Misestimating the age at which Social Security benefits exceed foregone earnings will cost clients tens or even hundreds of thousands of dollars in retirement wealth for at least three important reasons. A breakeven analysis does not consider the value of income in the more distant future. Future income is more valuable in a low-yield environment to higher-income clients who are more likely to be alive. It frames the failure to recover foregone benefits as a loss, which could trigger an emotional client response that favors early claiming. Third, it forces clients to estimate their own longevity – which many Americans cannot do.

Misestimating the age at which Social Security benefits exceed foregone earnings will cost clients tens or even hundreds of thousands of dollars in retirement wealth for at least three important reasons. A breakeven analysis does not consider the value of income in the more distant future. Future income is more valuable in a low-yield environment to higher-income clients who are more likely to be alive. It frames the failure to recover foregone benefits as a loss, which could trigger an emotional client response that favors early claiming. Third, it forces clients to estimate their own longevity – which many Americans cannot do.

The failure to maximize the net present value of Social Security income is the equivalent of a loss in retirement wealth. Claiming too early is economically equivalent to delaying claiming, withdrawing $100,000 from a portfolio, and setting it on fire. Claiming at a suboptimal age will result in less money to spend in retirement and less wealth passed on to beneficiaries.

Pricing annuities: Expected longevity and interest rates

Delayed claiming of Social Security income benefits is a decision to forgo a year of income to receive more income every year in the future. Delayed benefits are an investment. A 67-year-old retiree who gives up $25,000 of income in her 67th year will receive an additional $2,000 in inflation-protected income for life starting at age 68.

If trading a lump sum today for a stream of future income sounds like buying an annuity, it is. This makes it easy to estimate the net present value of delayed claiming by comparing the premium payment to the cost of creating a fairly priced (zero-profit) annuity.

Actuaries need two pieces of information to price an annuity – the expected longevity of annuity buyers and interest rates on bonds that fund future income payments. Annuities are more expensive when interest rates are low and when annuitants live longer. Today, real rates are negative and higher income Americans have gained roughly five years of longevity over the last 20 years.

The 1983 Amendments to the Social Security Act gradually increased full retirement age to 67 for those born in 1960 or later. This created a modest adjustment for anticipated improvements in longevity. But longevity increases have not been uniform among Americans, and this has a big impact on the value of delayed claiming.

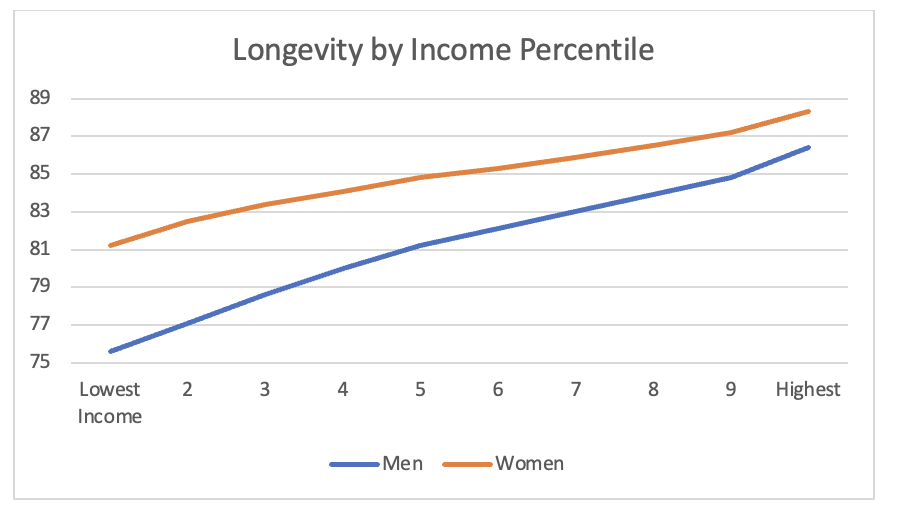

Planning clients live longer than the average American

According to data compiled by the Harvard’s Opportunity Insights policy initiative, the disparity in longevity between lower-income and higher-income Americans has widened since 2001. This is especially true for higher-income men, who have made the most significant gains in longevity in recent decades. Barry Bosworth of the Brookings Institution estimated that men in the top decile of income gained 5.9 years of longevity in a recent 20-year period.

