Many advisors use historical data to project expected returns for U.S. stocks and bonds. But a close look at the historical data suggests that the excess performance of stocks relative to bonds occurred mainly in two historical periods and has been much less consistent over the last 25 years. Advisors illustrating the decision to increase investment risk to fund future goals should acknowledge the possibility that the historical equity risk premium may be lower – indeed, low enough to no longer be considered a puzzle by financial economists.

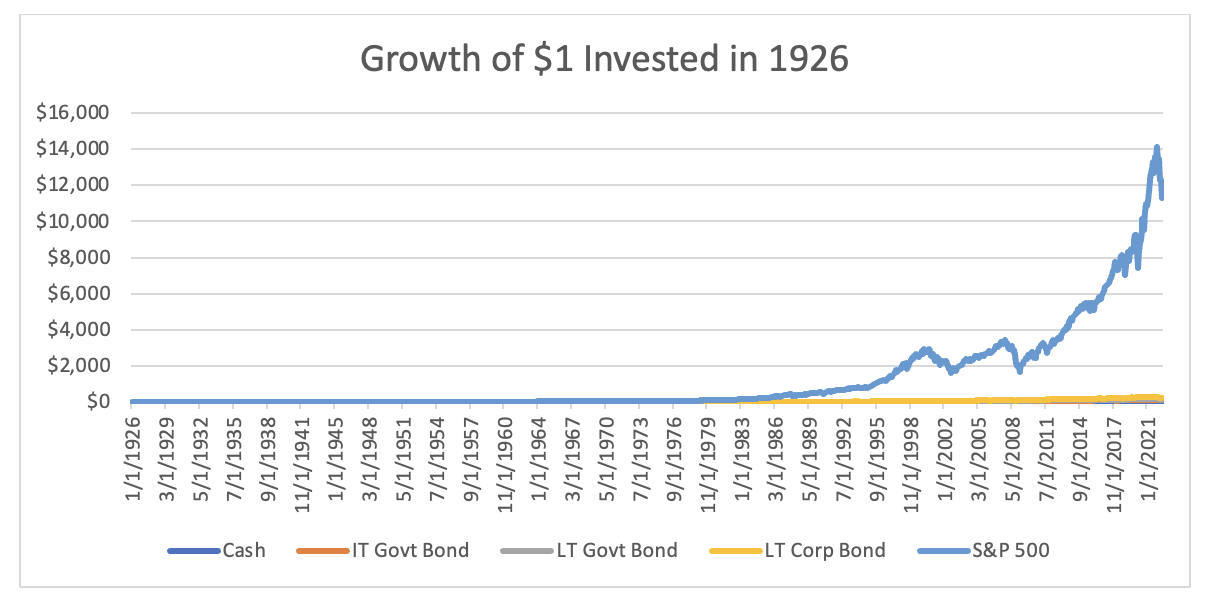

We’ve all seen the graph that compares historical stock and bond performance since 1926 using Ibbotson/Morningstar data:

The graph shows the dramatic performance of stocks compared to bonds over the last 95 years. Advisors show the graph to clients to explain why increasing investment risk pays off over the long run, and how they can provide value by creating portfolios that harness the power of equities.

The outperformance of stocks over bonds is a mystery to financial economists who refer to it as the “equity premium puzzle.” Between January 1926 and June 2022, the arithmetic average return on the S&P 500 was 11.43%, while the average return on intermediate-term Treasury bonds was 4.91% and T-bills returns were just 3.2%. Richard Thaler, who recently won a Nobel Prize in economic sciences, co-authored a widely-cited paper in 1995 that explained low stock ownership among individual investors as a behavioral anomaly driven by the tendency to focus on short-term losses rather than long-term excess performance. In other words, by helping investors manage short-term volatility and focus on long-term growth, advisors could help their clients capture puzzlingly high investment returns.

The idea that stocks are an engine that powers successful achievement of long-term goals has become dogma among financial professionals and even among academics. According to this dogma, investors with long-term spending goals should increase equity allocation to maximize expected long-run returns. I even co-authored a paper that uses a goals-based approach to estimate how much optimal equity allocation should rise when an investor’s time horizon increases.

However, much of the historical data covers time periods where, for stocks, the information was scarcer and transaction costs were much greater than the modern era. Today half of all American households invest in the stock market in mutual funds and ETFs that allow us to create well diversified stock portfolios at a very low cost. More than half of workers invest in stocks every month in 401(k)s through target-date funds. Capital gains tax rates are also historically low. The low costs and widespread automatic investment in stocks mean that markets do not need to provide a high equity premium to encourage investors to accept the risk of stock investments.

