A Compelling Opportunity in Puerto Rican Bonds

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

A settlement has been struck that will give certain Puerto Rican bondholders 33% upside to today's trading – with much more potential upside than most observers appreciate.

This is a follow-up article to the blog posting we published on January 24th of this year where we encouraged readers to consider investing in subordinate (“junior”) Puerto Rico Sales Tax Revenue Bonds (also known as “COFINA”) when they were trading just under 15 cents per bond. The blog post can be found here.

Just over half a year later the same bonds are now trading around 45 cents on the dollar after, starting the year under 10 cents on the dollar and there remains substantial near-term upside to this trade.

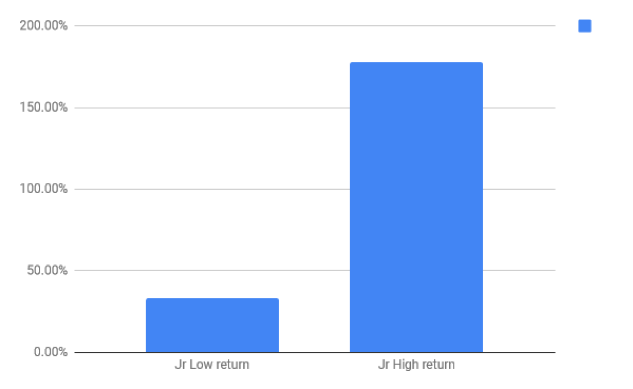

These bonds were and are trading “flat,” which means they are not trading with accrued interest of approximately 1.5 years that is currently in trust at Bank of New York. My firm’s analysis suggests junio COFINA bonds have additional, mostly near-term, upside of another 33% to as much as 180%. Though these bonds should only be considered by speculative investors, our research suggests a disproportionate amount of remaining upside for the chance of downside deviation from today’s market prices.

Our research suggests further upside to COFINA JR Bonds with returns of 33% to about 180% possible within the next three months with a relatively low likelihood of downside deviation.

Since our blog posting (which was our first public sharing of our research) the junior COFINA bonds have had a historic rally that is almost unheard of in the municipal bond market: up over 300% from that date. The most recent upward price movement happened after a settlement agreement was reached between most of the vested parties in the Commonwealth of Puerto Rico bankruptcy proceedings. According to our calculations, if the settlement is consummated on or about January 1, 2019, the net recovery on that agreement will be about 60 cents of par for the junior holders, an additional 33% upside to recent trades. However, we believe there is relatively low chances for downside deviation and much more upside than the market is currently pricing in. In fact, we believe there are several pathways that could lead to over 100% of par recovery (full par plus accrued interest already in escrow) for both junior and senior COFINA investors, which is closer to 200% returns based on recent trades. Because the junior COFINA bonds are currently trading for around 45 cents in odd lot quantities versus around 82 cents for senior issues, we favor the junior COFINA bonds at this time.

