Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Tax implications of withdrawals across multiple accounts is a top-of-mind issue for those planning for retirement. Advisors can ease this concern by providing a holistic retirement income plan including tax-smart strategies such as capital gains management and tax-targeted qualified disbursals (TQDs). While an individual is working, taxes are primarily determined by their salary with only minor control by an advisor. However, once they transition into retirement, their advisor becomes a tax conductor, orchestrating timing and sourcing of cash flows and disbursals to maximize their safe, post-tax spending.

In his article, Pay Attention to Marginal Tax Rates and Not Tax Brackets, William Reichenstein went into extensive detail about the tax effects of the Social Security multiplier and IRMAA on an additional dollar of taxable income from qualified retirement accounts, often referred to as tax-deferred accounts (TDAs). In this article, Reichenstein pointed out the flaws of relying on the posted marginal rates of tax brackets, introduced improvements to the framework of tax-efficient withdrawal strategies, and contrasted his work to that of other notable researchers: Ed Slott, Michael Kitces, and Wade Pfau.

The focus of Reichenstein’s article was decisions regarding TDAs: whether to make a Roth conversion, whether to save into a TDA or Roth account, and how to tax-efficiently withdraw funds from TDAs. For this article, I will focus on the first and third decisions, making withdrawals from TDAs throughout the year to fund retirement income and discretionary Roth conversions at the end of the year.

The framework proposed by Reichenstein includes considering four factors when making those questions: 1) Will the Roth conversion increase taxes in the current tax year?; 2) Will the Roth conversion increase Medicare premiums in two years?; 3) What will be the impact on taxable income in the future?; and 4) What will be the impact on Medicare premiums in the future? Reichenstein pointed out that this framework ignores the effects of capital gains taxes, which he explained with an assumption that most clients of advisors will be paying the 15% capital gains tax.

As Pfau posted in a response to Reichenstein, and agreed to by Kitces researcher Derek Tharp, this framework is not new, and the term marginal tax rate management may be confusing to the average retiree. This was further reiterated by Pfau in Tax-Efficient Retirement Distributions with Inheritance in Mind, where he clarified that his framework already uses the ideas described by Reichenstein and that the primary objection is to the term tax-bracket management when “including non-linearities in the tax code that cause marginal tax rates to [be] different from the federal tax brackets for ordinary income.” While making withdrawals across a household’s non-qualified taxable accounts, qualified TDAs and Roth tax-free accounts, it is important to consider the cumulative tax effect of realizing gains and increasing taxable income, both in this tax year and throughout the retirement horizon.

Income Discovery’s AI engine AIDA incorporates dynamic, tax-efficient withdrawal strategies, Roth conversions, and capital gains management into a personalized, optimal, holistic retirement income plan which is managed and monitored through its ”paycheck” capability. However, while tax efficiency is an important aspect of planning, simply minimizing taxes should never be the end goal of a retirement income plan. In fact, a household can often have a higher and safer post-tax income by making decisions that could increase their cumulative taxes across the horizon of the plan.

While I agree with Reichenstein that a framework of best practices is required for the industry to make informed decisions regarding withdrawals from TDAs and that his framework is asking relevant questions, he fails to fully evaluate the decisions. Retirement income plans need to be evaluated holistically, with discretionary tax-targeted qualified disbursals and capital gains management evaluated as part of the plan. When a household claims Social Security, how much of their assets are annuitized, their base level of taxable income, and other factors go into determining the optimal tax strategy for that household. There is no generic solution that works across all households.

Regarding TQDs specifically, it is important to distinguish withdrawals for income throughout the year without full tax information where assumptions about taxes need to be made from Roth conversions at the end of the year when full tax information is known. To perform TQDs, there needs to be a targeted incremental average tax rate on the disbursals. Reichenstein highlighted why filling a federal tax bracket is not the answer and that the marginal rates (MTRs) within the brackets of a given year must be considered. Software like Income Discovery can evaluate multiple target tax rates to find the optimal target for a household in conjunction with all other strategy levers instead of evaluating each decision in isolation.

