Retirees don’t like spending down their savings.1 Unfortunately, it has never been more expensive to buy income from a portfolio. Historically low interest rates coupled with declining dividend yields has created a significant dilemma for income investors.

Retirees don’t like spending down their savings.1 Unfortunately, it has never been more expensive to buy income from a portfolio. Historically low interest rates coupled with declining dividend yields has created a significant dilemma for income investors.

The average cost to generate $1,000 in income from a 50/50 balanced portfolio historically has been about $25,000. Today, $1,000 of income costs approximately $80,000 from a balanced portfolio and briefly exceeded $150,000 for bond investors in 2020. The rising cost of portfolio income is a global phenomenon.

In response to the low-yield environment, many investors will be tempted to reach for yield, either by purchasing lower quality bonds or equities with higher dividend yields. We demonstrate that these approaches will increase the risk of a portfolio with little expectation of reward through higher returns.

There is no easy answer for income investors whose expectations and behaviors need to be adjusted accordingly.

Living off yield

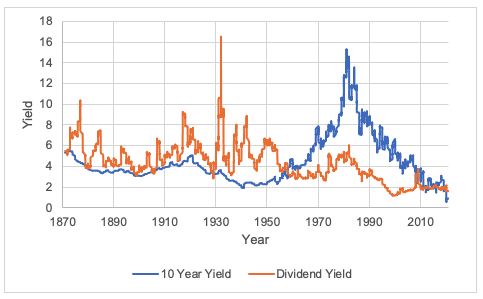

Yields on financial assets have plummeted. We document this effect for 10-year U.S. government bonds and large-cap equities from 1870 to 2020 below using data from Robert Shiller’s website.

Historical Yields

Source: Robert Shiller’s website

The average bond yield over the period was approximately 4.5% and the average dividend yield was 4.1%; at the end of 2020, these numbers stood at .9% and 1.6%, respectively.

What is most troublesome about the drop in yields is that they are taking place at the same time. Historically, periods of low dividend yields and or interest rates have cancelled themselves out some extent (i.e., when dividend yields were low, bond yields were high), and today both are well below long-term averages. Companies are increasingly using repurchases to return money to shareholders, which coupled with high equity valuations has decreased dividend yields globally, and bond yields have plummeted, in part from a flight to safety following the onset of the pandemic.

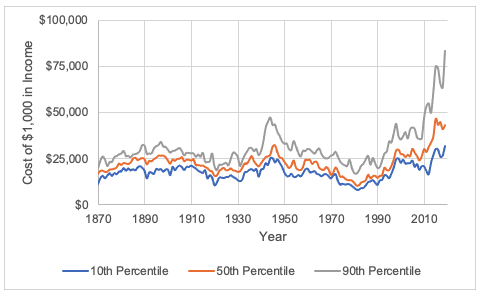

Not surprisingly, lower yields have a measurable impact on the income that can safely be generated from a portfolio. We demonstrate this by estimating how much it costs to generate $1,000 in income from a portfolio. The calculation is relatively straightforward; we divide $1,000 by the yield of the portfolio. For example, if portfolio is yielding 4%, the cost of $1,000 would be $25,000. For this analysis, we focused on a balanced portfolio with a 50% allocation to 10-year U.S. government bonds and a 50% allocation to large-cap equities.

The High Cost of Income

Source: Robert Shiller’s website, authors’ calculations

It has cost $26,267, on average, to generate $1,000 from a balanced (50/50) portfolio historically. This means an investor could expect a yield of roughly 4% from financial assets.

In contrast, as of January 2021, the cost of $1,000 increased to $79,118, down slightly from a peak of $83,889 in August of 2020. While this may seem high, the cost of $1,000 from 10-year government bonds peaked at over $150,000 in April 2020 when 10-year US government bond yields fell to .66%.

The increasing cost of income is not just a U.S. phenomenon. Bond yields have declined in many global markets more than in the U.S. and dividend yields are also below historical averages.

To provide some perspective on this effect, we repeat the previous analysis, where we estimate the cost of $1,000 in income from a balanced (50/50) portfolio but do so for 16 countries2 (leveraging the Jordà-Schularick-Taylor Macrohistory database, coupled with some additional sources for completeness). The exhibit below shows how the costs have evolved from 1870 to 2019.

