There’s a memorial to Paul the octopus at the Sea Life Centre in Oberhausen after the cephalopod seer earned worldwide fame by correctly predicting the outcome of all Germany’s seven games at the 2010 World Cup

The search for havens from the worst inflation in four decades feels like it’s about to get a lot more real. The bad news is that the task isn’t looking at all easy or straightforward, at least for individual investors whose choices are confined to the standard asset classes and who rely on a traditional 60-40 portfolio mix of equities and bonds to weather the ups and downs of market cycles.

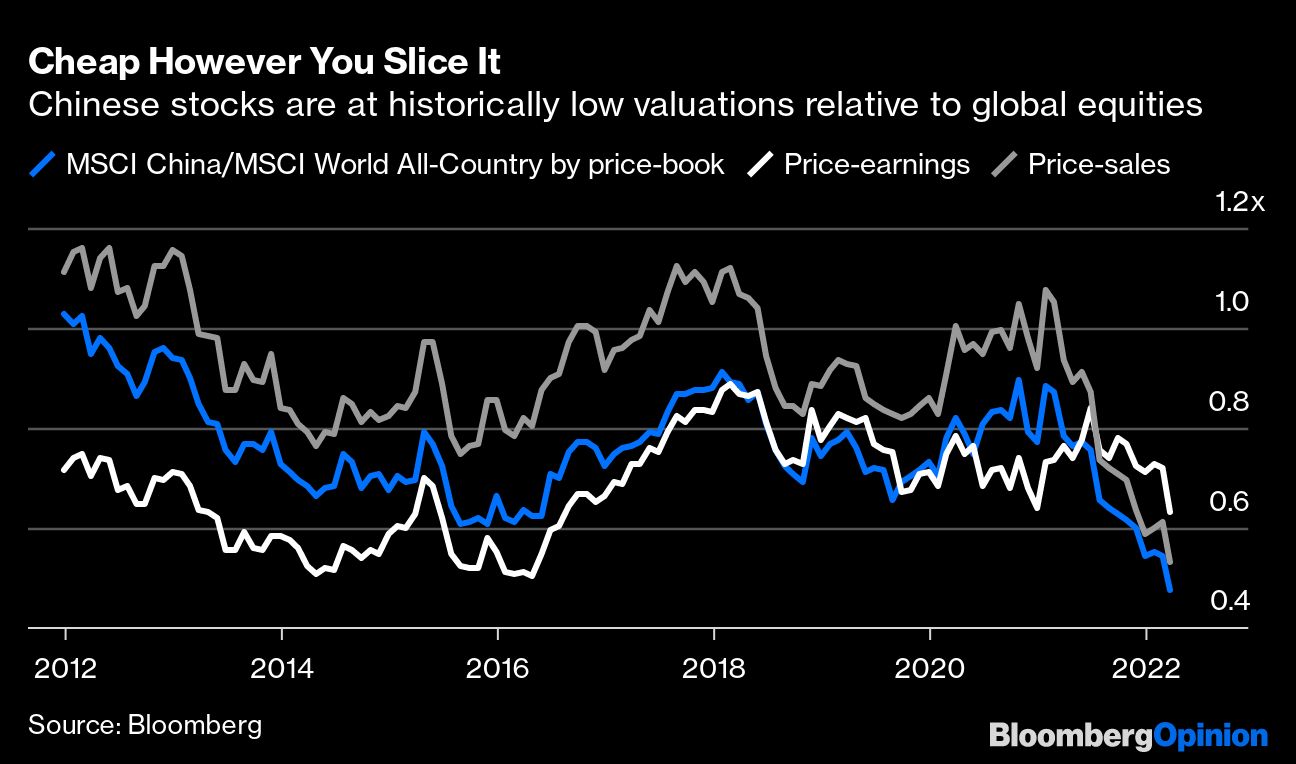

Things are never as good or as bad as they seem. That adage has generally served investors well. Ignoring the extremes of optimism and pessimism can spare equity buyers some painful mistakes — such as piling into tech stocks at the height of the dotcom boom — and may signal lucrative opportunities for the brave, such as during the depths of the 2008 global financial crisis.

