Rising interest rates was the dominant story in 2022. Did fixed income losses cripple insurance companies? Or has the insurance industry shifted the risk to your clients who purchased their products?

Rising interest rates was the dominant story in 2022. Did fixed income losses cripple insurance companies? Or has the insurance industry shifted the risk to your clients who purchased their products?

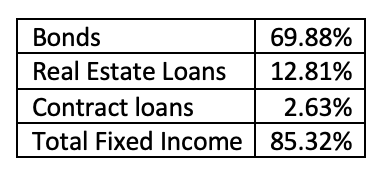

This has been the worst year in the history of the bond market. Through the first three quarters, a Bloomberg Aggregate Bond fund (BND) lost 14.50%. That will have a huge impact on life and annuity insurance companies which had, on average, 85% of their assets in fixed income, according to the Insurance Information Institute. The loss on the 85% fixed income was roughly the total capital surplus of the industry.

Let’s look at the insurance industry and, more importantly, the impact on our clients who own insurance products.

Background

In October, my article in Advisor Perspectives summarized the bond performance from Edward F. McQuarrie, professor emeritus in the Leavey School of Business at Santa Clara University who has long researched the history of bonds:

Life and annuity insurers overall had the following investment allocations to fixed income on their balance sheets at the end of 2021:

While I don’t know the duration of these fixed income holdings, clearly the economic value of those assets plunged this year, though not necessarily their book value. I spoke with Dale Hall, managing director of research for the Society of Actuaries Research Institute, who confirmed that insurance companies do not mark to market. He stated “bonds bought at premium are recorded at cost and accreted. Bonds bought at discount are recorded at cost and amortized.”

But market value is far more important than any statutory accounting rule or the book value by which it is calculated.

Yet the decline in the economic value of the assets is only half of the story. The reserves are derived from the value of the assets less the liabilities. Cynthia MacDonald, senior director of experience studies at the Society of Actuaries, stated, “Same goes for liabilities. A SPIA liability doesn’t decrease with increasing rates.” The liability of an annuity, such as a SPIA, is the present value of the anticipated payments to the annuitant, discounted at now higher interest rates.

A recently purchased SPIA would likely have a duration greater than the fixed income assets used to back it. That’s a net plus for the annuity provider as the market value of the SPIA could decline by as much as the 37.4% of the Extended Duration Bond Fund (EDV) noted above. Of course, the inflation-adjusted payouts from the SPIA to the consumer who purchased it would be drastically reduced.

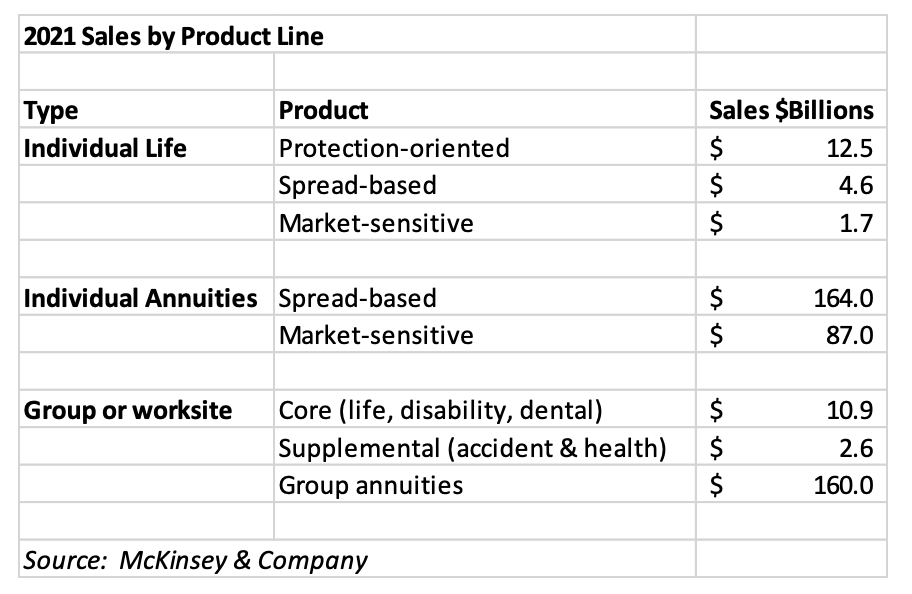

I turned to the global management consultant, McKinsey & Company. Its Global Insurance Report 2023: Reimagining Life Insurance reported on segments of the insurance industry and provided a framework to evaluate the impact to liabilities. The chart below came from this report:

Let’s look at how this mix of products, and examine the impact of the liabilities from these higher rates.

