Long-Horizon Investing, Part 2: Stocks are Always Risky

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This is part two of a five-part series that develops an analytical framework for long-term, retirement-oriented investing. You can read part 1 here. The author would like to thank Joe Tomlinson and Michael Finke for their helpful comments on this article series.

Introduction

As I noted in Part 1 of this series, common aphorisms and assumed truths about stock returns often imply the disappearance of risk over long horizons. (E.g., “you’ll have time for stocks to recover” or “you’re betting on the economy, and that always wins in the long run.”)

But among those who have researched the concept in depth, the existence of long-run stock risk is not particularly controversial. For example, Jeremy Siegel of Stocks for the Long Run fame had this to say, in the chapter of that book in which he most aggressively made the case that stock risk is unexpectedly low and that stocks are better than bonds over long timeframes:

Note that I am not claiming that the risk on a portfolio of stocks falls as we extend the time period. The standard deviation of total stock returns rises with time, but it does so at a diminishing rate.1

In perhaps the most famous treatise favoring long-run stock investing, the author did not claim stock risk disappears at long horizons, nor even that it diminishes, but only that it grows at an unexpectedly slow rate! No wonder then that in the famous debate between Siegel and Zvi Bodie, the actual disagreement is a bit hard to spot.

The market thinks the market is risky

Speaking of Bodie, his article “On the Risk of Stocks in the Long Run” used options to make the case that stock risk grows with the time horizon. Strictly speaking, what he demonstrated is that the up-front cost to purchase protection against stocks underperforming the risk-free rate increases as the time horizon increases.

To make this case, Bodie used put-call parity to show that the price of a put to insure against a shortfall below the risk-free rate must be equal to the price of a call capturing all stock returns above the risk-free rate.2 This is true regardless of the amount of time to expiry. In fact, the call option gets more expensive with greater time horizon – rather intuitively reflecting the increasing probability that stocks will significantly outperform – and the put option grows equally more expensive – less intuitively reflecting the growing magnitude of a potential shortfall in the worst-case scenario.

Put-call parity itself is just an example of the law of one price (LOOP), which states that two assets or portfolios with identical payoffs in the future must have the same price today. This is far removed from assuming a random walk (Bodie specifically pointed out that mean reversion does not affect his argument) or an “efficient market” in the broader sense of a market that always properly prices future risk and return. Rather, LOOP is among the most basic requirements for a rational, functioning market.

To put numbers to his point, Bodie used the Black-Scholes formula to illustrate rising put prices with increasing horizon. This has led some observers to conclude that his results depend on Black-Scholes, but that is not so. Bodie noted that only the “no arbitrage” principle (i.e., the notion that the market does not leave risk-free, instantaneous profits lying around for anyone to pick up) is required to make the point.3

In fact, I first learned about this line of reasoning in a Harvard Business School course taught by Robert C. Merton, who won a Nobel Prize for developing the Black-Scholes formula.4 He took pains to point out that neither Black-Scholes nor any complicated set of assumptions was required to make Bodie’s point, but only the LOOP.

Taxation likely shifts the LOOP argument a bit further for investors with tax-privileged accounts or in lower tax brackets. Consider the example of municipal bonds, which have higher riskiness than Treasurys but often have lower (pre-tax) expected returns. The tax-privileged nature of munis induces investors in high-tax brackets to bid their prices up to these levels because their after-tax returns will still be relatively favorable. But investors without these tax considerations are thus better served to avoid munis. Similarly, tax treatment for equities is generally more favorable than that for bonds, which may induce tax-averse investors to drive equity prices higher than the levels otherwise suggested by Bodie’s LOOP analysis, which ignored taxation. Unlike munis, this effect is certainly not strong enough to overwhelm the equity risk premium in expectation; but for investors for whom tax considerations are less substantial, this effect would reduce the probability of stock outperformance and reduce the optimal allocation to stocks over any horizon.

Quick hits: Additional theoretical arguments for long-run stock risk

For those interested in digging further into the theoretical rationale for long-run stock risk, here is a whistle-stop tour of additional literature.

In “Risk and Uncertainty: A Fallacy of Large Numbers,”5 Paul Samuelson, one of the godfathers of modern finance, deconstructed the argument arising from the observation that if you take multiple bets in your favor (e.g., multiple years of stock risk) your overall odds of winning grow larger. This is a fallacy because the amount you could lose grows larger as well. When the “bets” consist of consecutive years of investment, a longer series also consumes a higher percentage of a person’s lifetime, further raising the stakes.

