Who could have foreseen the selloff in shares of big technology companies? Anyone who bothered to do a little math.

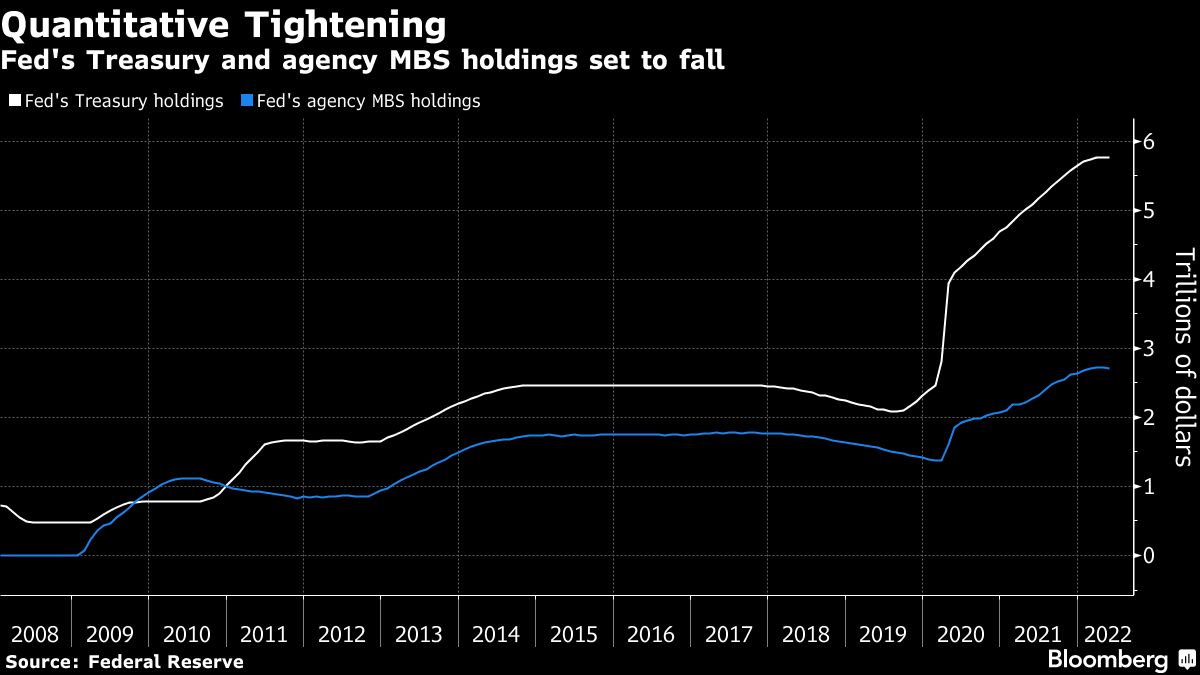

With the Federal Reserve releasing minutes from its latest meeting on Wednesday, traders are looking for further details on the plans to let billions of dollars worth of bonds to mature each month without replacing them.

Every advisor will agree with the goal of giving their clients peace of mind. But there’s mounting evidence few actually do. Why is that?

Recent warnings from corporate executives and rapidly declining regional manufacturing surveys make me wonder if a recession has already started.