Whether the equity risk premium will persist is fundamental to planning strategy. Quantitative planning tools that estimate optimal asset allocation and saving will recommend riskier portfolios and lower optimal saving when fed stock return data from periods where stocks dominated bonds. Retirement planning software will provide analyses that assure clients that taking greater investment risk will reduce the probability of running out of money.

But a closer look at the data shows the inconsistency of the equity risk premium and suggests that the premium became far more modest as the costs of stock ownership fell.

A goals-based approach to investment risk

Imagine a newly retired 65-year-old investor. She hopes to use stocks and bonds to pay for expenses that will occur each year. If she invests a dollar in stocks, she presumably will be able to spend far more than if she invests in bonds. This belief is strengthened by the obvious outperformance shown in the previous chart.

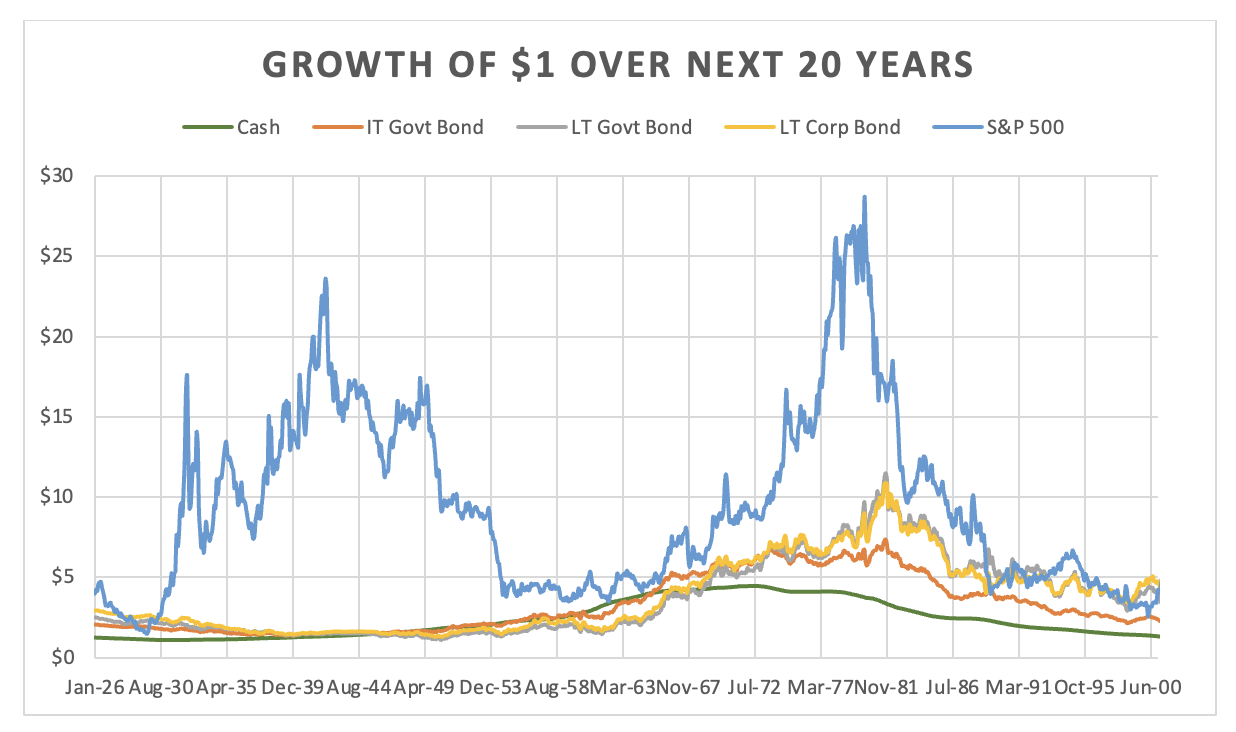

How confident can she be that each dollar invested in stocks will result in significantly more future spending than an investment in bonds? Let’s look at the historical record of goals-based stock investment returns. The next chart, created with the assistance of David Blanchett, head of retirement research at PGIM, shows the nominal growth in $1 over historical 20-year periods using the same Ibbotson/Morningstar SBBI data as the previous example.

