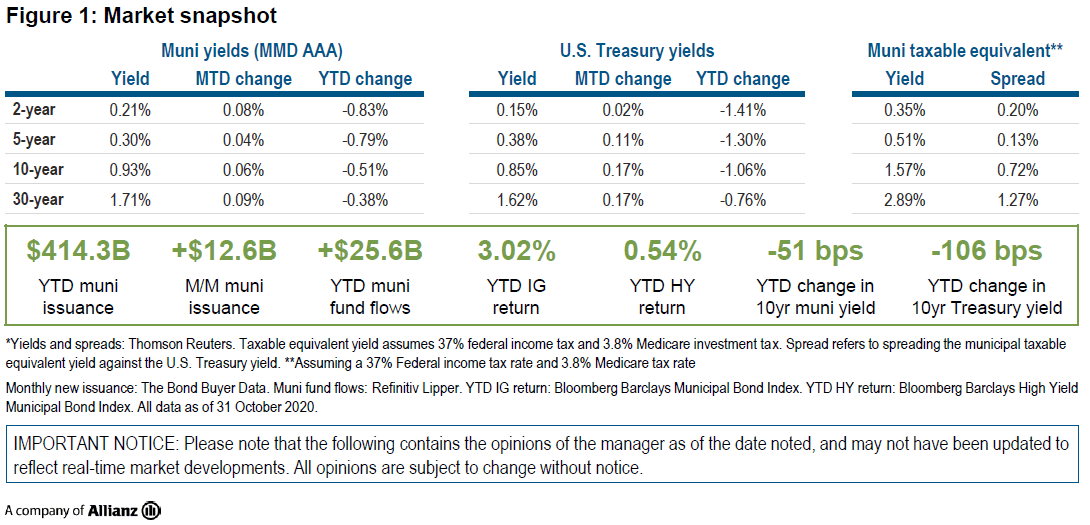

A brief monthly update on what's happening in the municipal bond market.

Washington will likely focus on fiscal stimulus immediately – but given the realities of governing and the pandemic, economic recovery will take time.

Bundling may help plan sponsors unlock alpha potential and supplement low returns from long Treasury bonds.

Conventional wisdom says urban residents will flee cities in droves in response to higher taxes and the COVID-19 pandemic. But will that really come to pass?

PIMCO’s Global Advisory Board discusses the longer-term outlook for major economies and geopolitical developments.

Canada’s central bank looks to evolve its policy framework amid concern over disinflationary trends.

The pandemic has amplified four long-term macroeconomic disruptors, and fiscal policy – a key swing factor – may hold the key to upside or downside surprises. Read our long-term outlook and learn implications to consider when investing.

Policy will continue to be carefully calibrated as China walks a tightrope between supporting growth and maintaining financial stability.

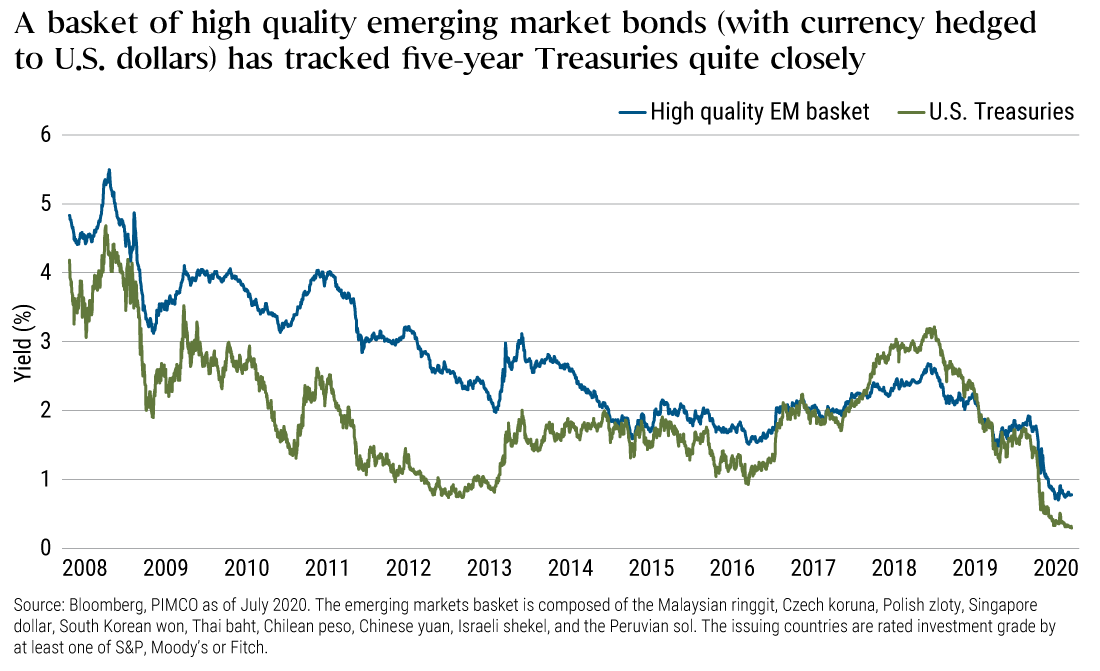

A basket of emerging market bonds may offer the same appeal investors have long sought from U.S. Treasuries.