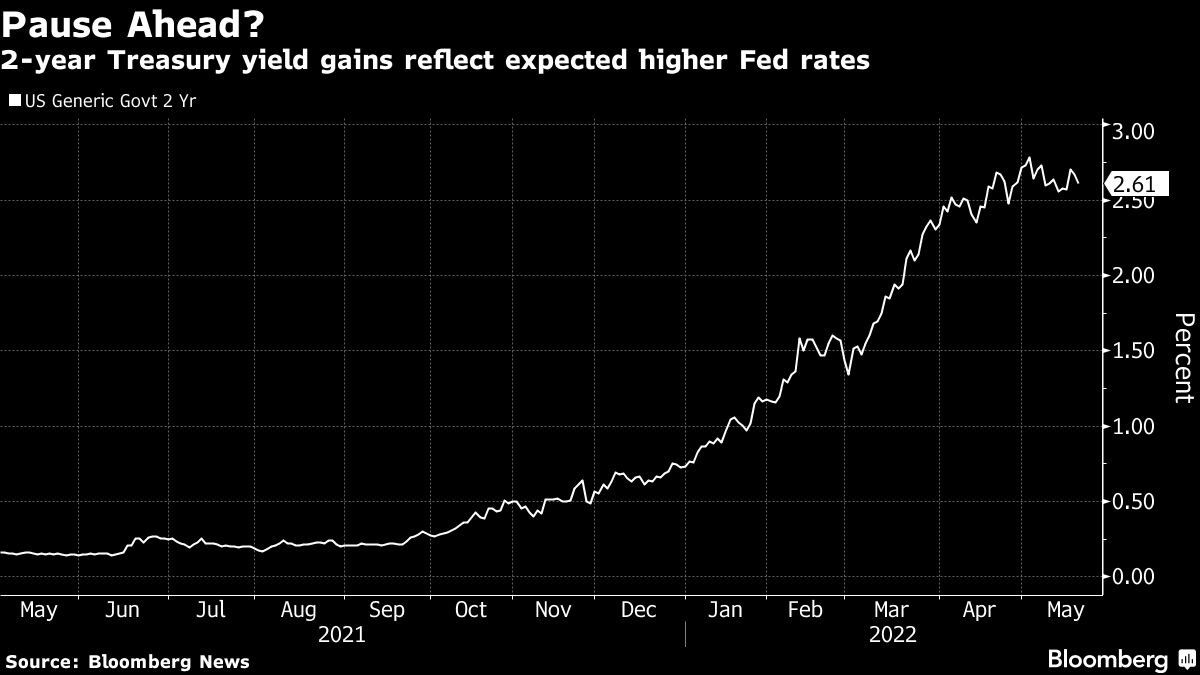

Federal Reserve Bank of Atlanta President Raphael Bostic has cracked open the door to discussing a September pause in the central bank’s aggressive rate hikes -- a move that will only be on the table if inflation falls more than expected over the summer.

In the face of bad news, what, if anything, should you do to adjust your long-term portfolio management strategy?

I want to draw your focus to the three most important, yet boring, tax strategies that every advisor should be discussing with every client.

You can do plenty to improve your client's experience, and you don't need any software or other tools to do it.

RIAs can be paid to service trails-paying annuities without a broker-dealer.

What can you do about an overly restrictive compliance department? Or a non-responsive compliance department? Or one where you get different answers depending on who you ask?

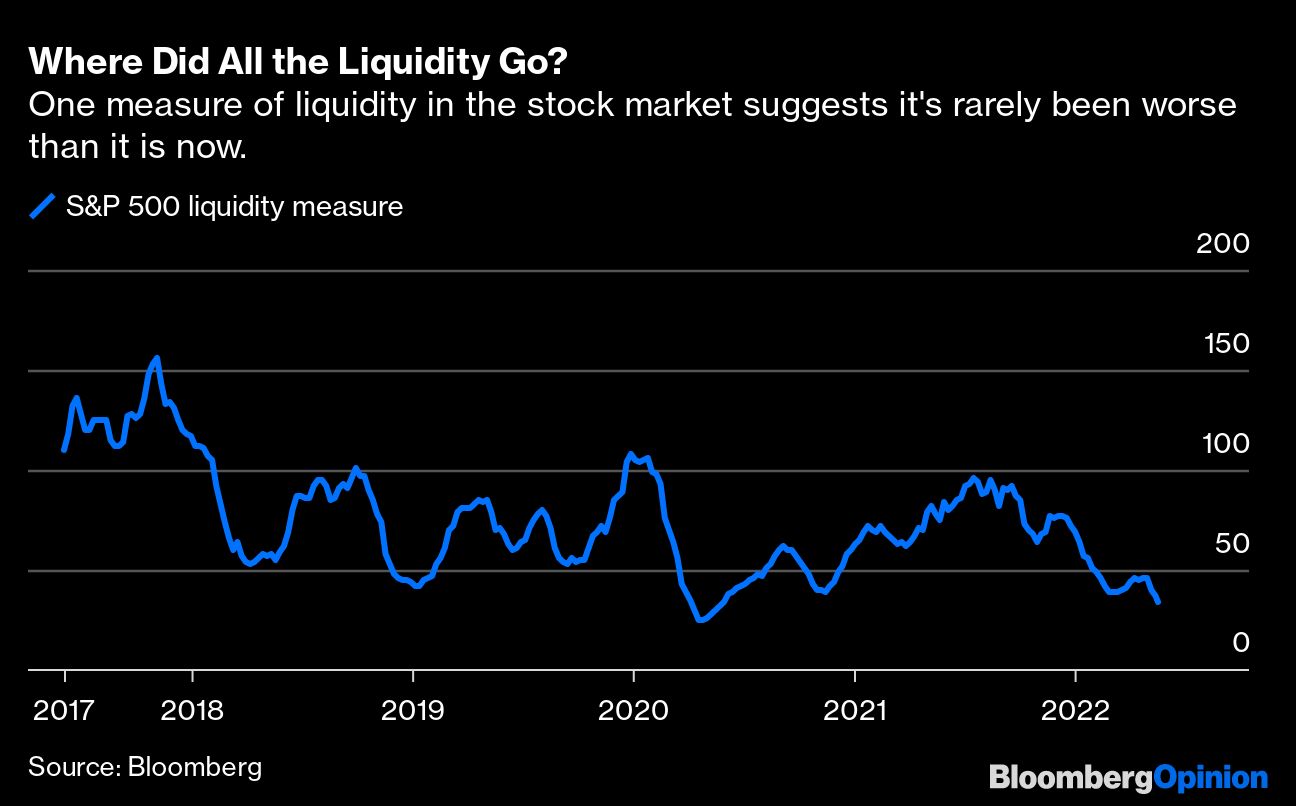

Liquidity is the lifeblood of the capital markets. It is the ease at which an asset can be turned into cash without disrupting the price of that asset. This was never really a concern in the US, whose markets are prized for being the deepest, most liquid in the world. It’s one reason why the dollar is the world’s dominant reserve currency.