Historical Cost of $1,000 in Income, 1870 to 2019: Distribution of International 50/50 Portfolios

Source: Jordà-Schularick-Taylor Macrohistory Database; Dimson, Marsh and Staunton dataset; OECD; MSCI; Morningstar, Authors’ calculations

The global average annual median cost of generating $1,000 from 1870 to 2019 has been similar to the U.S., coming in at $22,624. Like the U.S., though, the cost of generating income increased considerably in the last few years, with a median cost of $43,123 at the end of 2019. The costs will be notably higher when these figures are updated to include 2020 year-end values.

The cost of buying $1,000 of portfolio income in countries at the 10th percentile rose to $31,983 in 2019. Those countries with the highest sovereign bond yields and dividend income likely have a higher risk of default and fewer protections for equity investors. Yet, buying $1,000 of portfolio income costs more today at the 10th percentile than the average between 1870 and 1990 at the 90th percentile. An investor would need to take significantly more risk to achieve the same income as a high-quality portfolio could produce for much of the 20th century.

Reaching for yield in all the wrong places

Retirees are a behavioral bunch. Only 22% of retirees plan to spend down their financial assets, 32% plan on maintaining their financial assets by withdrawing only earnings, and 22% plan on growing their wealth. This approach is not realistic today.

Behavioral investors who want to cling to the notion that principal must be preserved will reach for yield by purchasing lower quality bonds or higher dividend paying stocks. Neither approach is likely to end well.

Reaching for yield in fixed income

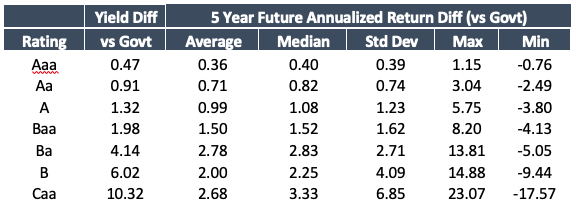

Yields on Treasury bonds are comically low… so why not invest in high-quality corporate bonds? And if you’re going to invest in corporates, why not go a few rungs down in credit quality to ratchet up returns? That 7%+ yield on Caa-rated bonds sure does look attractive!

Here’s the thing, though, when it comes to corporate bonds, higher yields don’t translate to higher returns. For example, since 1987the average yield spread between Caa-rated intermediate-term corporate bonds and Treasury bonds has been 10.32%.But Caa-bond investors have earned only 2.68% more over five-year periods. The additional volatility has also been intense. What gives? There’s a reason high yield bonds are also called “junk bonds;” defaults lower the realized return.

We demonstrate this effect below, where we include historical yield differentials for a variety of Bloomberg Barclays Intermediate Credit indices versus the Intermediate Government index. The analysis uses rolling monthly returns from February 1987 to December 2020, the longest period of returns available for all series, and all returns are annualized future five-year values.

Historical Yield and Return Spreads for Bloomberg Barclays Intermediate Credit Indices versus Intermediate Government Bonds

Source: Morningstar Direct, Authors’ calculations

For lower rated bonds, investors haven’t achieved higher realized returns despite the higher yields. The difference between the yield and average/median returns is largely attributable to defaults, which is why the differential increases as credit quality declines. Risk (volatility) increases considerably; Caa bonds have had a higher return than Aaa bonds, their standard deviation has been more than 17-times greater.

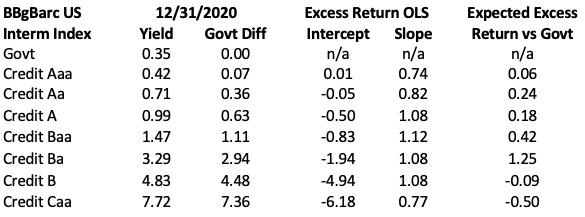

We can use the information about the historical yield and returns relations to estimate what the expected excess returns versus government bonds will be as of 12/31/20, based on a series of ordinary least-square regressions. We include the results of the analysis below.

Expected Excess Return of Credit Indices as of December 31, 2020

Source: Morningstar Direct, Authors’ calculations

The far-right column is the key result, i.e., the expected excess return for corporate bonds versus government bonds. For example, A-rated bonds have a yield spread today of 63 basis points and their estimated realized return has been -50bps + 1.08 * 0.63 (the spread today) = 18 bps.

The most attractive category is Ba-rated bonds, which have a spread of 2.94% over Treasury securities. But the realized difference is likely to be only 1.25%, given the historical data; however, that difference is mostly noise within the model. The expected return differentials are generally less than 50 bps and the credit spreads aren’t large enough to make moving away from government bonds all that attractive, at least given the historical realized returns.

