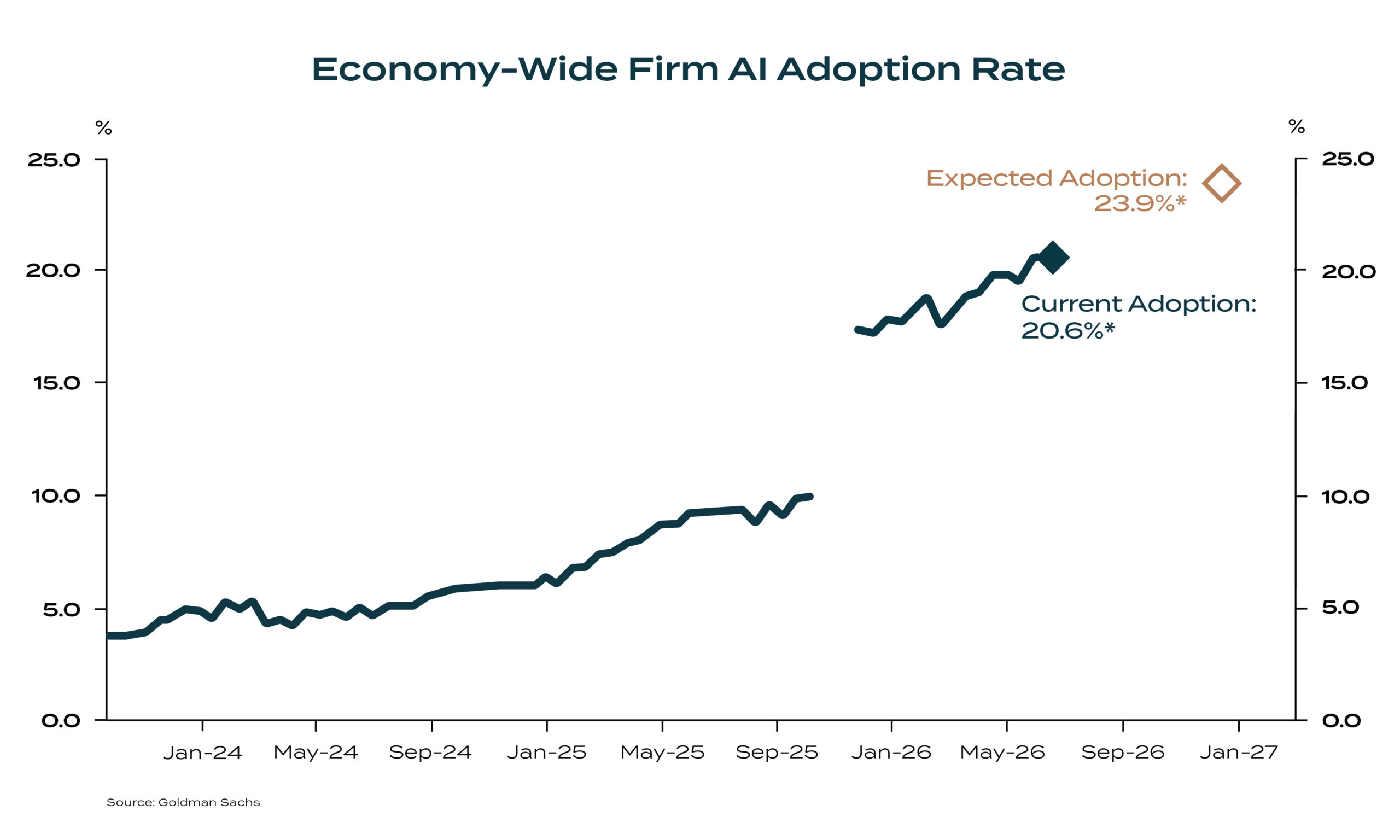

The enormous amount of capital devoted to building out AI infrastructure has driven what might be called phase one of the AI trade: the buildout phase. That has been a powerful tailwind for the companies that provide the hardware, networks, and platforms that make AI possible. But as the technology diffuses through the global economy, phase two is likely to be about the users rather than the builders. Over time, the greatest benefits should accrue to businesses that can harness AI to raise productivity, deepen customer relationships, and translate those advantages into sustainable earnings growth.

The chart below tracks AI adoption across industries. The essential point is straightforward: adoption is accelerating rapidly, yet we still appear to be in the very early innings. Many enterprises are only beginning to experiment, and most are tapping just a fraction of what these tools can do.

We are seeing this firsthand at Sequoia. We have recently implemented AI capabilities at the enterprise level, and the range of what they can already do is striking, from improving research and content creation to streamlining workflows and decision processes. Even so, we believe we are still in the early stages of realizing AI’s long-term potential across our business.

In that sense, we are a small reflection of the broader economy: testing, learning, and gradually weaving AI into everyday business activity. If this is what the early phase looks like, it is reasonable to think that the impact on productivity and profitability over the next several years could be considerably larger than most investors currently assume.