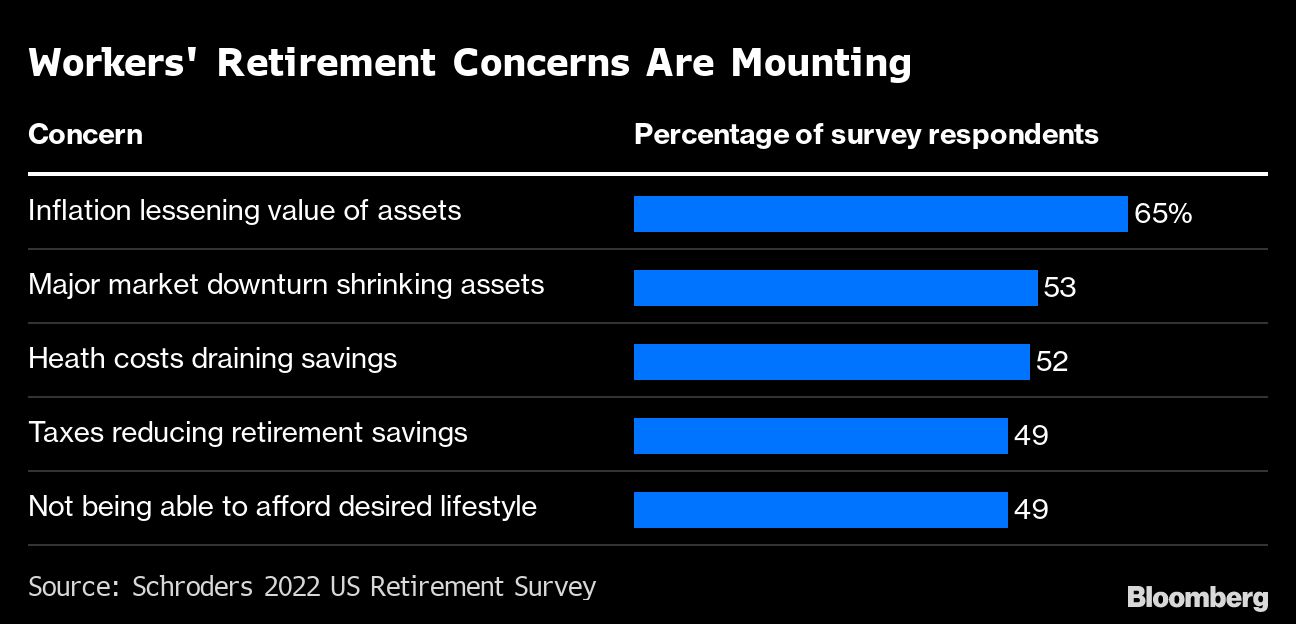

Many Americans expect a significant shortfall in their retirement savings. Fifty-six percent said they expect to have less than $500,000 saved by the time they retire, including 36% who anticipate having less than $250,000.

Russia’s blockade of Ukraine’s ports is a “declaration of war” that threatens to trigger mass migration and a global food crisis, a United Nations official said, adding to the dire warnings on the opening day of the World Economic Forum in Davos.