Launched in September 2020, the CFO Principles for Integrated SDG Investments and Finance are designed to help create a market for corporate SDG (Sustainable Development Goal) investments.

We believe the Fed’s mortgage purchase program is helping to bolster economic activity, and accomplishing more than Treasury purchases alone.

The lack of market reaction suggests that many investors are not convinced that the Fed’s new guidance represents any material shift in policy.

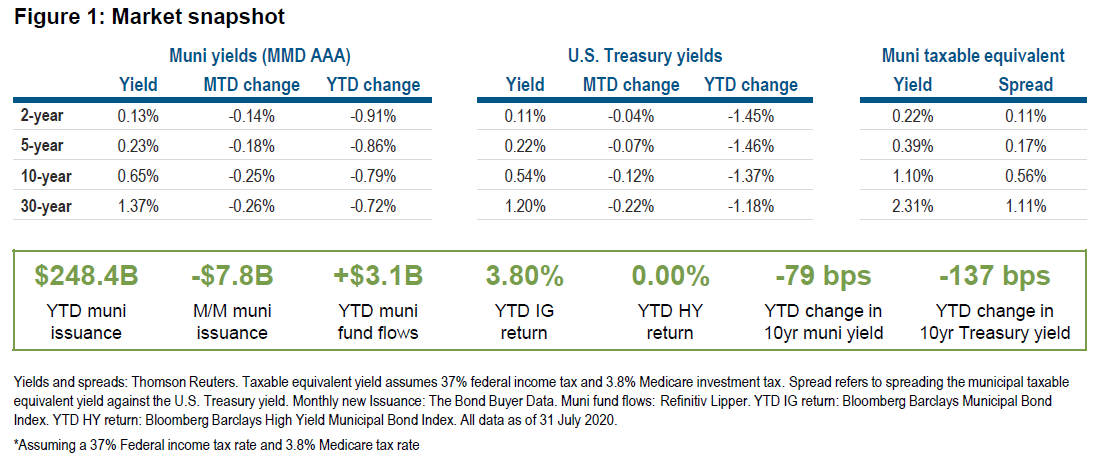

In a challenging year dominated by the COVID-19 pandemic, the municipal market is recovering on the strength of unprecedented federal support.

Resiliency and diversification potential remain critical in a world with meaningful uncertainty ahead.

Although the pandemic could make for a chaotic return to school, it is unlikely to create significant municipal credit stress.

The Federal Reserve released the results of its multiyear framework review alongside a speech by Fed Chair Jerome Powell at the Kansas City Fed’s Economic Policy Forum on 27-28 August. While the announcement came earlier than anticipated, the conclusions were in line with the evolutionary, not revolutionary, changes to the Fed’s framework we have long been expecting.

Despite reaching record highs earlier this month, gold remains attractively valued, according to our framework.

Research Affiliates discusses the increase in portfolio tactical shifts and recent research efforts supporting the All Asset strategies in today’s evolving investment environment.

Rising prices in July have led PIMCO to raise its core inflation forecast for 2020, but not 2021.

Looking across the global opportunity set, we see potential for attractive yield, though uncertainties surrounding the global recovery suggest this is a time to be cautious.

The Federal Reserve wants financial conditions to remain accommodative as it looks to support the U.S. recovery.

PIMCO’s CEO and its head of retirement outline the firm’s approach to generating retirement income.

European measures applied to mitigate the effects of the pandemic have contained the unemployment rate in Europe more than in the U.S. While recognizing economic risks from the rising number of COVID-19 cases in the U.S., our forecast sees this success ratio reversing before the end of the year.

Municipal bond investors will need to contend with the impact of monetary policy on market prices.

We expect more stimulus, both monetary and fiscal, will be necessary to support the recovery amid the renewed COVID-19 outbreak.

The protracted low-yield environment has left many investors with insufficient returns to meet their goals: how can credit help? Here we highlight where we see 5 credit opportunities.

After a decade of steady growth and rising asset prices, economies and financial markets were rocked by the COVID-19 pandemic. The global health crisis forced most governments to lock down their communities, halting economic activity almost overnight and causing financial markets to reprice lower at an unprecedented speed.

The health crisis creates opportunities to unite historically disparate investor groups to help build economic and market sustainability and resiliency.

The text book rules about where to invest following a recession may not apply in a post-pandemic world; more than bricks and mortar, stimulus efforts are green and digital now.