Risks Remain, Even as Opportunities Grow

We think it is reasonable to say that AI will prove to be a net positive for the global economy over time. The ability to do more with less, to automate routine tasks, and to augment judgment has historically been a powerful driver of growth. At the same time, the speed and breadth of this particular transition are almost certain to create air pockets along the way and meaningful industry-wide disruption. As the capabilities become more visible, investors are right to ask whether some business models that once appeared to enjoy wide and durable moats are as secure as they seemed.

Against that backdrop, it is more important than ever to have portfolios that are genuinely diversified and professionally managed. For long-term investors, the goal is twofold: to participate in the opportunity AI creates, while also being prepared to live through the inevitable dislocations that accompany structural change. Positioning portfolios to benefit from the winners without being overexposed to the losers is likely to be a key differentiator in the period ahead.

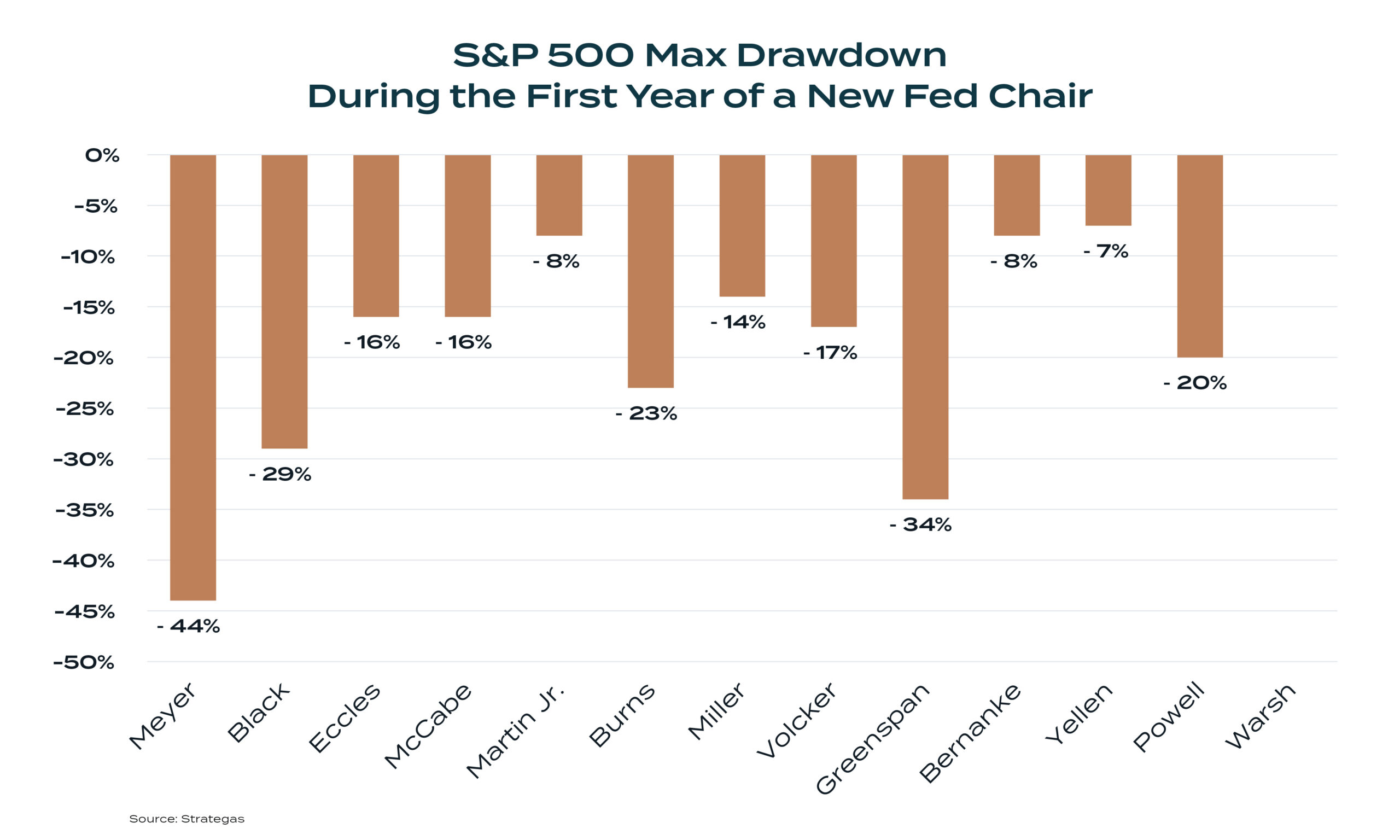

None of this means the worry list has suddenly gone away. In fact, there is no shortage today of potential sources of volatility. One of them is the new Federal Reserve chair, who introduces a significant element of uncertainty around the future path of policy. People often say bull markets do not die of old age; more often than not, they are ended by policy mistakes. That is one of the reasons we are paying such close attention to how this new regime evolves.