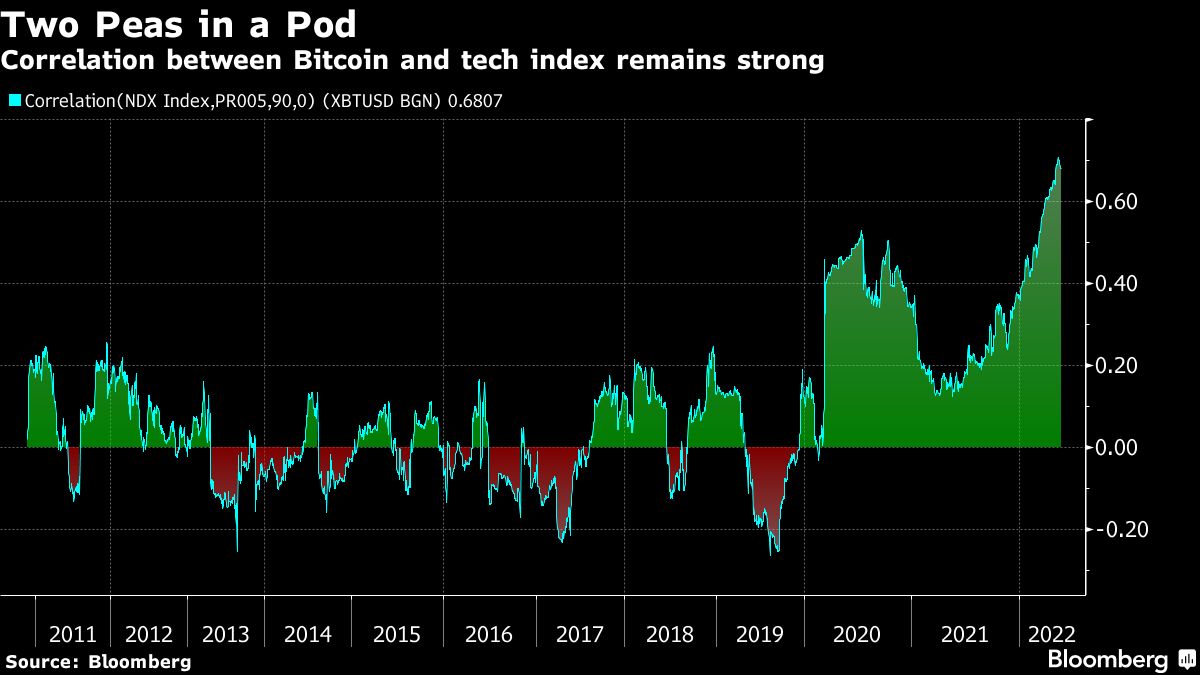

Bitcoin, which trades 24/7, has largely tended to move higher on weekends, and the coin hasn’t been posting any abnormal moves between 9:30 a.m. and 4 p.m. on Saturdays and Sundays, which are the stock market’s US operating hours during the week.

Wall Street lenders are calling on the US government to hold off on launching a digital dollar, arguing that a virtual currency backed by the Federal Reserve risks draining hundreds of billions of dollars out of the banking system.

The Federal Reserve has talked a lot about its goal of a soft landing for the economy as it raises interest rates to fight inflation, but there hasn't been as much talk about what that would look like for workers.

"The bear is coming! The bear is coming!" Indeed, it is. Should you be worried?

Shiller’s CAPE ratio is the most-cited predictor of long-term equity returns. But new research shows that the “Buffett” indicator does a good job of forecasting, and both ratios predict subdued, long-term returns for stocks.

The following is a hypothetical and fictional account of how big tech can disrupt the wealth management industry. A back-to-client focus is discussed. reminiscent of how Apple’s Mac OS empowered users and supplanted predecessor operating systems.

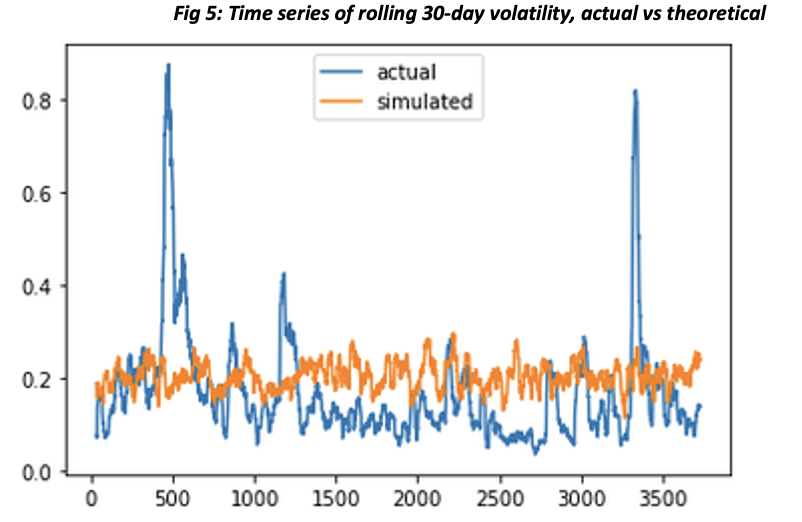

Volatility is the standard measure used by advisors to measure risk. It has been useful but has limitations. There are ways that volatility will not provide an accurate representation of the risk of an investment portfolio.

“I have been poor, and I have been rich. Believe me, being rich is better for the soul.”

Two of the world’s most respected investors, Jeremy Grantham and Ray Dalio, offered identical warnings: The bubble in U.S. equities is unwinding, and the economy is headed for stagflation.