In “How Risky are Stocks in the Long Run?”6 here on Advisor Perspectives, Michael Edesess elegantly illustrated the problems with assuming mean reversion will always ride to the rescue over sufficiently long timeframes. (Edesess asserted that Zvi Bodie’s arguments assume Brownian motion, but Bodie’s article clarifies that his primary reasoning holds even if stocks are mean reverting.)

Equal parts theory and quantitative analysis, “Stocks for the Long Run? Evidence from a Broad Sample of Developed Markets”7 by Aizhan Anarkulova, et al., utilized a bootstrap resampling procedure across a broad international stock return data set to estimate that the odds of suffering a real return loss over a 30-year equity investing horizon exceed 12%. Samuelson first suggested a bootstrap procedure in his article “Dogma of the Day,”8 and Anarkulova, et al. improved on the concept with techniques that make the procedure relatively robust to the presence of mean reversion, economic cycles, and various potential data biases.

In “Wishful Thinking About the Risk of Stocks in the Long Run,”9 Zvi Bodie provided a clarifying rehash of his earlier article, addressed fallacies that have appeared in various publications, and pointed out implications for a wide range of investment policies. He also noted that reality mirrors theory, in that at-the-money-forward put option prices do increase with horizon.

Finally, no tour is complete without my favorite Paul Samuelson quote: “When a 35-year-old lost 82 percent of his pension portfolio between 1929 and 1932, do you think that it was fore-ordained in heaven that it would come back and fructify to +400 percent by his retirement at 65?”10

An important general point here: If we choose to believe that stocks become riskless over some time horizon (say, 30 years), then if they underperform over a shorter time horizon (say, 15 years), we now have a shorter time horizon (the next 15 years) over which they must necessarily outperform by even more, to make up for the earlier shortfall. This is the stock investing version of the “gambler’s fallacy.” It also illustrates the difference between rational mean reversion – where lower valuations may indeed imply higher expected returns for stocks, quite possibly as compensation for elevated risk! – and irrational mean reversion – wherein prior losses must necessarily be fully compensated by sufficiently higher subsequent returns to ensure the attainment of some long-run average.

Admittedly, the above arguments all depend on an assumption of basic market rationality – though again not on anything like full-blown market efficiency. But for anyone who sees in this fact a potential escape clause whereby behavioral anomalies might explain disappearing stock risk in the long run, I would offer the following caution: Not only must you thereby believe that the markets are so massively inefficient as to effectively create two risk-free rates (the long-run Treasury rate and whatever higher rate the stock market is sure to achieve11), but you must also believe that this irrationality is unidirectional, such that the market in its inefficiency only ever sets the prices of stocks too low.12

Quantitative analysis

Okay, so maybe the theory says stocks can’t be riskless in the long run, but doesn’t the evidence say they are anyway? Certainly the “stocks for the long run” case is always made using historical data. After all, as one example, since the 1926 inception of S&P 500 total return data, the worst 20-year nominal and inflation-adjusted returns for the index were +3.1% and +0.8% annualized, respectively. The worst nominal and real 30-year returns were +8.5% and +4.4% annualized, respectively. These results seem far removed from the warnings of Bodie and his ilk.

A major issue here is the paucity of independent long-run data. For example, the S&P 500 total-return history contains only three independent 30-year periods…far too few to be of statistical significance. Even the dataset used by Siegel commencing in 1802 is sufficient to produce only seven independent 30-year observations.13

This problem may be even worse than it appears. As I noted repeatedly above, in any model for stock returns, the probability of a shortfall declines as the horizon increases, but the magnitude of the worst shortfalls grows larger. Thus, as the horizon increases, stock risk increasingly looks like “tail risk.”14 This implies that as the timeframe grows, the amount of independent data required increases – i.e., to establish whether negative outlier events occur less frequently than they should – but the amount of independent data available decreases.

The inclusion of international data can expand the available set. But this introduces some sobering examples, such as Japan, a global powerhouse economy whose stock market spent more than 30 years below its 1989 peak, or Austria, whose stock market has produced just a 0.9% annualized real return since 1900! And even then, it’s debatable just how much independent value is added by including additional countries, given the (inter-)dependence of countries’ stock markets on the remarkable global economic developments of the past century.