The chart shows how much $1 would have grown if invested in stocks, intermediate-term government bonds, long-term government bonds, long-term corporate bonds, and the S&P 500 over the next 20 years. In other words, the point above January 1926 represents the growth of $1 between January 1, 1926 and December 31, 1945.

The chart illustrates just how inconsistent investment growth has been over 20-year time horizons. The problem with drawing conclusions about the excess performance of stocks over the last century is that much of the high returns relative to bonds occurred during the mid-20th century in the United States, and during the 20-year period prior to the run-up before the tech bubble.

No retiree has a 100-year investment horizon. For a retiree, the distance between the initial investment and the sale of the investment to fund spending ranges between one and perhaps 35 years depending on the age of retirement and health.

A sharp-eyed reader may question how a stock investor in, say, February 2000 would have seen their savings grow from $1 to only $3.41 by the month before the pandemic crash after the longest bull market in the history of the S&P. A $1 investment in long-term corporate bonds rose to $4.77 over this same period, and even intermediate-term Treasuries rose to $2.52. If the investor had waited another month, the intermediate-term Treasury would have beaten growth in the S&P over 20 years.

Beginning January 1, 1990, a $1 investment in the S&P at the beginning of the month never grew to a value higher than $7 over the next 20 years through June 2022. No S&P investor between October 1, 1933 and March 1, 1954 saw their initial $1 investment grow to an amount less than $7 over 20 years, and in most cases, investors saw their $1 grow to between $10 and $20 with an average future amount of $13.

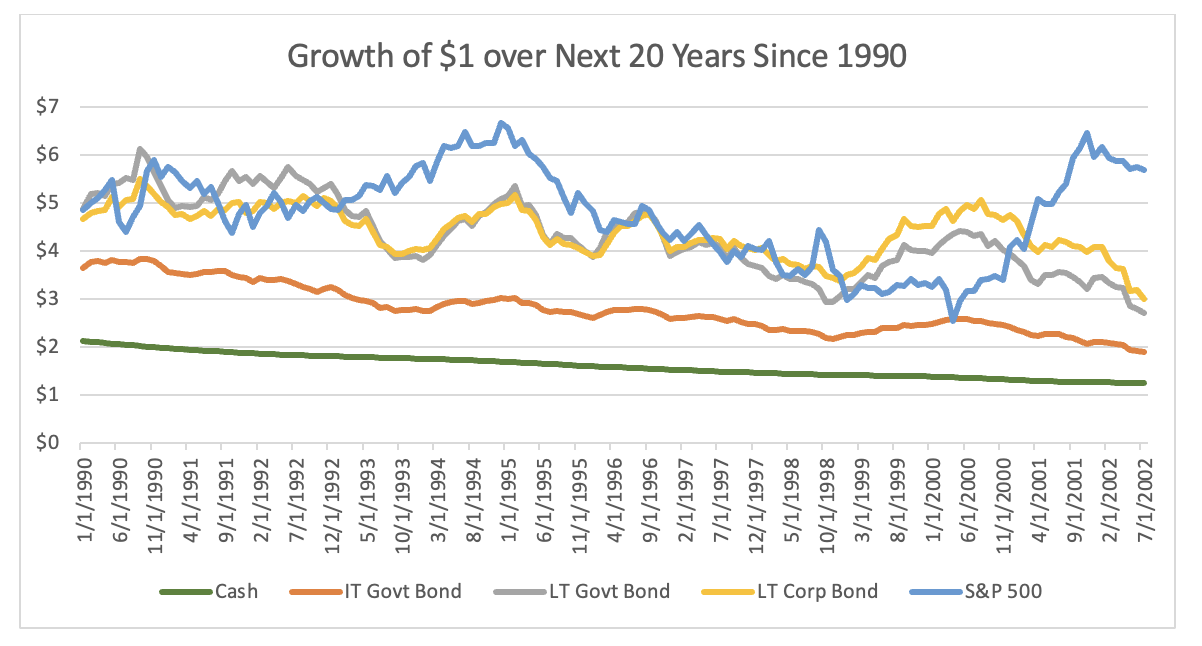

The next figure shows the relative growth of stocks compared to bonds during the modern mutual-fund era beginning January 1990. Defenders of the high equity premium dogma may argue that longer-term bonds have benefited from a declining interest rate environment. The fact remains, however, that the 20-year growth is far less than growth in stock investments through much of the 20th century. Stock valuations are also based on discounted long-term cash flows and will likely also be reduced by an increase in interest rates. For example, S&P investors in the mid-1960s who faced a long-term rising interest rate environment saw growth over the next 20 years that was only slightly higher than the growth of an investment in T-bills.