Data: https://opportunityinsights.org/data/

Financial planning clients are most likely in the top decile of earners. They will live longer than the average American.

Imagine that a healthy, higher income 65-year-old retiree is sitting on a nest egg and needs to toss bricks of cash to the future version of herself to pay for spending at a given age. When she tosses $20,000 today to the 85-year-old version of herself, she has a 74% chance of being alive the catch the money. The present value of this payment is 74% of the brick of cash today.

Inflation-protected future income is valuable

How much cash is needed to fund $2,000 of inflation-adjusted spending in 20 years? On June 18, 2021, the discount rate on a 20-year inflation-adjusted payment from the federal government (TIPS) was -0.38%. The present value of the future inflation-protected $2,000 payment is $2,158. Multiply this by the 74% chance she’ll be alive to spend the money and the present value of this payment is $1,597.

I am sympathetic to advisors who believe that using a negative real rate to discount future cash flows is overly conservative. But that is the market price. Advisors measure a client’s wealth using the current price of stocks and bonds. They should measure the wealth of guaranteed future cash flows using current prices. Using the 20-year Treasury nominal discount rate of 2% may be appropriate for a nominal cash flow, but future Social Security payments will grow over time and investors place an insurance value on an asset that pays more when prices rise. The credit premium for corporate bonds is near zero at today’s credit spreads, so the opportunity cost of investing the foregone income payment is not the current yield on bond investments.

Using a discount rate that incorporates a risk premium is not appropriate for guaranteed future Social Security cash flows. It is also appropriate to consider the increase in wealth from delayed claiming as part of a client’s fixed income portfolio. A client who increases their Social Security income through delayed claiming should correspondingly hold a higher allocation of equities in their investment portfolio.

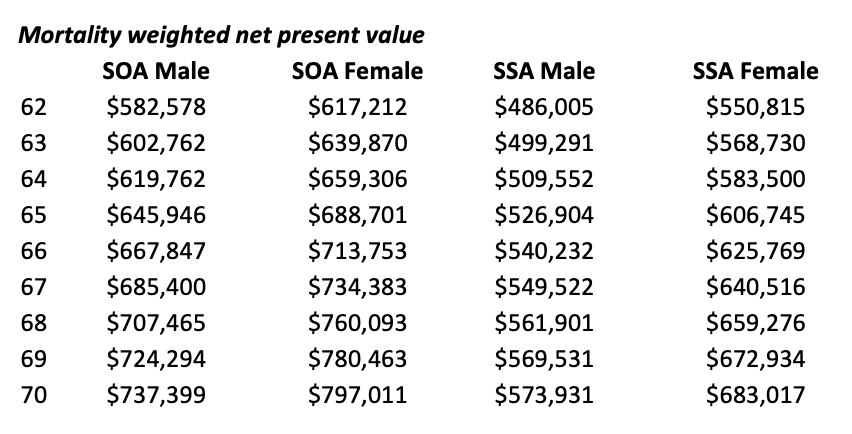

The following table shows estimates of the total wealth value of Social Security benefits discounted at today’s TIPS rates for a high-income worker (born in 1960, $100,000 average earnings) from my recent study to be published in the Journal of Financial Services Professionals, co-authored with Sophia Duffy of The American College and David Blanchett of PGIM. We provided estimates for men and women using the 2012 Society of Actuaries (SOA) annuity mortality table adjusted for improvements in 2021, and the 2017 Social Security Administration (SSA) mortality table. The SOA table is appropriate for healthy Americans who buy annuities and hire financial advisors. The SSA table is appropriate for a client who is as healthy as the average American.