Alan Greenspan: A Note On The Current Market Environment

We were struck recently by the passing of Alan Greenspan. While his tenure as Federal Reserve Chair will be debated for years, one contribution endures with unusual clarity: his warning about “irrational exuberance.” It wasn’t a prediction so much as an observation—that from time to time, markets become less about fundamentals and more about psychology.

Events of the past few weeks have brought that idea back to mind.

We were presented with materials for a new venture capital fund organized by a well-known actor and his agent. The economics were notable—2.5% management fees and 30% participation in profits, contingent on a 3x return. But what stood out most was not the fee structure itself, but the underlying proposition: access. Not a differentiated process, not demonstrated investment acumen, but access to opportunities.

This does not appear to be an isolated case. Increasingly, capital is being raised through vehicles whose primary offering is entry—SPVs and syndicates that provide investors with the ability to participate, but often with limited involvement in diligence, governance, or ongoing oversight. In some cases, the distinction between investing and simply gaining proximity to investing becomes less clear.

It is important to acknowledge that access has always had value. Relationships matter, and they can open doors to attractive opportunities. But when access becomes the central feature being monetized, rather than a byproduct of expertise, it raises questions about where we are in the cycle.

In our experience, the most reliable signals are rarely the obvious ones. Instead, they tend to appear as small shifts in behavior—things that would have seemed unusual in other environments but gradually come to be accepted as normal. When investors begin to pay primarily for participation, rather than for judgment or skill, it may suggest a greater willingness to suspend skepticism.

None of this tells us what will happen next. Markets can sustain these conditions longer than expected. But it does suggest something about the current balance between risk and caution.

Greenspan’s phrase has endured because it captures something fundamental about cycles. Each period has its own justification, its own narrative explaining why the old rules no longer apply. And yet, over time, those narratives tend to encounter the same limitations.

Which brings us, once again, to a familiar conclusion: the belief that “this time is different” is itself among the most consistent features of markets.

Conclusion

We do not know what will happen next. We never do. But midyear offers a useful vantage point for seeing how much has already changed, and how far reality has diverged from the neat expectations that seemed reasonable at the start.

Coming into 2026, the story sounded straightforward: inflation would cool, the Federal Reserve would become more cooperative, fiscal policy would stay supportive, and a narrow group of dominant companies would continue to lead the market. Instead, what we have seen is more complicated and, in many ways, more familiar. Growth has been more resilient than expected, inflation more stubborn, policy less predictable with a new Fed chair, and markets have had to adjust to a path that bears only a passing resemblance to the one investors had penciled in.

The result has been a period that feels unsettled. Discomfort, however, is not a sign that markets are failing; it is often the backdrop against which the most important adjustments occur. Markets do not require tranquility to advance. They require that fundamentals, expectations, and valuations reach some workable balance. When the noise level rises, the challenge is not to respond to every headline, but to distinguish between what is interesting and what is consequential.

Equally important has been the character of that strength. For a long stretch, the market was powered by a narrow group of U.S. mega cap technology companies. Much of this year’s improvement in earnings expectations still resides in that complex, but the story is beginning to broaden. Large cap U.S. stocks have trailed both international markets and U.S. small caps, and we are seeing early signs that earnings growth is spreading beyond its original home. In our view, this evolution from narrow greatness to broader strength is a healthier backdrop for long-term, diversified investors.

AI has been central to this transition. The first phase of the AI story was the buildout: massive capital devoted to infrastructure, hardware, and platforms. The more interesting phase, looking ahead, is likely to be about the users rather than the builders. As AI diffuses through the global economy, the enduring benefits should accrue to businesses that can genuinely harness it to raise productivity, improve decisionmaking, deepen customer relationships, and translate those advantages into sustainable earnings growth. Adoption is accelerating, yet most enterprises are still in the early innings. If this is only the initial stage, the longterm impact on productivity and profitability may be greater than most investors currently assume.

None of this should be confused with a risk-free environment. AI will almost certainly be a net positive for the global economy over time, but the pace and breadth of change will create air pockets and real industry-level disruption. Some business models that once appeared to enjoy wide and durable moats may find those moats narrowing. At the same time, a new Fed chair introduces additional uncertainty around the future path of policy. History reminds us that bull markets do not simply die of old age; more often, they are undone by policy mistakes or misplaced confidence.

Which brings us to a familiar conclusion. The belief that “this time is different” is among the most consistent features of markets. Each period has its own narrative explaining why the usual disciplines can be relaxed. Each period also has its own way of reminding investors that fundamentals, valuation, and prudence still matter. Our task, as we see it, is not to predict the next shock or the precise timing of the next recovery, but to remain attentive to these underlying forces and to position portfolios so they can live through the full cycle—participating in the opportunities that genuine progress creates, while maintaining respect for the risks that never fully disappear.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Sequoia Financial Group

More Sustainable Investing Topics >