Monte Carlo-style statistical tests

Given how few “long runs” are available, we are typically reduced to using overlapping historical data, such as 20- or 30-year return series commencing each year. Statistical techniques exist to perform hypothesis tests on overlapping data, but it pains me to realize that my relevant mathematical training occurred what is now more than half my life ago. But the intervening decades also produced a mind-boggling explosion in computing power, enabling another type of statistical testing: Monte Carlo analysis.

In what follows, I start with the 97-year historical S&P 500 total return data series and ask the question, “How unlikely would these results be if stocks followed an IID random walk?”

This is not to suggest that I believe stocks truly follow Brownian motion; the evidence for momentum, mean reversion, and “fat-tailed” distributions is formidable.15 But if the historical evidence that gives rise to the belief in long-run stock safety cannot be reliably distinguished from the results of a random walk that does not provide such safety, then our hope that what doesn’t work in theory might yet work in practice must surely be diminished.

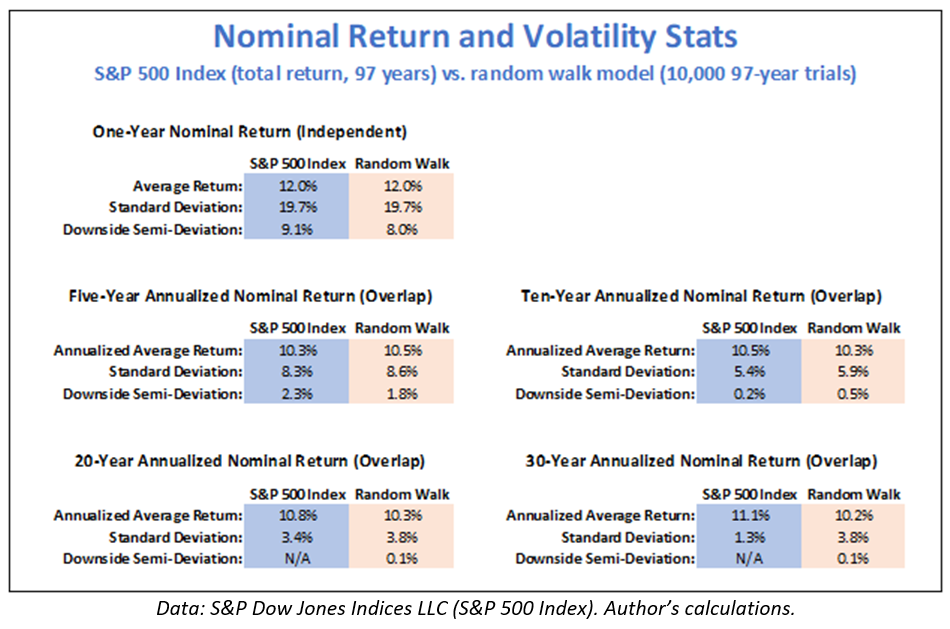

To that end, below is a comparison of S&P 500 historical data versus a random-walk simulation of 10,000 97-year trials drawn from a normal distribution with mean equal to S&P’s arithmetic average annual return and standard deviation equal to S&P’s historical volatility.

One-year results confirm that the average return and standard deviation across all 970,000 independent yearly trials matches S&P, as expected. I also include a measure of downside risk, “downside semi-deviation” (sometimes simply called “downside deviation”), with a target return of 0%.

Subsequent tables compare the historical record to the average of 10,000 97-year random walks for overlapping five-, 10-, 20-, and 30-year periods.