High-yield bonds have also historically looked a lot more like equities, with average equity correlations of 0.6 to stocks; they provide only modest diversification in addition to their extra risk.

Reaching for yield in equities

Another approach to increase income is stocks with higher dividend yields. An important question, then, is how have stocks with higher dividend yields performed historically? We conducted an analysis looking at U.S. open-end mutual funds classified as large value as of January 17, 2020. We used only the oldest share class to represent each fund and included funds that have failed (i.e., the dataset is survivorship-bias free). We have data on dividend yields for funds beginning at the end of 1999.

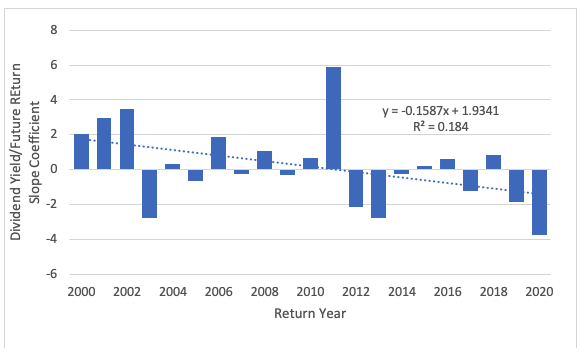

We ran a series of ordinary least-square regressions, where the dependent variable is the calendar year return for the fund and independent variable is the dividend yield at the end of the previous year. We ran the regression each year from 2000 to 2020 (for a total of 21 regressions). The exhibit below shows the slope coefficient from each regression.

The relation between dividend yields and fund returns

Source: Morningstar Direct, Authors’ calculations

A positive slope means funds with higher dividend yields had higher returns (outperformed), while a negative slope implies the opposite.

The results of our analysis show that large-value funds with higher dividend yields have significantly underperformed in three of the last four years and that this underperformance is part of a longer trend over the last 21 years.

While we don’t know why this effect exists, we can speculate: Dividends were in short supply and were overbought. While you can still “buy” dividends, there is an increasing cost associated with doing so. Not exactly exciting prospects either – especially when dividend income taxes are likely to increase for higher-income Americans.

When thinking about investing in equities it’s important to consider valuations. While dividend yield has historically been used as a valuation metric, it’s not as reliable as it used to be given the rise of buybacks. Other valuation metrics, such as the CAPE ratio, suggest that markets are relatively expensive. This makes investing in equities for income purposes riskier relative to bonds.

Conclusions

“Unprecedented” was the buzz word of 2020. But the yield/income environment is unprecedented, since investors face the highest cost of income since 1870. This high cost is not just a U.S. phenomenon, so reaching for portfolio income in global markets is also far more expensive.

Evidence from past returns shows that reaching for additional yield by investing in lower quality bonds or higher dividend stocks entrails greater risk with little expectation of reward through higher returns.

Viewing one’s principal as untouchable and spending only income is a behavioral mistake. Rationally, one should focus on maximizing the after-tax return from the portfolio. Therefore, advisors – especially those serving retirees – need to acknowledge the danger of trying to eke a few more dollars of income from their portfolio by reaching for yield in bonds or equities, and help their clients accept that liquidating capital may be the only way to meet their lifestyle goals.

David M. Blanchett, Ph.D., CFA, CFP®, is head of retirement research for Morningstar’s Investment Management group and an Adjunct Professor of Wealth Management at The American College of Financial Services.

Views expressed are his own and do not necessary reflect the views of Morningstar Investment Management LLC. This blog is provided for informational purposes only and should not be construed by any person as a solicitation to effect or attempt to effect transactions in securities or the rendering of investment advice.

Michael Finke, PhD, CFP®, is a professor of wealth management and the Frank M. Engle Distinguished Chair in Economic Security at The American College of Financial Services.

1 For example, Michael Finke conducted a survey in 2015 and found only 14% of retirees were comfortable with the idea of seeing their savings decrease to meet lifestyle goals.

2 Australia, Belgium, Denmark, Finland, France, Germany, Italy, Japan, Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, UK, and the US

More Fixed Income Topics >

Retirees don’t like spending down their savings.1 Unfortunately, it has never been more expensive to buy income from a portfolio. Historically low interest rates coupled with declining dividend yields has created a significant dilemma for income investors.

Retirees don’t like spending down their savings.1 Unfortunately, it has never been more expensive to buy income from a portfolio. Historically low interest rates coupled with declining dividend yields has created a significant dilemma for income investors.