Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

A practice built on a stool of products, pricing and performance is doomed to collapse. Competent planning requires a focus on the deeper issues your clients face.

The financial industry is a landscape littered with landmines that consumers and their advisors must navigate, with preconceptions of what they think should be important rather than what is important.

We are all guilty of it; chasing the new shiny object, reacting to the latest headline, chasing rates of return, or putting money in front of what really counts.

Every investment professional promotes the investments they offer as better than what the consumer has, so that customers will move their money to them. Vendors provide software specifically designed to accentuate a feature or statistical aspect of an investment portfolio in an attempt to separate the consumer from their investments and/or their advisor.

Every financial professional offers investment consulting. It is often their primary offering, and they all say they are good at it! No joke, right? If they couldn’t invest, they would be out of the profession. Of course, an advisor wouldn’t say to a potential client, “Hey I’m not that good at investing but please invest with me anyway, and hopefully I’ll get close to what your current stuff is already doing for you.” It seems silly, but all advisors have access to similar technology and analytics, albeit some may be more limited than others. Investment consulting is table stakes and is nothing more than a commodity you can obtain with a few clicks of a mouse at extremely low cost. Fidelity will invest your money for free!

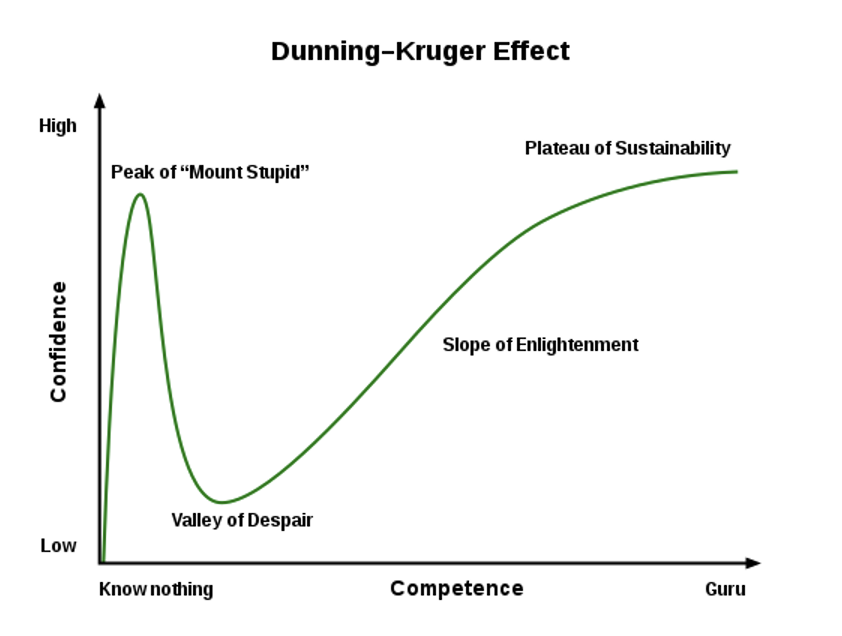

Nobody has a perfect solution; if you think you do, you are at the peak of “Mount Stupid.” Please forgive the terminology, but psychologists David Dunning and Justin Kruger came up with it, not me. The point is that no single investment strategy, money manager, fancy annuity, life insurance contract, daily volatility hedging strategy, or whatever hot financial thing is being circulated will consistently outperform everything else. If anyone had the best performing strategy, we would all already be invested there.

Before you send me hate mail about how great your investment performance is or how you have the best trading strategy, hear me out. Even if your historical performance is great, past performance is not indicative of future results. And, if you are the best performer, better than all the rest, you are not reading this article because you are having drinks with Warren Buffett. If you are an advisor and leading with investment performance as your differentiator, it will only be a matter of time before another advisor does the same to you. Having the best performance is not sustainable.

Nobody has the magical investment strategy or product that solves all the problems or consistently outperforms everything else. To get great results for a client, you must do advanced planning, which fewer than 7% of financial professionals do.1 A lot of advisors talk about it, but few have the resources to deliver. More on that in a bit.