Despite the more modest 20-year growth in the modern era, the consistency of the long-term excess performance of stocks relative cash (T-Bills) is notable. Over long horizons, stocks have recently always beat cash even though they occasionally underperformed long-term bonds. Despite arguments against recommending a higher stock allocation for longer horizons by economists, return data both in the United States and internationally suggest that optimal stock allocation, even for risk-averse investors, is surprisingly high for long-term investing horizons.

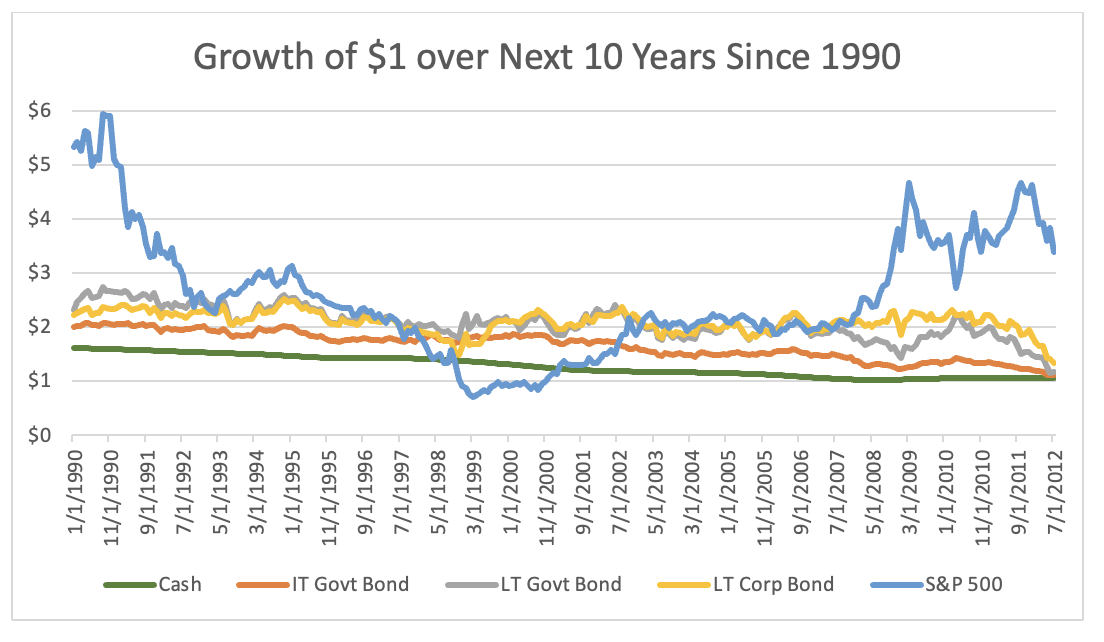

As time horizons shrink, excess stock performance over bonds becomes less consistent. The following graph shows the growth of $1 over 10 years during the modern era. Sometimes stocks outperform, and sometimes they underperform even T-Bills. As I noted in a previous article for Advisor Perspectives, an investor is at far greater risk of underperformance if she buys stocks during periods where prices relative to recent earnings are high.

The volatility of future stock prices is a reminder that investment risk is real. An investor who has a shorter-term financial goal, for example saving for a child’s education, needs to accept a greater range of future investment outcomes when she takes greater investment risk. Even though investors are historically rewarded for accepting risk, this reward may not materialize over short-term horizons.

Planning implications

As a long-term investment, stocks trounced bonds for much of middle-20th century in the United States. This trouncing shows up in the historical data often used to project future asset growth. In this analysis, I show that the highest excess performance of stocks occurred in two historical periods and have not reappeared in the modern era.

Advisors who rely on historical data that include these periods from the golden years of domestic stock investing are likely to overestimate investment growth and the relative benefit of a higher portfolio allocation to stocks when investing for future client goals. While the benefit of investing in equities persists in the modern era, there is always a possibility that stocks will not outperform bonds – particularly over shorter-term time horizons.

Michael Finke, PhD, CFP®, is a professor of wealth management, WMCP® program director, and the Frank M. Engle Distinguished Chair in Economic Security Research at The American College of Financial Services.