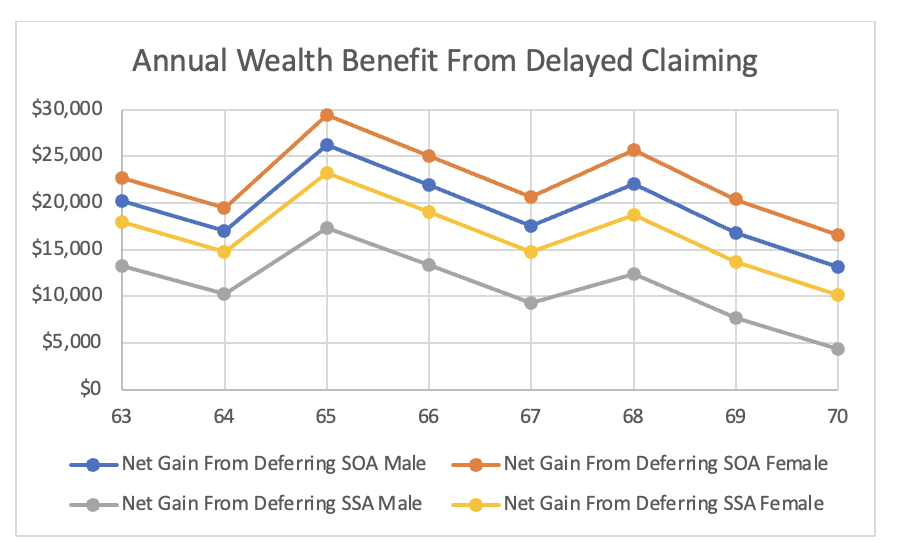

A keen reader will notice that the incremental increase in wealth from delayed claiming is not the same each year. This is because the Social Security administration uses a shortcut to estimate the actuarially appropriate increase in income from delayed claiming. For example, a retiree gets an 8% boost when delaying from 67 to 68, from 68 to 69, and from 69 to 70. The present value of the income increase is greater at age 68 than at age 70 because she pays the same price for an income annuity despite having more expected years to receive benefits. Using the same 8% rate may be simple but it is not actuarially accurate. Retirees get a bigger boost in wealth by waiting until the age at which the rate of income increase is higher (for example by delaying from 64 (5%) to 65 (6.66%) or from 67 to 68).

Healthy retirees (the SOA data) get the biggest benefit from delayed claiming, but even average-health women can increase their wealth by $132,202 by delaying from 62 to 70. Delayed claiming is especially valuable for women because they live longer than men, and wives out-earn husbands in about 30% of married couples today.

We conducted additional analyses in the paper that estimated the wealth impact of a 1% and 2% increase in real TIPS yields, as well as a 21% cut in benefits (possible but highly unlikely before 2026). With a 21% benefit cut and today’s low yields, using either mortality table, all cohorts would see an increase in expected wealth from delayed claiming to age 70. Even at 2% higher TIPS yields, the wealth benefit persists. Neither a benefit cut nor reasonably higher discount rates negates the benefit from delayed claiming.

Breakeven age: People are bad at predicting longevity

In the first example, a 67-year-old woman can increase her income by $2,000 per year by deferring $25,000 of Social Security income. She will break even in her 79th year at today’s TIPS discount rates. She’ll break even at 82 if she uses a 2% (real) discount rate (which does not exist in today’s market). Since a healthy woman has a 77% chance of being alive at age 79, she’ll accept the deferral if she has an accurate understanding of her expected longevity.

Unfortunately, many Americans are bad at estimating the chance they’ll be alive at older ages. It is common to use easily accessible information such as how long one’s parents or grandparents lived. Of course, longevity is subject to idiosyncratic factors, and advances in medicine and significant changes in behavior (such as not smoking) mean we’re all living longer than previous generations.