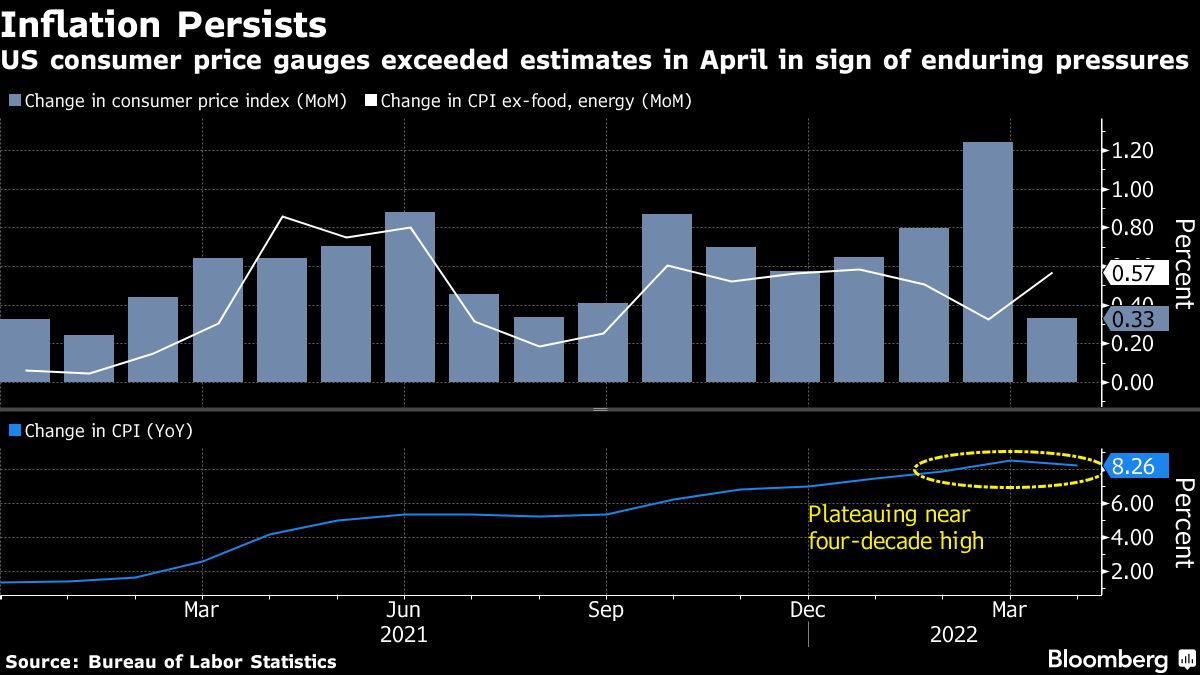

Wherever you get your news, there's no escaping the perception that rising prices are breaking the US economy. Recession is almost a foregone conclusion on the Bloomberg terminal, which aggregates 150,000 news sources with every bulletin categorized and counted. Headlines with the word “inflation,” increased 345% to 186,000 times a month since the beginning of 2020, while “strong economy” declined 48% to 1,766 times monthly.