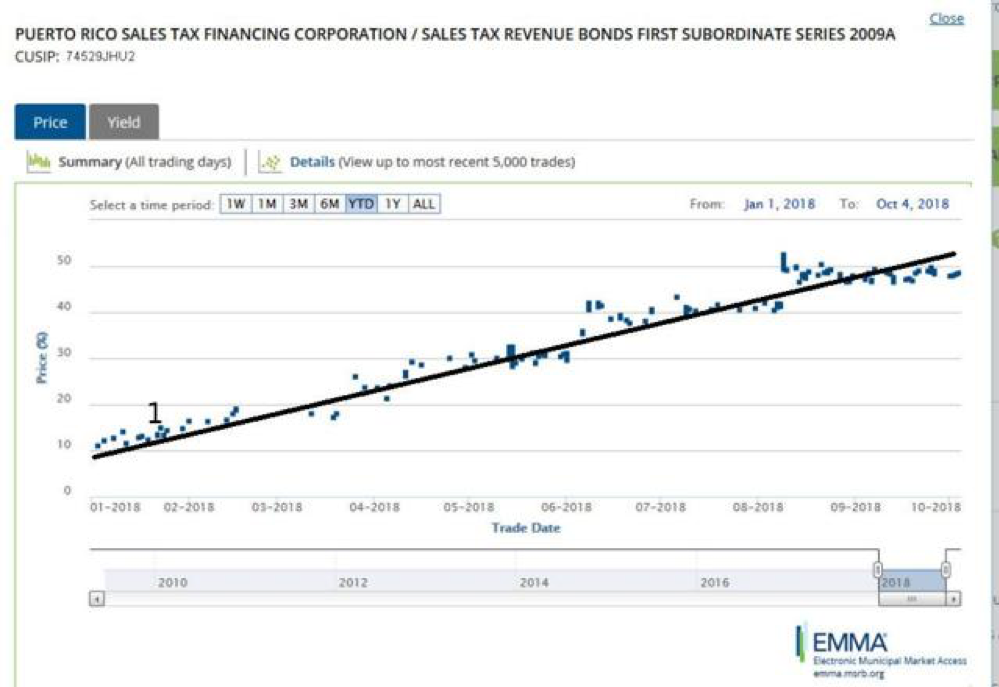

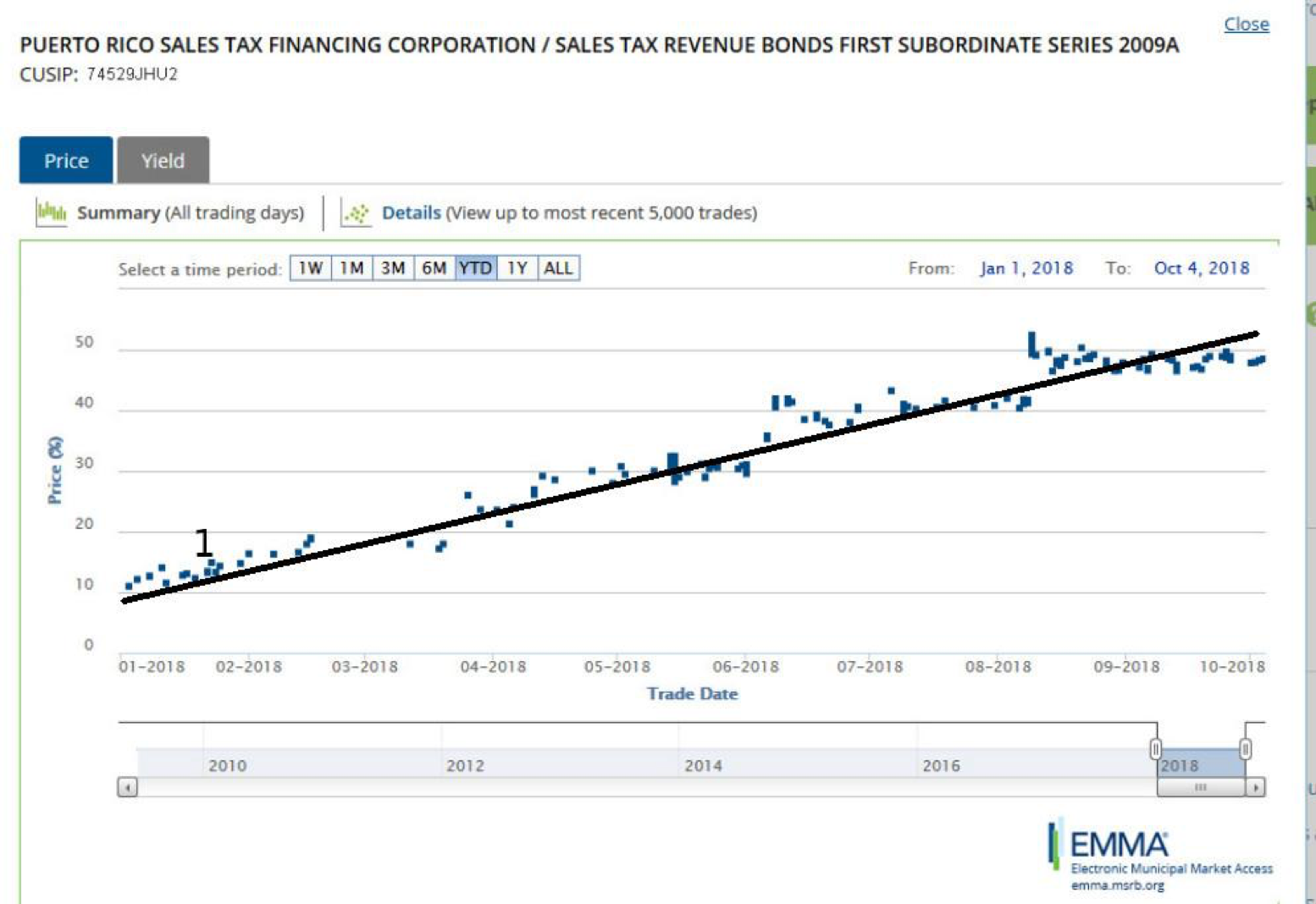

Graph of a junior COFINA bond price chart YTD

Source: emma.msrb.org “1” represents the approximate time and level of trading of our last Seeking Alpha posting (1/24/18 at around 14.2 cents).

We believe the 33% upside we calculate to be inherent in the existing agreement to be a relative baseline that is unlikely to be negotiated lower – and this (and potentially greater) upside shall be realized mostly between now and year end 2018.

How do we calculate about 60 cents (33%) minimum likely upside on junior COFINA coupon bonds?

The announced settlement of cash and new bonds was calculated as of August 1, 2018. According to the agreement principles, junior holders will receive 56.4 cents total consideration for each $1.00 of face value of each bond as of that date and will accrue additional interest at a blended rate of about 4.75% annually commencing on that date. For the purposes of simplicity we shall include the 2 cents additional the current proposal reserves for those voting “for” the reorganization (we intend to vote against the settlement and we believe all bondholders should be treated equally no matter how they vote), bringing the total is 58.4 cents. Assuming the 4.75% annualized is accrued on the 58.4 cents starting August 1, that would equal an additional 1.16 cents on January 1, 2019 for a total of 59.6 cents (rounding up to 60 cents).

Additionally the cash consideration would be tax free cash and the new bonds issued to replace the current issues are structured to achieve a rating of “AA.” We believe bonds with call protection for an average of 7 years, like those proposed, with “AA” rating quality and with the backing of the US Court proceedings would trade at a premium to par and therefore the net value to investors will likely be above 60 cents on the dollar – perhaps as much as 66 cents total value.

How could the recovery be greater than 60 cents on the dollar?

We see three different pathways junior COFINA investors could achieve a recovery rate greater than 60 cents on the dollar: 1) Judicial/political intervention 2) junior COFINA bondholders rejecting the settlement, and 3) a potential recovery from the U.S. Treasury for all losses.

Political or judicial pressure to increase the settlement offer

