Note from dshort: We're delighted to welcome Ed Easterling with this first installment of a two-part article on P/E ratios. Ed's books, Unexpected Returns and Probable Outcomes, have our unqualified endorsement for anyone trying to understand the complex and often puzzling relationship between the economy and the market.

Investors more than ever seek insights about likely stock market returns in the future. They have begun to recognize that higher valuations result in lower returns and, likewise, lower valuations result in higher returns. But in a world of high market volatility and economic variability, investors need a reliable measure of market valuation. That's where our hero, P/E, enters the story. P/E, also known as the price-to-earnings ratio, is the most common measure of stock market valuation.

THE BASICS

It is not as simple, however, as plucking price and earnings from the financial tables in the Wall Street Journal. Although the numerator (i.e., price) is fairly straightforward, earnings is subject to numerous distortions. That's why it is important to normalize the rollercoaster reports of earnings that occur across business cycles.

But in a world of high market volatility and economic variability, investors need a reliable measure of market valuation.

Keep in mind that the overall objective is to determine a relevant and reliable measure of market valuation. In other words, investors seek a measure of relative valuation to assess whether prices are high or low (i.e., expensive or cheap). The P/E ratio measures the current price in relation to the source of future returns — earnings. Earnings provides current cash from which to pay dividends and provides the future basis for price appreciation.

The impact from the level of P/E is significant. As the ratio of price to earnings increases, investors receive lower yields from the dividend payments and lower potential future appreciation. Therefore, P/E measures not only relative valuation, but also future potential returns from the overall market. No wonder that investors want and need a good measure for P/E.

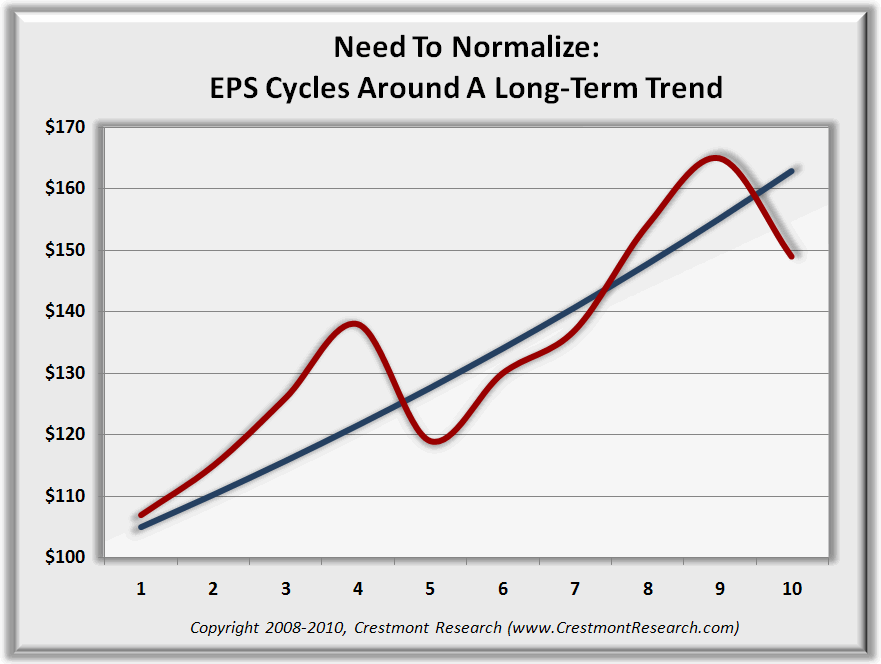

Earnings grow over time, generally in line with economic growth. They do not, however, grow at a steady pace. The business cycle drives earnings higher for several years (generally one to six), then fall for a couple years (generally one to three). Figure 1 illustrates the cycle.

The red line reflects the impact of the business cycle on earnings per share ("EPS"). It surges forward, and then steps back, before surging again. Each of the peaks and troughs create distortions to the long-term underlying trend, which is represented by the blue line in Figure 1. To avoid the misleading distortions to P/E from such high variability in E, investors need some way to adjust, or normalize, the red line to accurately reflect the underlying blue line.

Figure 1. EPS Cycle Illustration

THE METHODS

One of the most commonly reported methods for calculating P/E is to simply divide today's market price by the most recently reported earnings. Let's call this Simple P/E. This version of P/E shows up in the press, analyst reports, and in charts almost everywhere. Beware using it, however, because it sends such significantly distorted signals at business cycle extremes, which occurs every few years or so.