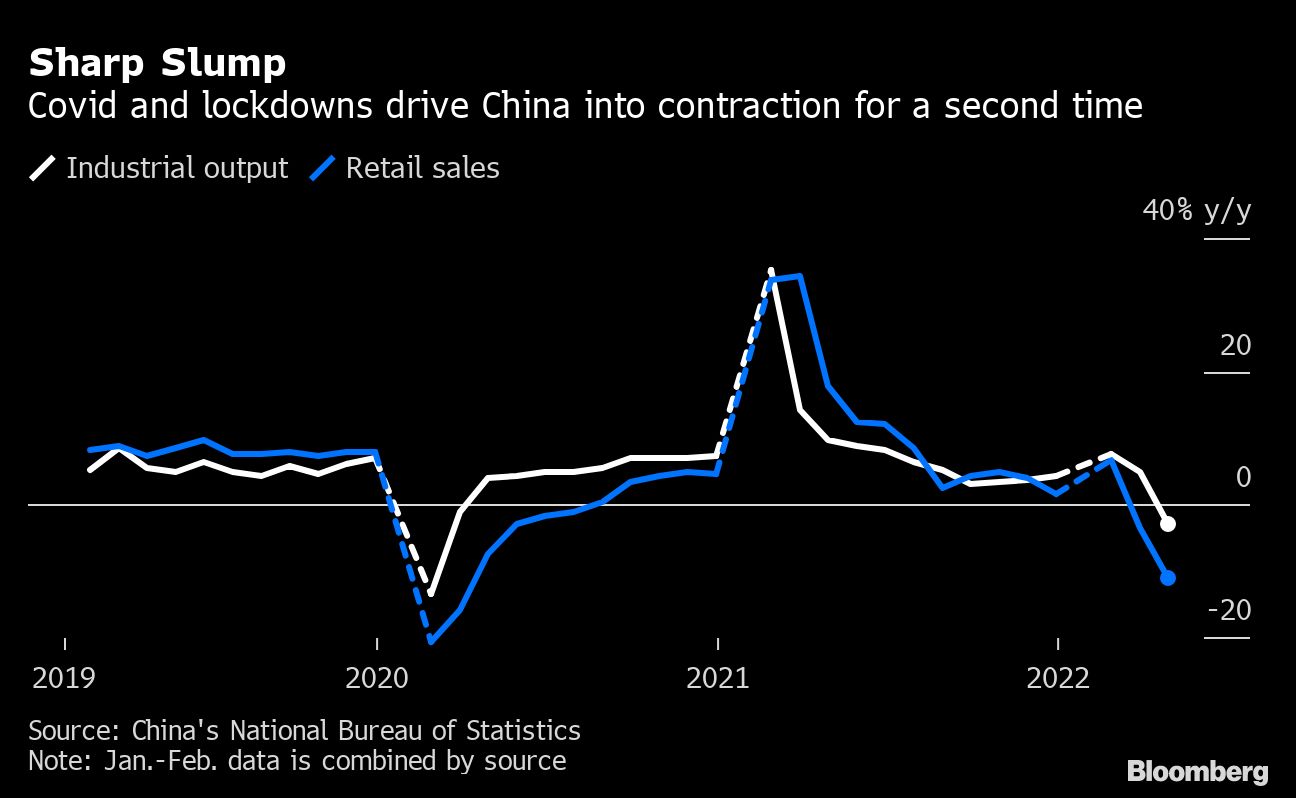

The US economy is starting to show signs of strain under the weight of decades-high inflation and climbing interest rates -- raising the risk of a downturn.

Some 162 companies in the S&P 500 Index received target price reductions Thursday compared with only 62 increases, according to Bloomberg data. The difference marked one of the sharpest swings in analyst sentiment in the 11 years of the series.

Technology stocks have taken a deep dive, blue-chip stocks are ailing, stablecoins aren’t stable, and don’t even ask about traditional crypto. Art markets, however, are alive and well — and it’s worth asking why.

The parallels between the 2020s and the 1970s grow more numerous by the day. The economy faces the threat of stagflation. Fuel prices are surging, and shortages loom. Politicians are flailing. The international environment is deteriorating. The Supreme Court is revisiting the 1973 Roe v. Wade ruling.

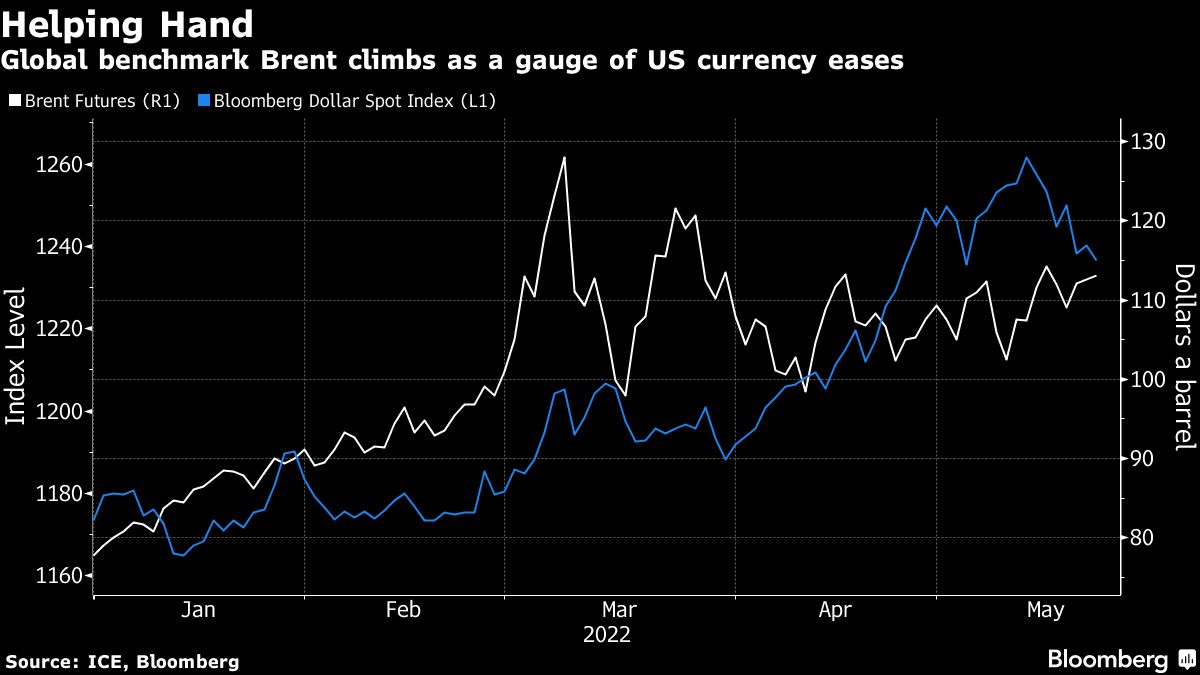

The rise in energy costs has contributed to rampant inflation, prompting central banks to raise rates and stoking investor concern growth will slow. The Biden administration is considering tapping a little-used emergency diesel fuel reserve to mitigate the supply crunch amid Russia’s invasion of Ukraine, according to a White House official.

A fatal shortcoming lies beneath the academic papers that have relied upon “back-testing” to promote the 4% rule. Use our Premium membership service to add your logo and send this to clients.