The only substantial difference between the senior and junior COFINA bonds is the senior issues get priority of payment in the event revenues for the COFINA structure are insufficient to meet principal and interest payments. Many do not realize that COFINA continues to be fully funded and solvent with the primary source of distress coming from a challenge to the entire COFINA structure that – in the unlikely event the structure was found to be invalid – would equally effect junior and senior COFINA investors. Therefore we believe if junior COFINAs are properly represented and fairly treated then a settlement agreement should allow for equal prepetition recovery claims with the exception of funds currently held at Bank of New York (“BONY”) which legally currently belong about 60% to JUNIOR COFINA trust accounts.

Per the current agreement both senior and junior COFINA recoveries are adjusted to reflect their essentially equal claim to resources then both shall receive a total of just over 70 cents (as of January 1) plus the accrued interest at BONY, which would provide a slightly higher than 77 cent average recovery for Junior holders and about 76 cents per Senior holders.

We do believe if the senior coalition must agree to treat the junior holders properly and fairly, they will fight for a greater settlement for all COFINA participants. We see the senior coalition as currently offering a settlement reflective of their confidence in the entire COFINA structure, with the chances of losing a court fight being only about 5%. As small investors and on-island (Puerto Rico resident) investors are disproportionately invested in Junior COFINA bonds there should be significant political backlash to improve the offer to not give what rightfully belong to junior investors to the vulture hedge funds who “negotiated” this bad deal for junior holders among themselves.

Junior COFINA holders may reject the current settlement offer

Despite the lopsided nature of the settlement agreement we believe it is unlikely the junior holders will vote to reject the offer. Why? Because it is common knowledge that junior lienholders almost always get a much smaller return in a distressed debt transaction. However due to the structure being solvent, in the COFINA matter there should be no difference between recoveries of the junior and senior tranches.