While a near-term mechanical bounce in economic activity in response to the lifting or easing of lockdown measures looks likely, we expect the subsequent climb up to be long and arduous.

We expect the Federal Reserve will continue to conduct asset purchases at its current pace through year-end, and eventually commit to keeping interest rates on hold through 2022. This should help ensure easy financial conditions and support the economic recovery.

Over diversifying an LDI manager roster may have important hidden costs.

This strategy aims to help investors participate in the ongoing recovery of the global economy, offering potential for attractive yield while managing downside risks.

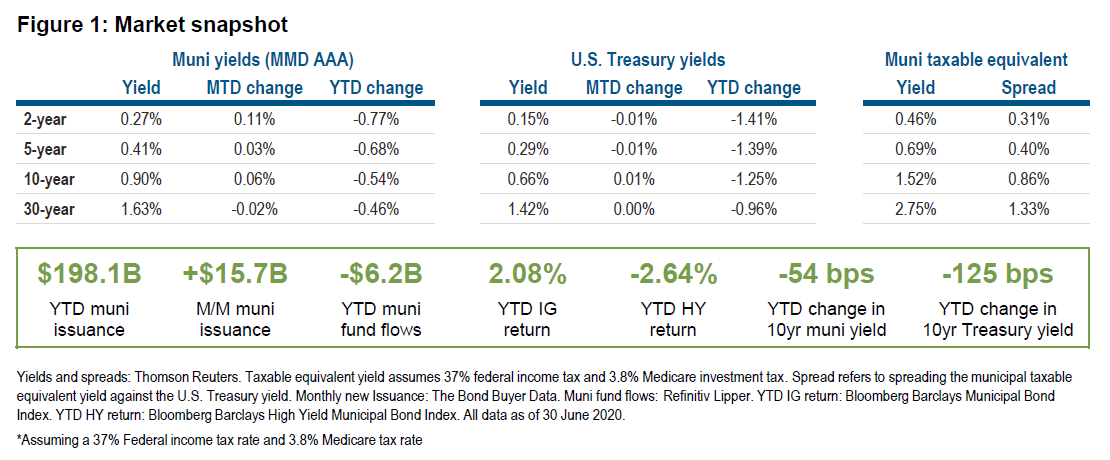

A brief monthly update on what's happening in the municipal bond market....

The COVID-19 crisis is likely to accelerate many underlying, secular disruptive forces already affecting economies and financial markets. This may only increase the difference between those companies, sectors, and countries that are being disrupted, and those that are acting more like disruptors. Distinguishing between the two is becoming crucial.

The U.S. political focus has shifted to the reopening of the economy.

Research Affiliates discusses how the All Asset portfolios seek to capitalize on opportunities amid pandemic-related market volatility and a strengthening U.S. dollar.

Weak technicals are creating an opportunity in long-duration municipal bonds.

Over the next several quarters, monetary conditions will likely be set not only by Fed balance sheet policies, but also by the expected path of interest rates.

Major economies are contracting, but extraordinary policy responses could limit severe recessions to this year.

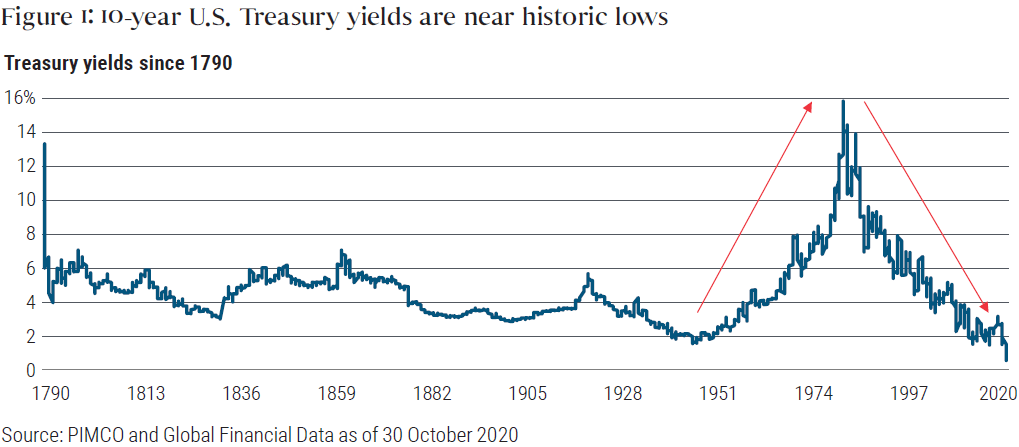

Evidence from decades and even centuries ago, plus the unique circumstances of the current global health crisis and its economic impact, suggests we can expect a “New Neutral 2.0” of lower interest rates for longer.

The U.S. labor market disruption is the worst the country has experienced in recent memory, suggesting that the decline in overall activity could also be much more severe.

The Fed has moved aggressively to stabilize core assets, including mortgages. Yet several market indicators are still concerning.