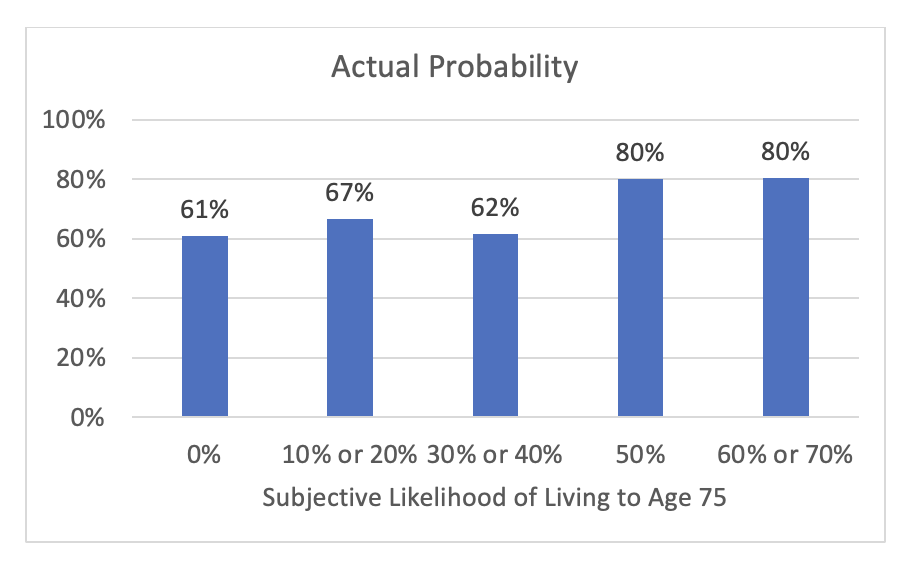

In the Health and Retirement Study, a panel study of 20,000 older Americans administered by the University of Michigan, respondents are asked about the chances that certain events will happen. Using a scale of 0 (absolutely no chance) to 10 (absolutely certain), respondents were asked to estimate the chance they will live to the age of 75.

We reviewed a sample of 61-year-old respondents who were asked this question beginning in 1990 when there was enough data to establish whether the respondent lived to age 75 (the survey data runs through 2018). Of those who believed that they had “absolutely no chance” of living to the age of 75, 61% ended up celebrating their 75th birthday. More than two thirds of those who believed they had between a 10% and 20% chance of living to the age of 75 ended up living beyond the age of 75.

Source: 1990-2018 Healthy and Retirement Study, Calculations by David Blanchett

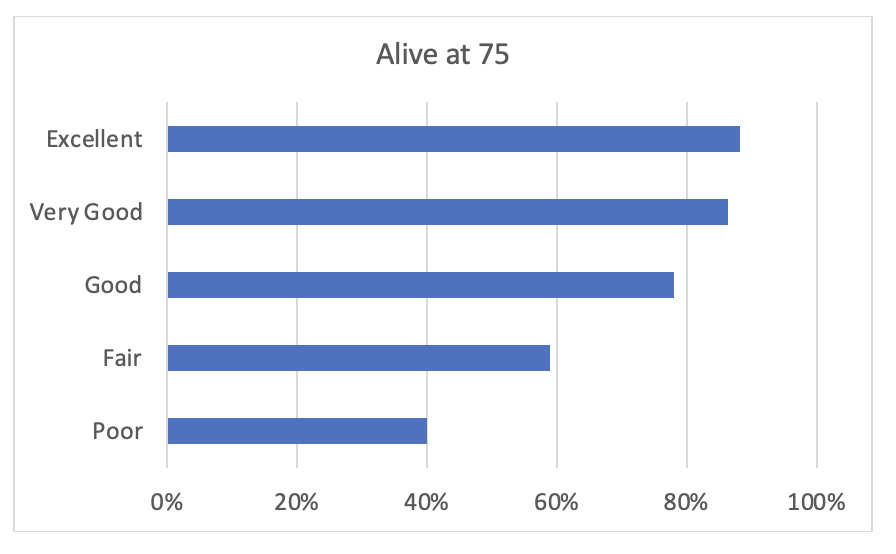

Although many held exceedingly pessimistic opinions of their expected longevity, people weren’t terrible at evaluating their own health. Those who indicated that they were in “excellent” or “very good” health at age 61 were more than twice as likely to live to the age of 75 (88% and 86%, respectively) than those who indicated that their health was poor (40%). Even those who were just in average (good) health had a 78% chance of living to age 75.