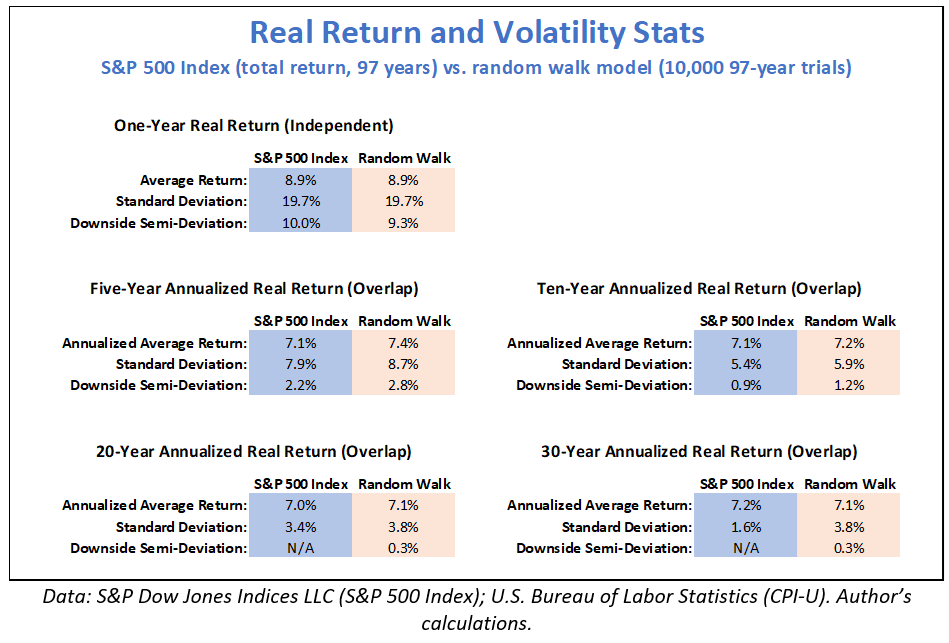

The tables below show the same concept, but with inflation-adjusted “real” returns. Because it restates all calculations in purchasing-power equivalents, this version of the analysis is arguably superior.

There are two items to note. The annualized multi-year returns (i.e., compound annual growth rates/CAGRs) are lower than the single-year arithmetic average returns; this is the expected result of variance drain.

Second, as the timeframe increases, the average annualized standard deviation declines in both the live and trial data. How are we to reconcile this with Siegel’s statement above that risk increases with horizon? Simply put, as Siegel explains on the prior page of his book, the annualized volatility of returns in a random walk declines by the square root of time. But the volatility of total terminal wealth increases by the square root of time.16 Both Siegel and Bodie would submit that the variance of total wealth is a better measure of risk, and I would agree. But in an apples-to-apples comparison like this, annualized figures can be easier to work with.

What do we observe from the figures above? Just as Siegel stated, the annualized volatility of returns in the live S&P data declines faster than the average volatility in the simulation. The riskiness of stocks has indeed been less than would be expected!

The downside risk looks even better. In fact, in the 20- and 30-year overlapping data, there has never been a negative nominal or real return.