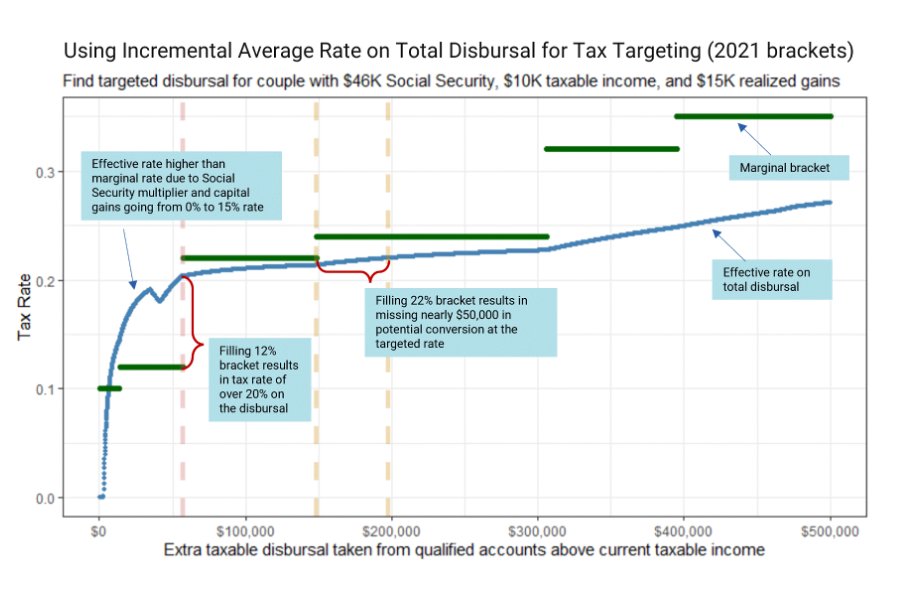

Figure 1: Targeting Incremental Average Tax Rate vs. Filling Marginal Brackets

Of the three primary factors impacting the marginal rates in the federal tax brackets to create the MTRs Reichenstein discussed, the most impactful for most retirees are the Social Security taxable portion and the capital gains rate. Reichenstein dismissed the capital gains rate and instead focused on Medicare premiums.

Most people do not go beyond the standard Part B premium. In 2019, only 7.5% of people enrolled in Part B paid premiums above the base premium1. Even going up one or two brackets may not be a significant part of the decision. Even a couple with MAGI at the top of the base premium ($176,000 in 2021) converting $100,000 from TDAs to Roth accounts will jump two brackets and may only have a $3,564 increase in premiums in two years if cutoffs don’t increase. If this household had $50,000 in taxable income with $126,000 in capital gains and hasn’t claimed Social Security yet, that same $100,000 increase in taxable income would result in nearly $25,000 in additional taxes (including an addition of nearly $9,000 of capital gains tax) assuming both are over age 65 and receiving the standard deduction. All these factors should be taken into consideration when evaluating the decision.

The tax on each additional dollar of taxable income should not be the focus. The important factor is the effective tax rate paid on the entire discretionary disbursal. For example, for someone with capital gains at the 0% rate and Social Security benefits that are less than 85% taxable, one dollar from their TDA could cause an extra $0.85 taxable Social Security income, as explained by Reichenstein. This could, in turn, move $1.85 from 0% capital gains to 15% capital gains. Finally, that $1 could theoretically push them from base Part B premiums to the next bracket. To take that $1 from their TDAs, they end up paying $0.4995 in taxes this year, a 50% effective tax rate, plus an additional $1,425.60 in Part B premiums in two years due to the two-year look back for determining Medicare premiums.

However, nobody is withdrawing or converting only $1 from their TDAs. Across the entire disbursal, they may end up paying a 22% incremental average tax rate (see figure 1), which could be the optimal target for the household. Over the 30- to 40-year retirement plan, the taxes paid on each individual dollar are not going to be impactful, but targeting an incremental average tax rate on the cumulative discretionary disbursals each year in coordination with other dynamic, tax-smart strategy levers will lead to an increased safe post-tax income2 for the household. Additionally, this is easy to explain to the client with, for example, $10,000 of TQD and a 16% incremental average tax rate meaning the client will pay $1,600 in additional taxes solely because of the TQD.