Source 1990-2018 Healthy and Retirement Study, Compiled by David Blanchett

If an advisor asks their client to rate their overall health, their response is a surprisingly effective indicator of expected longevity. Clients who are in fair or poor health are less likely to benefit from delayed Social Security claiming. However, in today’s low-return environment, clients who say they’re in good, very good, or excellent health are likely to be among those who receive a positive NPV from waiting to claim until age 70.

Breakeven age: Loss aversion and government distrust

Estimating the tradeoff of delayed claiming using a breakeven analysis creates a simplified frame of reference that can trigger an emotional response to loss. The retiree who delays claiming from 67 to 68 will lose if they don’t live to age 80. If they live beyond age 80, they win. But the perceived emotional gain from winning is less than the perceived loss from failing to recoup the income given up. Clients, particularly those who are loss averse, will prefer taking the money now.

Of course, economic models predict that those who are risk averse will place an even greater value on the lifestyle security provided by a guaranteed, inflation-protected lifetime income. Behavioral risk preferences damage the claiming decisions of those who would benefit the most.

Compounding the behavioral response to loss is the stubborn distrust of government institutions among many clients. They don’t believe that the government will make promised future Social Security payments, so they mentally discount those cash flows – especially those they won’t see for another 20 years.

As we’ve seen through the pandemic, many people have a difficult time clinging to objective reality (such as the failure to follow objective medical advice) when it deviates from their desire to maintain behavior consistent with a political tribe. Advisors who face emotional resistance to claiming Social Security early need to develop language that can help guide clients toward making better choices.

One approach is to guide clients away from the possible loss of legacy if they don’t live long enough to recoup deferred income. Will your beneficiaries care if they don’t get the extra $20,000 if you die at age 70? If the client is wealthy enough to see an advisor, probably not. They will care if assets dwindle in old age or from prolonged long-term care expenses. Creating a higher, inflation-adjusted lifetime income protects a legacy when a client needs it the most.

A second approach to countering opinions about Social Security solvency is to remind clients that they will receive 80% of their promised income in the worst-case scenario. Social Security payments come from payroll withdrawals; as long as Americans work, they’ll receive income payments. Do they believe that Americans will stop working (if they do, we’ll all have bigger problems..)? Have they ever heard of a politician who got reelected after cutting Social Security? The most likely scenario is some combination of higher taxes and more modest inflation increases (such as a chained CPI). In either scenario, the client will still be better off waiting until age 70 to claim Social Security.

Finally, delaying Social Security is the best way to create opportunities to pull assets out of IRAs to fund spending before age 70. This can reduce the amount of savings subject to RMDs and give the client greater tax flexibility. Positioning deferral to reduce taxes can help push even the most anti-government client to consider the appeal of delayed claiming.

Michael Finke, PhD, CFP®, is a professor of wealth management, WMCP® program director, and the Frank M. Engle Distinguished Chair in Economic Security at The American College of Financial Services.

Misestimating the age at which Social Security benefits exceed foregone earnings will cost clients tens or even hundreds of thousands of dollars in retirement wealth for at least three important reasons. A breakeven analysis does not consider the value of income in the more distant future. Future income is more valuable in a low-yield environment to higher-income clients who are more likely to be alive. It frames the failure to recover foregone benefits as a loss, which could trigger an emotional client response that favors early claiming. Third, it forces clients to estimate their own longevity – which many Americans cannot do.

Misestimating the age at which Social Security benefits exceed foregone earnings will cost clients tens or even hundreds of thousands of dollars in retirement wealth for at least three important reasons. A breakeven analysis does not consider the value of income in the more distant future. Future income is more valuable in a low-yield environment to higher-income clients who are more likely to be alive. It frames the failure to recover foregone benefits as a loss, which could trigger an emotional client response that favors early claiming. Third, it forces clients to estimate their own longevity – which many Americans cannot do.