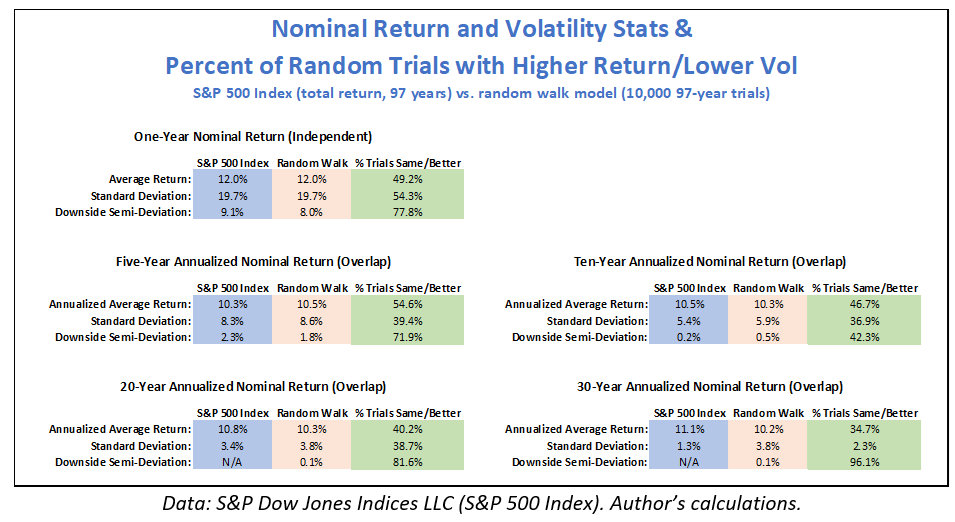

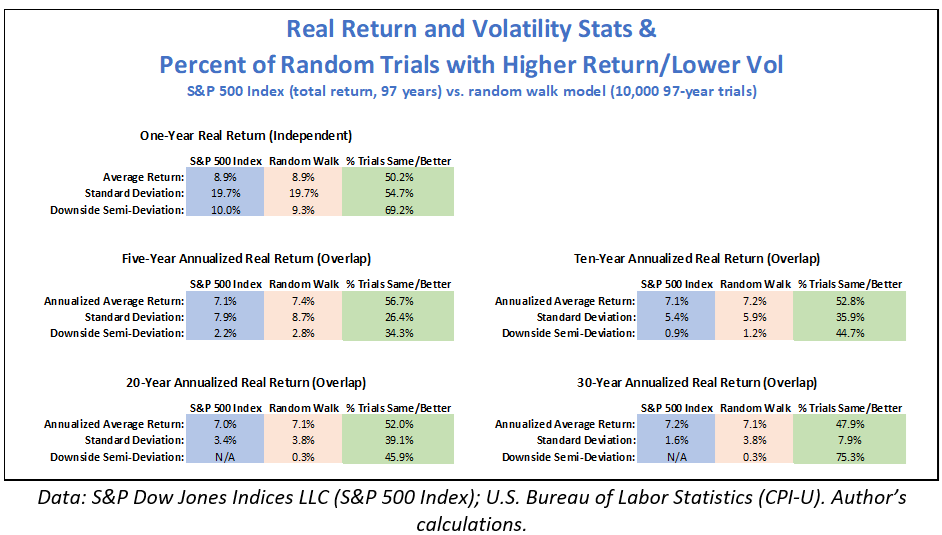

But exactly how improbable are the live outcomes? To help answer this question, we can count how many of the 10,000 simulations produce results that are “as good as” or “better than” (i.e., same/higher return or same/lower risk) the live data. The results for the nominal and real data are shown in the tables below.

On most metrics, the S&P results would not even be a one-sigma outlier. For example, the lack of negative real returns on 20- or 30-year horizons seems rather less impressive when observing that nearly half and three-quarters, respectively, of all random trials produce the same result.

In fact, it seems none of the less-than-expected risk figures would pass a 1% test to reject the hypothesis that they were derived from a random walk. Only one data point would pass a less stringent 5% test, though to Siegel’s credit, that data point is the standard deviation of overlapping 30-year nominal returns. But when we back out the noise introduced by time-varying inflation in the live data – i.e., by switching to real data – even the average 30-year standard deviation is bettered by nearly 8% of the random trials.

Again, none of this analysis purports to prove that S&P 500 returns are really drawn from an IID random walk. But the inability to reject that hypothesis, combined with the powerful theoretical arguments for non-negligible long-run stock risk, argues for great caution about adopting a “stocks will surely outperform over time” investment approach regardless of risk capacity.

What if the expected return isn’t really that high?

There is more to consider. The above calculations derive from a random walk using the historical average S&P return as the mean in the generating function. But given the wide dispersion of plausible long-run outcomes, it is highly unlikely that the ex-post realized return will be equal to the ex-ante expected return. What if the market did not, in fact, fully price in the explosion in corporate profitability over the past century?

For example, suppose the ex-ante arithmetic-average expected real return was 200 basis points lower, about 6.9%/year. Recentering the random walk around that figure, I still find that 12%, 19%, 19%, and 17% of all 5-, 10-, 20-, and 30-year-overlapping 97-year random trials, respectively, have average annualized returns exceeding those achieved by the S&P 500 over its 97-year history.17

Is it particularly hard to believe that the developments of the “American century” (starting about 1950) represented a 1-in-5.5ish outlier relative to ex ante expectations? Potential evidence for this is the S&P’s aggregate price-to-earnings multiple expansion from 11 to 23 over those years, plausibly indicating upwardly revised profit growth expectations, downwardly revised return expectations, or both. This also implies that even if we get another 97 years at the same economic growth rate and the same relationship between corporate earnings and GDP growth, the S&P P/E multiple would have to expand to 48 to achieve the same total return!

One more thing: Stock risk is shortfall risk

The foregoing analysis considered absolute nominal and real returns, with the downside semi-deviation specifying a “minimum acceptable return” of 0%. But this is too conservative when investments are available that would produce significant positive return risk-free over a preselected horizon. Part 3 of this series will analyze the implications of this point in depth.

For example, we saw in Part 1 that $1 invested in a Treasury STRIPS would be worth about $3.55 in 30 years, guaranteed. Stocks could avoid posting a loss but still fall 255% shy of a return that could be had with certainty.18 (This is central to Bodie’s argument.) Similarly, a 30-year TIPS “constant maturity Treasury” (CMT) rate of 2.08% as of this writing implies that if stocks merely maintain their purchasing power, they will fall ~86% short of the inflation-adjusted return that could be obtained without risk.19

Unfortunately, while I can cobble together a 97-year history for one- and 10-year Treasury rates from freely available sources,20 the history of 20- and 30-year CMT rates21 is only sufficient to yield 36 and 16 overlapping 20- and 30-year periods. Over those limited timeframes, only once in a 20-year period (commencing 2000, near the peak of the dot-com era) did the S&P underperform the risk-free rate, but it did so by 59% (4.3% annualized).