There are thousands of mutual funds that offer to select stocks and bonds for your portfolio. But which ones are right for you? Use our Premium membership service to add your logo and a note from you and forward it to your clients.

It can take three years before a niche focus takes off for your financial advisory business. This article covers seven marketing steps for year one to ensure you lay a solid foundation for success.

Tesla has grown into a $735 billion company on the back of its breakthrough electric-vehicle engineering. Its own carbon footprint is a small fraction of its peers, and its success in the market has pushed the industry overall away from gas-powered vehicles.

So here we are: When investors aren't worried about inflation, they're worrying about recession. Tech companies are announcing hiring freezes and job cuts in growing numbers. Homebuilders are starting to talk about slowing demand and the supply of existing homes is rising. Walmart reported this week that it has excess inventories.

New graduates face fierce financial headwinds of soaring rent, ballooning student debt and inflation. The oft-repeated message to the young to “save early and often” may feel near-impossible. Still, it's worth highlighting the benefit of doing so for those who can somehow squirrel some money away.

The world economy is increasingly succumbing to the threat of stagflation reminiscent of its 1970s ordeal, a mounting headache for global finance chiefs already navigating the fallout from the war in Ukraine.

Treasuries gained for a second day as investors sought out the safest debt, driving the 10-year yield down 11 basis points to 2.77%, it’s lowest level since late April. Weaker than forecast US jobless claims and a sharp decline in a regional Philadelphia Fed survey spurred a burst of buying in Treasuries, with equities futures indicating that stock prices will open lower.

The Twitter spat about taxes and inflation involving President Joe Biden, Amazon.com Inc. founder Jeff Bezos and former Treasury Secretary Larry Summers has served mainly to prove that Twitter is a bad place to attempt intelligent debate. Still, the point at issue matters. It deserves a slightly less abbreviated treatment.

The terms "value" and "growth" have been blurred. What appears to be a value stock may be in its reputation only.

I understand why some advisors won’t achieve the success they deserve.

Do we respect ourselves and our family members enough to treat them like they are our clients?

Is it odd some newer people would have such negative things to say about me?

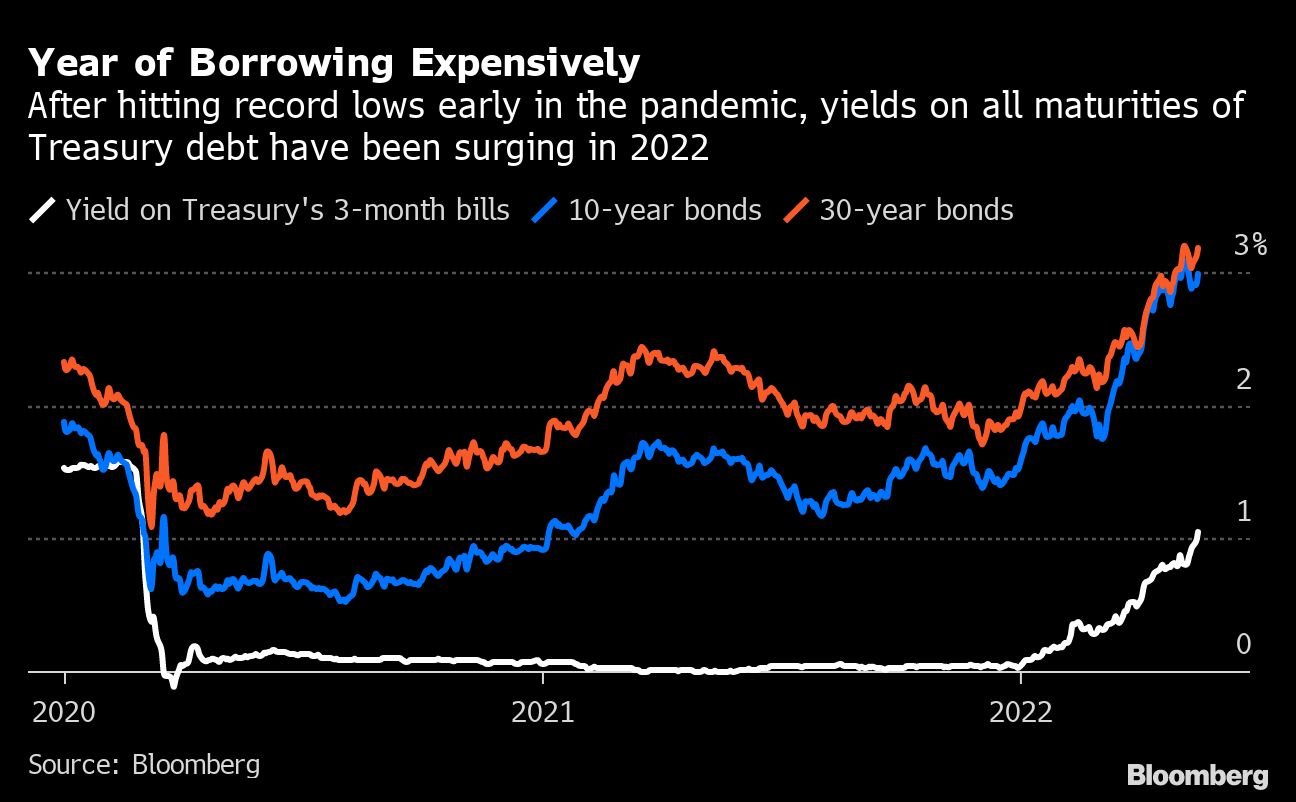

Like a supertanker, US debt-service costs only change course very slowly. But it’s happening now -- and from Washington’s point of view, the new direction is the wrong one: they’re heading up.

