As the forces shaping bond markets become more local, the opportunities become more global. From energy stress to fiscal policy to advances in AI, today’s defining market forces are likely to play out differently across regions, sectors and issuers. We think that makes this an especially compelling time for US investors to broaden their bond allocation with hedged global bonds.

Central banks are following increasingly different policy paths as inflation and growth evolve differently around the world. Energy geopolitics are reshaping markets and repricing risk unevenly. Issuers able to secure lower-cost renewable energy have an advantage over those still exposed to volatile fossil-fuel prices. And some countries and companies are better positioned to capitalize on the AI-driven investment boom than others.

See more: Tax-Loss Harvesting: How Often Should It Happen?

The result is greater dispersion across global bond markets—and a richer hunting ground for active investors.

The Benefits of a Larger Opportunity Set

That broader opportunity set has long been one of the biggest advantages of global bonds.

While the US bond market is the world’s largest, it constitutes just 35% of the global bond universe. By shifting to a global strategy, investors gain access not only to a broader range of issuers, credit profiles and yield curves across regions and sectors but also to a wider mix of sectors—including sovereign and corporate bonds, investment-grade and high yield, and securitized assets such as residential and commercial mortgages.

This expansion goes beyond mere scale. Different countries operate under distinct economic, monetary and inflation regimes, offering uncorrelated return streams and alternative sources of income and risk. These differences can improve diversification and help investors better navigate shifting market conditions.

For active managers, this broader landscape offers not just different but better opportunities to generate income and excess return—particularly in today’s less-synchronized environment. Regional differences in inflation, growth and policy cycles can lead to diverse market dynamics—and in many cases, more attractive valuations or higher hedged yields than those available in the US. This added flexibility gives active managers more levers to pull in pursuit of alpha.

Hedged Global Bonds: Historically Higher Returns, Lower Volatility

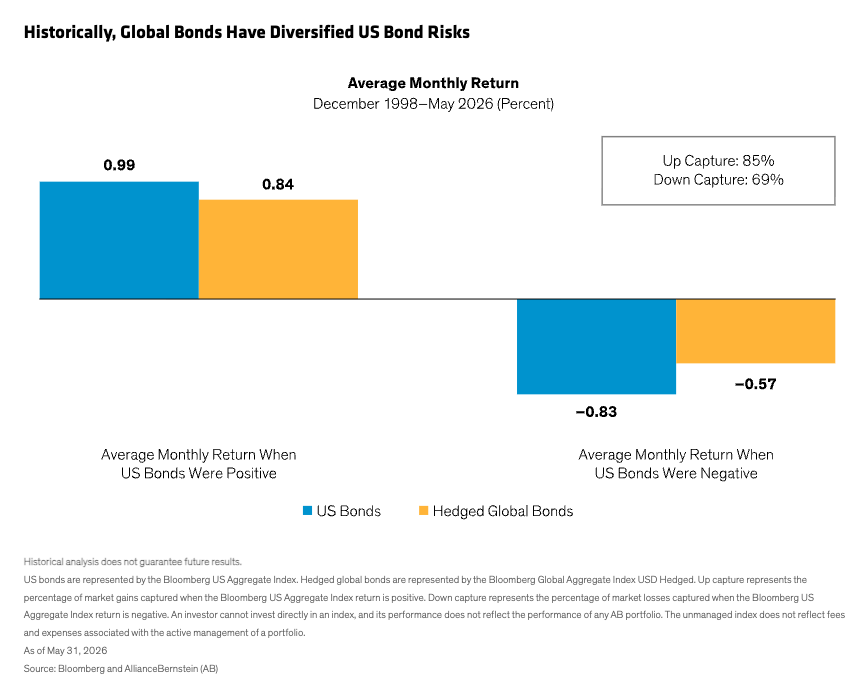

One of the biggest challenges facing US investors is how to reduce volatility without sacrificing return potential. This is where global bonds hedged to the US dollar can shine. Since the inception of the Bloomberg Global Aggregate Index in December 1998, hedged global bonds have captured 85% of the gains from US bond market rallies. But when US bonds sold off, hedged global bonds experienced just 69% of that downside (Display).