Perhaps paid sources could provide more data, but while I considered a $25,000 Bloomberg license for about 0.68 seconds,22 I decided to pass. Besides, a more rigorous inflation-adjusted historical analysis is hopeless, since TIPS bonds have not existed long enough to supply a single 30-year observation. Suffice to say, though, that while such analysis would likely yield similar results to what were outlined above, they would presumably indicate that even greater caution is in order.23 (Relatedly, the Advisor Perspectives article “Forget What You Know about Stock Returns” by Michael Finke is well worth a read.)

Wrapping up and moving on

If stock risk never disappears, and by some measures even grows with time, why buy equities at all? Because in exchange for the risk of increasingly large shortfalls in worst-case scenarios, the risk premium – the extra expected total return from holding stocks – is both increasingly large (in terms of end-to-end returns) and increasingly probable with a longer holding period. If you have the capacity to take the risk and the tolerance to stomach it, the reward is likely – but not certain – to be well worth it.

This may indeed be viewed as a return for “betting on the economy.” But if economic growth (and associated growth in profitability) were truly predictable, the market in its confidence could set higher prices today for lower, safer returns tomorrow.

Consequently, a better view may be: The riskiness of stocks, over all time horizons, creates the higher expected return. Or as I like to view it: Stocks are always risky, and that’s a good thing! The ever-present risk is why the far higher expected return exists. The return is real!

But the risk is also real. And what if someone can’t accept the risk, or wishes to lock down certain goals without incurring it? What is the low-risk alternative? Part 3 of this series will take up this question, but here’s a sneak peak: If a goal exists at a distant horizon (for example, future retirement income for someone in their 30s), the low-risk option to meet that goal most certainly is NOT cash, T-Bills, or low-duration bonds!

In his role as chief investment officer for Round Table Investment Strategies, Nathan Dutzmann is responsible for applying financial science and investment research to the process of constructing portfolios tailored to our clients’ individual needs and goals. Nathan was previously an investment strategist with Dimensional Fund Advisors and a partner and chief investment officer with Aspen Partners. He holds an MBA from Harvard Business School and a master’s degree in international political economy and a bachelor’s degree in mathematical and computer sciences from the Colorado School of Mines.

1 Jeremy Siegel, Stocks for the Long Run, Fifth Edition, McGraw Hill Education, 2014, p.99.

2 Where the risk-free rate is defined by a horizon-matched zero-coupon Treasury. Readers of Part 1 may sense a theme developing.

3 Put/call parity alone is sufficient to see why the put and call prices must be the same. As to why the price grows larger with the horizon, here are a couple more ways to think about it: 1. Option “time value” always erodes as time passes; or for those familiar with “the greeks”: theta is always negative. 2. A put is portfolio insurance, and like all forms of insurance, you trade a negative expected return for purchased safety; but a negative expected return means the longer in time you retreat from the insured date, the higher the price required up front.

4 Why is it called “Black-Scholes”? Because that’s what Merton named the formula when he developed it as an extension of existing work by Fischer Black and Myron Scholes. On the Harvard and MIT campuses, it is considered more correct and polite to refer to the famous result as the “Black-Scholes-Merton formula.”

On a personal note, one of my first exposures to financial science was a “Research Experience for Undergraduates” project, in which my team developed a software algorithm to find solutions to the differential inequality version of Black-Scholes for American options. This experience greatly augmented my subsequent enthusiasm when I was privileged to meet and learn from Prof. Merton years later.

5 Paul Samuelson, “Risk and Uncertainty: A Fallacy of Large Numbers”, Scientia, 98 [1963]: pp. 108-113.

6 Michael Edesess, “How Risky are Stocks in the Long Run?”, Advisor Perspectives [2014], https://www.advisorperspectives.com/articles/2014/10/07/how-risky-are-stocks-in-the-long-run.