There are many methods to normalize earnings and provide a more reliable measure. Two of the most popular are known as the Shiller P/E and the Crestmont P/E. Robert Shiller of Yale University has popularized a method of normalizing P/E; it is also known as P/E10 and CAPE (Cyclically Adjusted Price Earnings ratio).

This methodology uses the actual reported earnings per share for the S&P 500 Index over trailing forty quarters (i.e., ten years). The quarterly EPS data is then interpolated to monthly values. Each value in the series is adjusted to today's dollars by historical inflation (i.e., into real terms).

Additionally, Shiller calculates a market price index for each month based upon the average daily closing price of the S&P 500 Index across the month. Each month's value for the market index is adjusted to today's dollars by historical inflation.

The P/E for each month is calculated based upon that month's price index and the trailing ten years of inflation-adjusted EPS data. As a result, P/E10 provides a measure of market valuation that excludes the distortions of inflation and mutes the variability of the business cycle.

The advantages of this methodology include: (1) it is relatively simple to calculate; (2) it is a recognized and well-vetted approach; (3) it is effective at reducing the distortions to EPS caused by the business cycle; and (4) it is an objective quantitative methodology. The shortcomings include: (1) it generates only a historical series and does not provide future estimates or forecasts; (2) it produces a value that lags by real growth; and (3) it inherently assumes that the distortions on both sides of the baseline are equal.

Keep in mind that aspects of this methodology prevent valid comparisons to most other P/Es. Specifically, this approach produces a value that is lagged by nearly five years in real terms. Though the methodology adjusts for the inflation rate, it does not account for the underlying long-term real growth in the economy and earnings. The purpose of a normalizing methodology is to determine reasonable values within the long-term trend that reflect the underlying baseline to the business cycle. In most instances, the baseline value that is used for the recent month, quarter, or year needs to be representative of current values rather than a value lagged in time by nearly five years. This creates a value for P/E that is approximately 15% higher (due to the understated EPS) than P/Es which are based upon current normalized EPS.

Further, P/E10 is also a measure that is solely based upon its components. One of the components is EPS, which has a tendency to be highly variable and sometimes skewed toward the downside. The overruns on the upside are less dramatic than the plunges on the downside. This asymmetry distorts the resulting measure of normalized P/E. And since this measure represents a ten-year average, excess distortions in EPS echo in P/E for a full decade.

P/E10 is a valid measure for relative historical analysis, as long as the measure for one period is compared to other periods or averages using this same methodology. It is not valid or appropriate, however, to use the average from this series for comparisons to P/Es from other methods without adjusting for two aspects of its methodology. First, the values and average related to the series should be adjusted for the "lag effect" that occurs from using a ten-year trailing average. Second, the average for the series should be adjusted for the "skew" that occurs from the tendency for reported EPS to skew toward the downside, which skews the related P/E ratio toward the upside. The first adjustment is unique to this methodology and the second adjustment is common across series that have skewed histories.

Another approach, the Crestmont P/E, offers additional features yet it is more involved to calculate. This P/E employs a similar method for determining the numerator, using the average daily closing price for the S&P 500 Index.

The difference is its approach to normalizing EPS. The Crestmont approach uses the fundamental relationship between gross domestic product ("GDP") and earnings. The fundamental relationship is driven by two elements. First, GDP essentially represents composite revenues. Second, profits emanate from revenues. Therefore, over time, profits grow in line with economic growth.

Although economic growth has some variability, earnings has its own cycle from the business cycle of competitive market forces. It is the second cycle that most affects EPS due to its frequency and magnitude. Over time, however, EPS reverts back to its baseline relationship to GDP. Economists recognize that the profit margins cycle is one of the most mean reverting cycles in the economy. Therefore, profits (as reflects in EPS for public companies) has a strong and fundamentally-driven relationship with GDP.

The Crestmont approach for a normalized P/E uses overlapping fifty-year regressions between nominal GDP and actual reported EPS to generate a series for EPS based upon historical and estimated future nominal GDP. This methodology mutes distortions from the business cycle, while generating a current value for normalized baseline EPS.

The advantages of the Crestmont Research methodology include: (1) it is effective at reducing the distortions to EPS caused by the business cycle; (2) it can provide future estimates and forecasts as well as provide historical series; (3) it provides a value that is current in time; and (4) it is an objective and quantitative methodology. The shortcomings include: (1) the methodology is not simple to generate; (2) it requires an accurate measure or forecast of past or future GDP, which occasionally undergoes slight revisions; and (3) the vetting of the methodology is not yet as extensive as the method popularized by Shiller.