The faulty thinking that investment performance is the key to success comes from our misguided investment decision-making process that focuses on the wrong thing and is often a byproduct of what is known as the Dunning-Kruger effect. In psychology, it is a cognitive bias whereby people with limited knowledge or competence in a given intellectual or social domain greatly overestimate their competence relative to objective criteria or to the performance of their peers or of people in general.

In short, we don’t know what we don’t know, but we think we know more than we do.

I’ll use myself as an example. In the beginning of my career, I was told that a fixed-indexed annuity was the greatest invention since cell phones and everyone, yes everyone, was supposed to have at least a portion of their money in an FIA. When I was working in my father’s firm before opening my own, he would say, “Everyone in this room should have a portion of their portfolio in an indexed annuity. Everyone.” I believed him with strong conviction and was very good at sharing this with consumers.

But I was at the peak of “Mount Stupid.”

I knew all about index annuities and how to sell them, and I was very good at it. A few years later I started utilizing managed money accounts with clients and began to slide down off the peak, and when I became a CERTIFIED FINANCIAL PLANNER™ professional I found myself in the valley of despair. Now that I had increased my competence, I found that I needed to fill massive gaps in how I was serving clients and in my competence.

I climbed out of the valley of despair through hard work, tenacity, and the desire for enlightenment by creating a virtual family office (VFO). A VFO is a group of highly skilled experts in their own disciplines coordinating their advice for a single client. I share this with you not to brag, but to open your mind to the possibility you may be on the far-left side of the chart above regarding a particular topic. I was at the peak of Mount Stupid, and in some areas, I may still be. That’s why I am constantly seeking out experts to join my VFO, to increase my competence and outsource their expertise to benefit the client. The point is to identify when you are on the far left and move from left to right – or at least admit you don’t have enough knowledge and need help from someone more competent.

This leads us to the three-legged stool of misguided investment decisions. The planning profession has trained advisors to focus on three things, which in turn drives the consumer to look at those same things. But the three most important things the profession wants you to focus on are not nearly as important as the most valuable thing. The asset management industry is shouting about their products, their pricing and their performance. If you focus on those three things, inevitably one of them will fail due to a newer, cheaper or better performing option. You end up with an endless cycle of tipping over, picking yourself back up, only to tip over again when the next leg fails.

Instead, I do not focus on products, pricing, or performance. That’s table stakes. Every financial professional will provide what they believe to be the best product, at the lowest cost, with the best performance. Would you do anything less? There will always be new financial products to distract you.

While they all may have a place, products do not solve problems; advanced planning does.

Cheap is exactly that – cheap. We have all cut corners to save a few bucks and had it blow up in our face. A cheap investment (or advisor) offers you no guarantee that the result will be better. Cheap labor isn’t skilled, and skilled labor isn’t cheap. A client recently told me that working with my company was his largest household expense. As for performance, all investments have periods of looking good or not so good.

When you strip away product, pricing, and performance, you are left with what truly matters – having a cohesive team of experts to solve the five major issues facing wealthy individuals and business owners:

- Making smart decisions with their money;

- Mitigating taxes;

- Taking care of their heirs and their legacy;

- Preventing assets from being unjustly taken; and

- Maximizing gifts to the causes they care about.

Products, pricing, and performance do not address any of these concerns. Addressing the above concerns requires advanced planning with a team of experts. It may require us to humbly move off of “Mount Stupid.”

Jason Glisczynski, CERTIFIED FINANCIAL PLANNER™ professional, leads business owners and upper-level management to a work-optional lifestyle in 7 1/2 years or less, often before they turn age 65. Jason has been regularly recognized in the financial services industry as a top advisor and thought leader. He has appeared on CBS, ABC, WSAU, WAOW, WSAW, Advisor's Magazine, Advisor Perspectives, Investopedia, and has trained advisors across the country on ways to maximize the potential of their clients. Jason is the co-founder and CEO of Silvertree Retirement Planning of Stevens Point, WI with nearly 20 years of experience, a member of the VFO (Virtual Family Office) Inner Circle, and head of the Silvertree Private Wealth Management division, a Virtual Family Office. Investment Advisory Services offered through Brookstone Capital Management (BCM) LLC, a Registered Investment Advisor. Silvertree, LLC and BCM are separate companies.

1CEG Worldwide and AES Nation studies

Read more articles by Jason Glisczynski

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.