Individual life is comprised of whole life (protection-oriented), indexed variable life (spread-based), and variable life (market-sensitive). Life expectancy hasn’t changed much, so that could have a negative impact on the insurance company, though I typically see variable life products giving the insurance company the unilateral right to dramatically increase the cost of insurance, thereby protecting the company.

Individual annuities are products like fixed indexed and registered indexed-linked annuities (spread-based) which typically give the insurance company the right to unilaterally reduce maximum returns from those indexes in addition to carving out dividends from the return to the policy holder. Other products like variable annuities (market-sensitive) pass most of the risk of market returns to the policy holder.

Group or worksite products are mostly comprised of group annuities such as a stable value fund. That may be a big plus for the insurance industry, which had legacy contracts to employers offering above market returns on stable value funds when rates were so low. These legacy rates are no longer attractive.

I spoke to Ramnath Balasubramanian, a senior partner at McKinsey in New York and one of the authors of this report. He told me, “In general, life insurers are quite deliberate in matching liability and asset durations. In the near term, the rise in rates is providing a tailwind across the life industry, as assets reprice quicker than the liabilities.” He also stated, “Over the past decade, given the low interest rate environment, insurers have reduced the level of guarantees in their product portfolio and shifted away to non-guaranteed products.”

While the assets insurance companies that support liabilities lost market value, it’s likely their liabilities have decreased by at least the same amount or more. The net effect on their balance sheets is positive.

The future of the life and annuity business

I was stunned to read in the McKinsey report that the largest U.S. life insurers’ share of market capitalization within the financial services sector has decreased over the past 35 years – from 40% in 1985 to 17% in 2005 to only 9% in 2020. Balasubramanian told me the industry once had about the same market capitalization as the banking industry, but because it has frequently had returns less than its cost of equity, its relative market value declined.

Distribution channels are changing. McKinsey noted proprietary sales forces are declining, as third-party distributors are increasingly becoming more dominant, expanding their share of the market from 49% in 2010 to a forecasted 55% in 2021. Thus, RIAs and the platforms that serve them are becoming more important to the life and annuity business.

My conclusions

My thesis that the insurance industry would be under extreme stress with surging rates was dead wrong. Not only did my research disprove my hypothesis, but the market disagrees with me as well. As of November 25, 2022, the insurance company sector has a positive 9.4% return YTD while the U.S. market as a whole was down 15.6%.

Still, someone had to absorb those huge losses in bonds. The logical conclusion is that it had to be the individuals buying the insurance policies and annuity products. Much like the insurance companies do not mark to market, neither do policy holders. They do not see or know the market value of what they purchased.

MacDonald told me, “I remember back in the ‘80s when rates were high and insurance companies navigated well.” Hall followed up by saying, “With new higher rates, there may be some new products such as annuities with LTC benefits.” Expect those new products from the insurance industry.

This bond bubble illustrates that the insurance industry has developed products that shift risk to the policy holders. Indeed, I’ve worked with several insurance actuaries in my career, and they are smart people.

The insurance industry is increasingly dependent upon RIAs to distribute products. Thoroughly read every product and contract before recommending to a client. Look for any wording that shifts risk, such as giving the company the right to lower the return or increase the cost of a death benefit at its discretion.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

Rising interest rates was the dominant story in 2022. Did fixed income losses cripple insurance companies? Or has the insurance industry shifted the risk to your clients who purchased their products?

Rising interest rates was the dominant story in 2022. Did fixed income losses cripple insurance companies? Or has the insurance industry shifted the risk to your clients who purchased their products?