For more information, the Crestmont and Shiller methodologies and other considerations are highlighted in the book Unexpected Returns and detailed further with graphs and analysis in the recently-released Probable Outcomes.

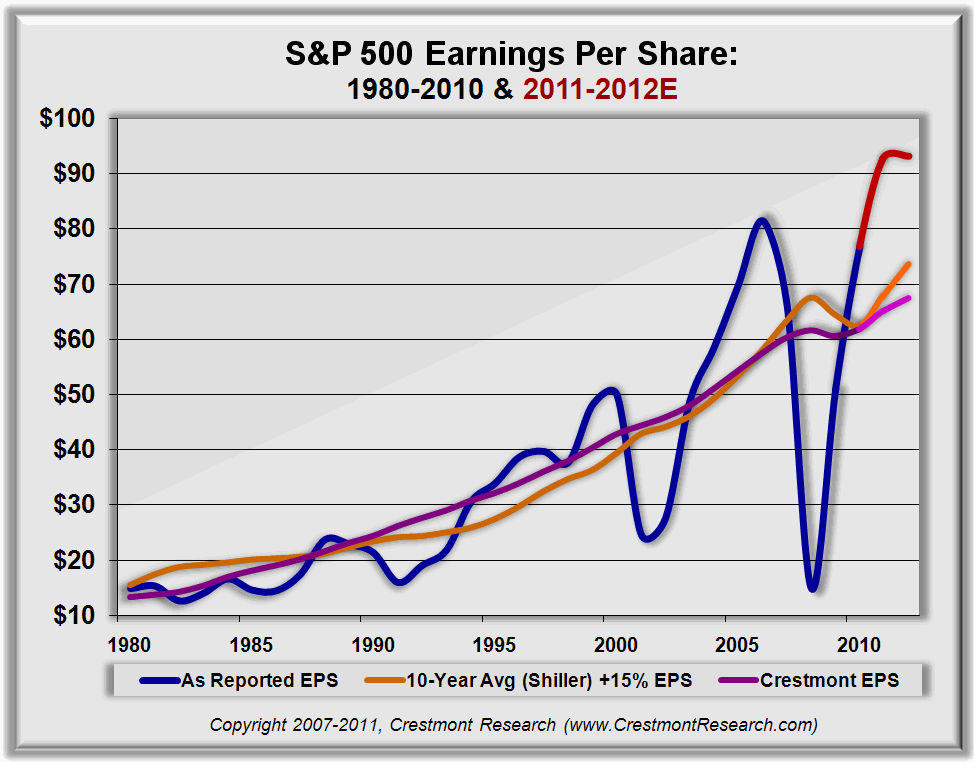

Figure 2 presents values for EPS over the past three decades based upon various methods. The key points to note are that (1) EPS is highly variable and needs to be normalized, and (2) both Crestmont and Shiller produce similar values (after adjusting for the lag distortion by Shiller).