The world’s biggest retailer on Tuesday reported profit that fell short of Wall Street expectations and downgraded its outlook for full-year earnings per share from a mid-single digit increase to a 1% decline. Chief Executive Officer Doug McMillon said the bottom-line results were “unexpected” and reflecte the “unusual” environment. Walmart shares tumbled more than 11% on Tuesday, the most in 35 years.

Whenever I surf television cable news channels, I see the plethora of ads for financial planning. But they are run by companies that sell financial products or are owned by huge insurance companies.

The US economy won’t be able to avoid a bout of stagflation and markets have yet to tune into the risk of a significant slowdown in growth, said Mohamed El-Erian, the chair of Gramercy Fund Management and former chief executive officer of Pimco.

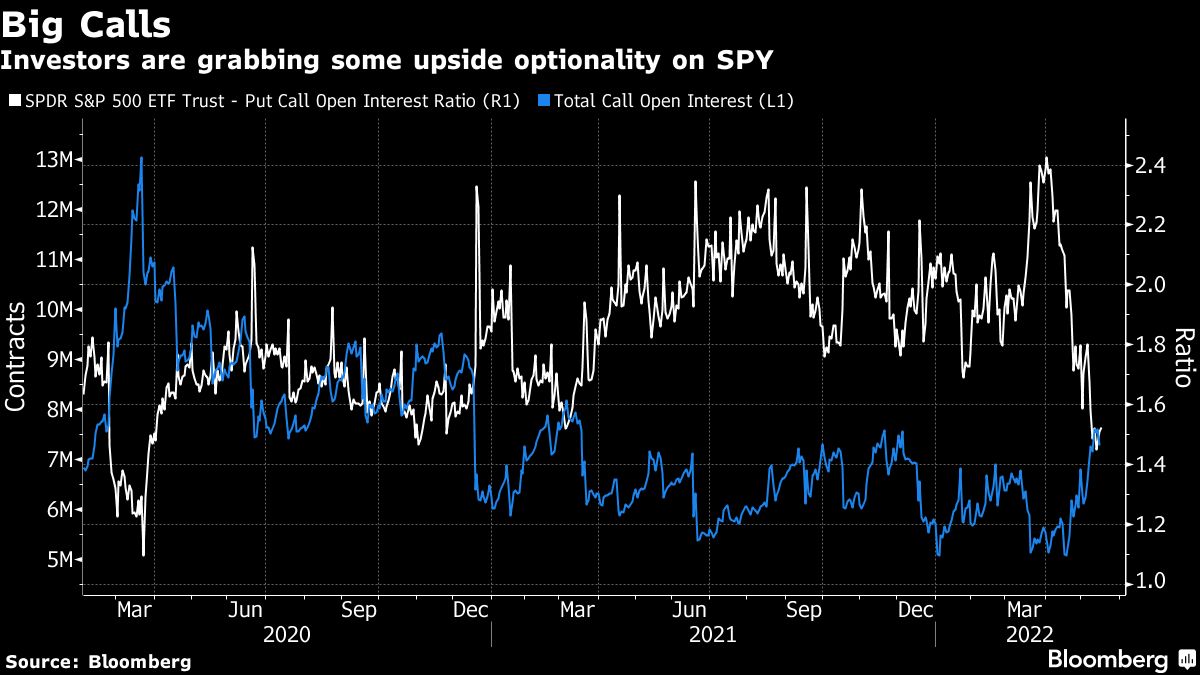

Bearish investors are snapping up bullish options to ensure that their defensively positioned portfolios won’t be left behind if the latest rebound in US stocks proves persistent.

Bitcoin is nursing a 21% loss so far in May -- the worst monthly slump in a year -- following last week’s crypto sector turmoil over the collapse of the TerraUSD algorithmic stablecoin, also known by its ticker UST, and Tether’s brief dip from its dollar peg.

Federal Reserve Chair Jerome Powell, in his most hawkish remarks to date, said the US central bank will keep raising interest rates until there is “clear and convincing” evidence that inflation is in retreat.

Plan for long-term Inflation that will be fought aggressively by the Fed, higher policy rates, and slower economic growth, according to Raghuram Rajan.

Advisors face an uphill battle to get attendance to their events.