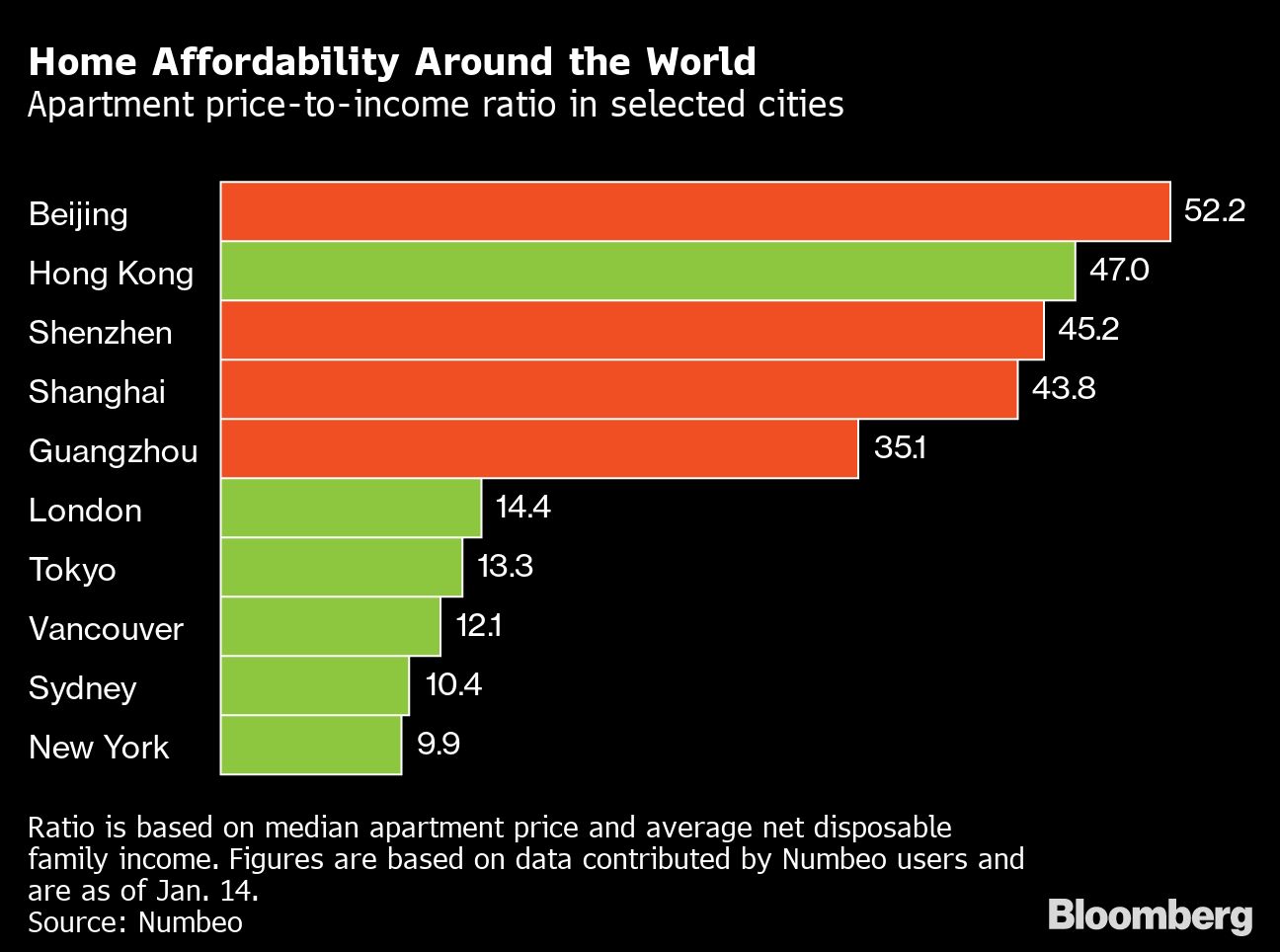

For a year and a half, Chinese authorities have been trying to reduce property prices, leverage, and the economy’s dependence on the real estate industry. As defaults and distress spread, from China Evergrande Group to Kaisa Group Holdings Ltd. and others, the first signs of a shift toward policy easing emerged last year.