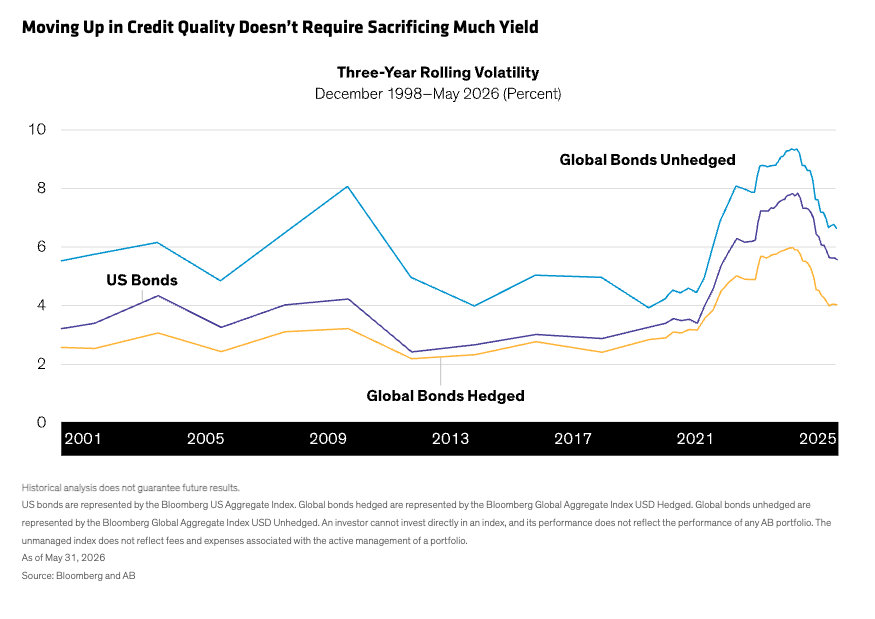

Underscoring the global bond market’s relative stability in diverse conditions, hedged global bonds have consistently exhibited lower volatility than US bonds over the past quarter century (Display).

Despite that lower volatility, hedged global bonds have outperformed US bonds over the period. Since its inception, the Bloomberg Global Aggregate Index (hedged to US dollars) has returned 3.9% versus 3.8% for the Bloomberg US Aggregate Index, on an annualized basis.

A global approach to fixed income can also help buffer equity market turbulence. Although both US and hedged global bonds have historically shown low or negative correlations to the S&P 500, the global strategy has proved especially resilient during periods of high US equity volatility.

In months when US stocks fell by more than one standard deviation, the correlation of hedged global bonds to stocks fell to 0.09 versus the 0.13 correlation of US bonds with stocks. In other words, hedged global bonds have historically buffered against US equity volatility more effectively than a US-only bond strategy.

Elevated Yields Create a Window for Global Income

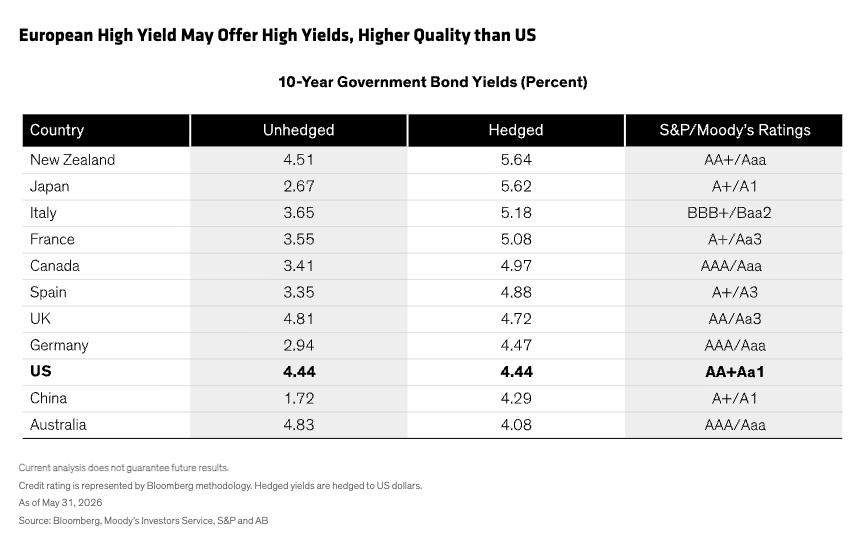

Many central banks have become cautious about easing or even hiked rates, helping to push yields higher across much of the developed world.

Higher yields do more than provide more income. They also help offset price declines that result from rising rates and widening spreads, providing a cushion in more volatile markets. In the case of 10-year government bonds, a hedging strategy can add 100 basis points or more to yields in developed markets (Display).

Today’s opportunity set is especially compelling. If global demand for US Treasuries declines and capital shifts toward smaller markets, the resulting drop in yields could lift bond prices in those markets—creating a tailwind for returns.

US Bonds Still Matter in a Global Strategy

Taking a global approach to fixed-income investing doesn’t mean forsaking US bonds. The US is still a key component of the global bond market, and active managers will allocate capital where risk-adjusted returns appear most attractive. At times, that may mean leaning into US bonds; at other times, focusing beyond it.

With volatility high, we think investors should consider ways to manage through bond market uncertainty while taking advantage of increasingly differentiated opportunities across global bond markets. In any market—and especially today—we believe a hedged global approach provides more opportunities to diversify risk, add alpha and generate income than a US-only bond strategy, while also delivering critical ballast in turbulent times.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

More ETF Topics >