Figure 2. EPS: As Reported, Crestmont, and Shiller

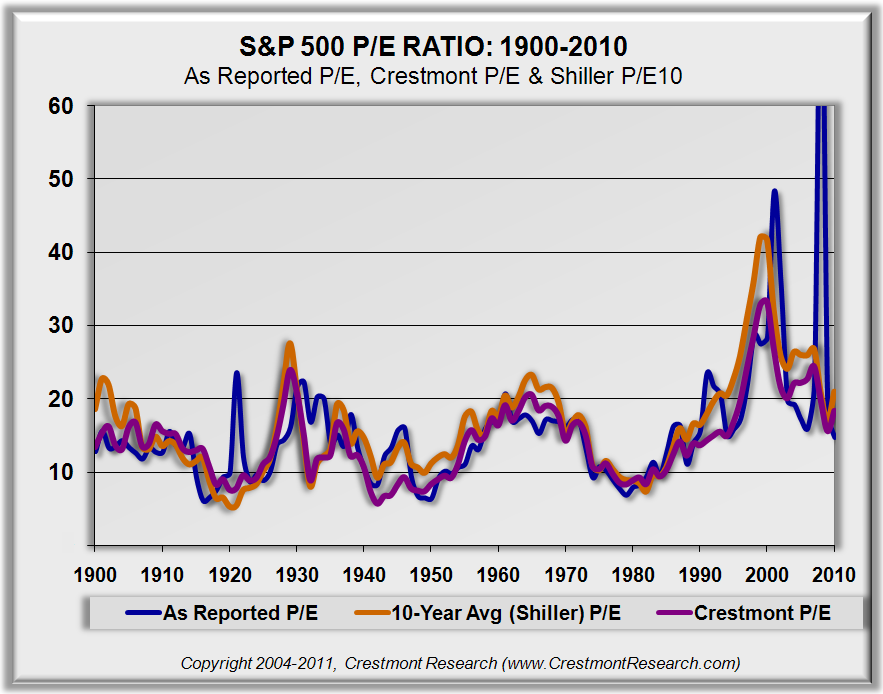

A normalized value for EPS generates a more relevant measure of P/E. Otherwise, P/E swings wildly and often sends an opposite or mixed signal about stock market valuation. Figure 3 reflects the annual P/E since 1900 using As Reported EPS and EPS from the Crestmont and Shiller methodologies. For this chart, note that the Shiller P/E has not been adjusted for the lag effect inherent in its EPS.

The first aspect to note is the high degree of consistency between the Crestmont and Shiller P/Es. Both approaches to normalizing EPS provide relatively similar results, although the Crestmont P/E offers a somewhat more stable series for the reasons previously discussed. Most of all, both of the normalized P/Es avoid the distortions caused by the business cycle.

At first glance, the As Reported P/E (blue line) tracks the other P/Es relatively closely. The variances, however, occur just when you will most want accurate insights. For example, consider 2008, 2001/2002, 1993, and quite a number of times back to and before 1921. The dips in the business cycle distorted EPS well below the baseline growth level. As a result, reported P/E spiked indicating an expensive stock market. Yet those points would have been regretful times to sell. Conversely, consider the times with the opposite business cycle distortions (2006 and 1999 as examples of the most recent two). Cycle highs in EPS distort P/E downward and flash "GO" just when the more rational view indicates caution. Be aware that 2011 or 2012 may soon be added to that list.

The key takeaway from Figure 3 is that As Reported P/E is relatively similar to the normalized versions, certainly enough of the time to inure complacency about the need for an alternate approach. Then, just when you need it most, the Simple P/E using As Reported EPS transmits a signal from the other side of Alice's looking glass. It screams action that is opposite from reality. When the data is viewed with greater granularity using quarterly or monthly data (upcoming in the second part of this article), the distortions are more extreme and frequent.

Figure 3. P/E: As Reported, Crestmont, and Shiller

A valid measure for P/E, without misleading distortions, provides numerous opportunities to better understand what drives stock market returns over time and to assess the current valuation level.

Speaking of misleading, be especially aware of the relatively new P/E known as Operating P/E. This is the Darth Vader of all P/Es. Operating P/E generally uses future expected operating earnings per share as the denominator. Be especially skeptical about the use of future expected values, especially with a series that has business cycle distortions. There is a tendency for analysts to extrapolate trends, which often leads to overly aggressive forecasts at cycle tops and understated estimates at troughs. Extrapolation can compound the typical distortions in P/E.

Second, and foremost, operating EPS is a measure of earnings that is intended to remove one-time gains and charges to provide a more consistent measure of future earnings and dividends. Optimistic analysts tend to add-back charges, but often don't exclude all of the unusual gains. The result is a bias of positive adjustments to EPS that drives an artificially lower value for the ratio of P/E.

A warning label should be applied when Operating P/E is used: "Do not compare Operating P/E to any other historical measure of P/E except Operating P/E." Most often, however, inexperienced media and promoting analysts not only compare Operating P/E to P/Es based upon net earnings, they often use the average for the Shiller P/E, with its 15% "lag effect" overstatement and reported EPS skew. That's like comparing the temperature in Celsius to a Fahrenheit scale!

The next part of "P/E: So Many Choices" further explores the primary driver of P/E over time and the signs of an overvalued, fairly-valued, or undervalued stock market.

Copyright 2011, Crestmont Research (www.CrestmontResearch.com)

Ed Easterling is the author of Probable Outcomes: Secular Stock Market Insights and award-winning Unexpected Returns: Understanding Secular Stock Market Cycles. Further, he is President of an investment management and research firm, and a Senior Fellow with the Alternative Investment Center at SMU's Cox School of Business where he previously served on the adjunct faculty and taught the course on alternative investments and hedge funds for MBA students. Mr. Easterling publishes provocative research and graphical analyses on the financial markets at www.CrestmontResearch.com.