The biggest reason junior lienholders are unlikely to reject the offer is because of a stacked ballot box: The senior Bondholders Coalition and mono-line insurers purchased over a billion additional dollars’ worth of junior COFINA bonds for pennies on the dollar after the hurricane Maria ravaged the island. Senior bondholders purchased the junior bonds in transactions that some claim to have used confidential inside information and be improperly self-dealing (increasing political pressure for a more equitable deal).

Recovery of full par, plus accrued interest: is the U.S. government liable?

Finally, no matter what may be negotiated as a haircut for all COFINA (and other Puerto Rico bond investments), investors still have a chance to be made completely whole. There is already one lawsuit arguing the federal law Congress passed that enabled Puerto Rico to default on their bonds and go through a bankruptcy-like procedure, PROMESSA, may be unconstitutional for one of two reasons: unlawful impairment of contracts and improper takings without compensation of private property. There is no higher law of any land in the USA than the Constitution and it appears possible, perhaps probable, one or more of the tenants of this highest law were broken creating liability for the U.S. federal government.

We believe that no matter the outcome the sophisticated senior COFINA bondholder coalition will fight to try to recover full par plus accrued interest for both senior and junior COFINA investors – and we believe they have more than a remote chance of winning the suit. Therefore the upside of junior COFINA investors are full par ($1.00) PLUS all accrued interest which, as of January 1, 2019, will be almost two years of interest at approximately 6% average coupon, for approximately $1.12 recovery per 0.45 cent bond purchased today (and in any legal win there could be additional damages awarded). Additionally, if the COFINA structure is enforced by the U.S. court system or is upheld as legal by U.S. court system then the bonds would likely also trade at a substantial premium to full par – creating an ultimate recovery perhaps as high as $1.25. This means junior COFINA bondholders still have potential upside of as much as 180% from today's prices. Not bad.

What is the chance of an outcome of less than today’s 45 cents (or 60 cents per the settlement offer) on the dollar?

We believe the chances of junior COFINA investors receiving less than 60 cents at settlement is possible, though relatively remote. In the instance COFINA investors and other parties do not settle out of court and IF the court then finds the COFINA structure to be invalid then COFINA investors could become unsecured creditors which could lead to very low recoveries and substantial losses versus today's purchase price (albeit with a potential claim of fraud against the Commonwealth and it would likely be heard by the U.S. Supreme Court, first!).

Elliott Asset Management believes the initial settlement proposal that was rejected by the Oversight Board where GO (General Obligation/unsecured) investors would have received new COFINA bonds mostly from junior COFINA funds (even more unfair than the current settlement offer) demonstrates the GO owners ultimate confidence in the validity of the COFINA structure and it being superior to their GO claims (as represented by every major ratings agency and government of Puerto Rico statement from the date of the creation of COFINA in 2006, until only recently).

Despite our relative confidence in the substantial upside versus downside risk these are distressed bond debt investments and should only be considered by experienced fixed income investors after careful consultation with one's financial advisor and attorney. One should only invest money one can afford to lose as there is theoretically the chance of getting substantially decreased – or even zero – recovery.

Though we believe the likelihood of this to be less than the 5% of substantial downside (about what the senior bondholders are willing to give up to settle the matter) it is a possibility that cannot be ignored completely. Our speculative clients at EAM have been "all-in" on these bonds since the start of the year. However, we continue to buy whenever new funds are available. These bonds now make up about 50% of all the capital allocated in EAM separately managed accounts. Since the blog post in January we have only sold some insured bonds to pick up additional uninsured COFINA bonds (mostly junior with some senior acquired).

Risk to reward strongly skewed to the upside

We estimate the chance of junior Investors receiving at least 60 cents, based on the mostly subjective evaluation of our years of research before the current economic and natural disasters hit the island and our analysis of events subsequent to those events, to be in the vicinity of 95 percent (assuming no other unexpected disasters). The COFINA structure is solvent and has been continuously paying the proper and full amounts for all COFINA investors in escrow at BONY, as the original A+/AA- ratings (versus BBB- and eventual junk ratings of GO bonds) originally predicted would occur even under severely distressed conditions like we have recently experienced.

We believe speculative investors should carefully consider COFINA junior bonds at today’s prices at this time.

Mark Elliott is president of Boston-based Elliott Asset Management, a Registered Investment Advisor.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All