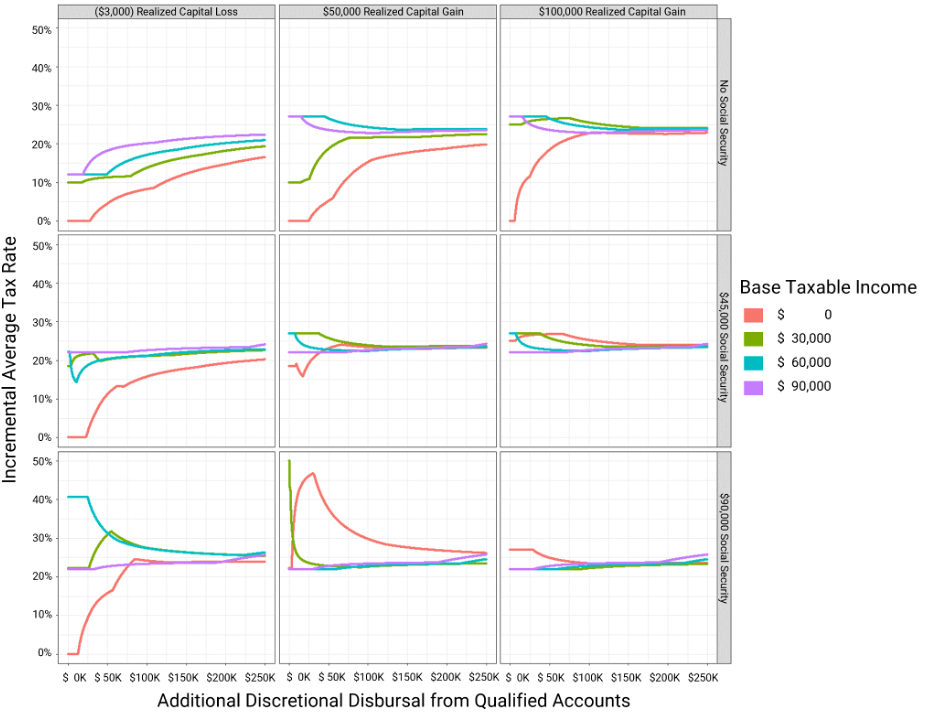

Figure 2: Determining Incremental Average Tax Rate on Discretionary Qualified Disbursals

As shown in figure 2, a household’s initial tax base (Social Security, non-Social Security taxable income, and realized capital gains) has a dramatic effect on the incremental average tax rate for discretionary disbursals from TDAs. These households would also need to be aware of what the breakpoints are for crossing the threshold for increased Part B premiums and take that into consideration. Planning software can determine whether it makes sense for a particular household to temporarily pay higher premiums to make larger Roth conversions at a higher targeted tax rate.

Income Discovery’s AI engine AIDA evaluates multiple configurations of both TQDs and capital gains management in conjunction with other strategy levers to find the optimal retirement income plan for a particular household. A TQD strategy consists of a targeted incremental average tax rate and whether to use the discretionary disbursals for sourcing the annual income, Roth conversions, or both. A capital gains management strategy consists of how to distribute taxable disbursals across non-qualified accounts to minimize gains when sourcing income and the full tax picture is unknown, whether to perform tax loss harvesting throughout the year, and/or realizing gains tax free (at the 0% rate) at the end of the year when the full tax picture is known.

By combining the optimal tax-smart strategies as part of a holistic retirement income plan including Social Security claiming strategy, annuitization, pension settlement, and investment strategy, AIDA aims to get households up to a 30% increase in post-tax income on their desired retirement timeline compared to a typical strategy. Once the optimal strategy is chosen, AIDA switches to management mode in paycheck and each year determines the appropriate account-specific disbursals based on the selected TQD target and CGM strategy.

The financial planning profession has often relied on simple calculators and rules of thumb regarding tax-bracket management that misses the impact of discretionary disbursals from TDAs. Reichenstein and Pfau’s frameworks are useful steps in advancing our thinking about the nonlinearity of taxes. Many other industry experts have discussed the issue of the Social Security multiplier, Medicare premiums, and capital gains taxes and their impact on taxes. But the profession still needs accepted best practices. Advanced software like Income Discovery considers these factors while optimizing and managing retirement income plans and helps advisors and their clients make informed decisions by highlighting the impacts and benefits of tax-smart strategies.

Stephan Granitz is a vice president and the chief analytics officer at Income Discovery

1Calculated as IRMAA Addition Number of Beneficiaries divided by Total Part B Premium Number of Beneficiaries as presented in MDCR PREMIUMS 4. Medicare Premiums: Medicare Part B Premium Beneficiaries and Amounts, Calendar Years 2014-2019 https://tinyurl.com/s24bj9r7

2Safe retirement income is the amount of income that has a 90% opportunity of being available into a retiree’s mid-90s. Safe retirement income consists of all sources of income (not just guaranteed sources): Social Security benefits, pension payments, lifetime income payments, withdrawals from investments and any other incoming cash flows, such as part-time work and rental income. Safe retirement income is increased by Social Security retirement benefit claim deferral, purchase of annuities, changing investment portfolio asset allocation and other strategies. The amount of increase and the optimal strategy varies depending on the individual circumstances, annuity payout rates and capital market return expectations. Read our white paper for limitations of the analysis, details of a hypothetical client case and assumptions.

Read more articles by Stephan Granitz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.