7 Aizhan Anarkulova, et al, “Stocks for the Long Run? Evidence from a Broad Sample of Developed Markets”, Proceedings of Paris December 2020 Finance Meeting

8 Paul Samuelson, “Dogma of the Day: Invest for the long term, the theory goes, and the risk lessens,” Bloomberg Personal Finance Magazine [January/February 1997]

9 Zvi Bodie, “Wishful Thinking About the Risk of Stocks in the Long Run: Consequences for Defined Contribution and Defined Benefit Retirement Plans”, Retirement Management Journal, Vol. 10 No. 1 [2021]: pp. 79-86.

10 Paul Samuelson, “The Long-Term Case for Equities: And How It Can Be Oversold”, Journal of Portfolio Management, 21, no. 1, pp. 15-24 [Fall 1994]

11 This “two risk-free rate” argument is an informal equivalent to Zvi Bodie’s law of one price-based argument. Specifically, if LOOP holds, the only case in which an at-the-money forward put (and thus also a call) could be worth $0 would be if stocks were sure to produce exactly the risk-free rate.

12 Cases cited by behavioral economists to illustrate market inefficiencies (bubbles, meme stocks, securities with similar tickers, etc.) tend to be examples where prices are driven to irrationally high levels, due partly to “limits to arbitrage”: i.e., market frictions that make it relatively difficult for arbitrageurs to bring prices down to rational levels. In other words, market efficiency makes a better floor than a ceiling – the exact opposite of what would be required for stock risk to disappear over some time horizon!

13 Moreover, it is debatable how trustworthy early data is, given the risks of easy data bias and survivorship bias.

14 Another old Advisor Perspectives article, by Geoff Considine, explains this concept quite well: https://www.advisorperspectives.com/articles/2009/07/21/the-retirement-portfolio-showdown-jeremy-siegel-v-zvi-bodie

15 Two of these three anomalies tend to increase riskiness. And they may all be related, as periods of mean reversion can create the “high peak” and periods of trending behavior can create the “fat tails” of a leptokurtic distribution. See this article for details: https://www.transtrend.com/en/insights/riding-kurtosis/

16 Cf. Bodie [2020], p. 5.

17 Moreover, in the recentered data, the volatility of trial outcomes that approximate the S&P’s return is lower. E.g., within the 30-year data, the average annualized standard deviation of those trials whose average return is within 1% of the S&P average is a full percentage point lower (2.7% vs. 3.7%). In other words, conditioning on above-expectation ex post returns, it is more probable to see below-expectation ex post volatility.

18 Unless, of course, even U.S. Treasurys experience permanent default. Which is a thing that can happen. But let’s not kid ourselves: No matter how robustly constructed, your retirement plan probably will not survive that eventuality. I mean, you yourself may not survive whatever precipitates that eventuality.

This is also why this article doesn’t invoke the occasional historical disappearance of some countries’ stock markets (i.e., a -100% return with no hope of recovery). Though it is obviously the biggest stock risk of all, in a U.S. or global market context, it likely represents a risk that cannot be hedged. For example, the above quote by Paul Samuelson continues, “How did the 1913 Tsarist executives fare in their retirement years on the Left Bank of Paris?” Sure, but Tsarist government bond holders fared no better!

19 Granted, real interest rates were meaningfully negative for much of the past decade. Part 3 of this series will consider implications of this contingency.

20 One-year and 10-year CMT data back to 1961 from the St. Louis Fed’s FRED site: https://fred.stlouisfed.org/series/DGS1 and https://fred.stlouisfed.org/series/DGS10, respectively. Approximate prior one- and ten-year data from Prof. Robert Schiller’s data set: http://www.econ.yale.edu/~shiller/data.htm.

21 https://fred.stlouisfed.org/series/DGS20 and https://fred.stlouisfed.org/series/DGS30, respectively.

22 For an android, that is nearly an eternity.

23 Here’s another entertaining example of absolute vs. shortfall risk: The ETF “TJUL” launched in July to some fanfare. Over a two-year timeframe, the ETF promises to deliver an upside of the first ~16% of the S&P 500 (sans dividends), while eliminating losses (i.e., a 0% downside). This sounds amazing until one realizes that the two-year Treasury rate as of TJUL’s July 18th launch date was 4.74%, meaning you could get a 9.8% risk-free two-year return. An upside of 16% and a downside of 0% sounds much less impressive when you reframe it as a 6.2% upside and a 9.8% downside! (And that doesn’t even account for the expected return drag from forgoing the market’s dividend yield.)

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All