It’s getting bleak for equity bulls hoping for a reprieve from the US stock market’s “higher-for-longer” tantrum.

The S&P 500 Index plunged to the lowest level since June on Tuesday, as the Dow Jones Industrial Average wiped out its gain for the year and the Cboe Volatility Index, better known as the VIX, popped above the psychologically important 20 level for the first time in four months.

The turbulence was sparked by a surprising increase in US job openings, something Jerome Powell has been watching as the Federal Reserve tries to tame stubbornly high inflation. His lieutenants have been hammering the theme that interest rates will need to stay high for a long period — Cleveland Fed President Loretta Mester and Atlanta Fed chief Raphael Bostic reiterated it over in the past two days — sending long-term Treasury yields to 16-year highs.

The problem is simply too few buyers. Hedge funds that chased the first-half rally have turned risk-averse, according to Citigroup Inc. Sentiment among retail traders has also soured as they plow cash into money-market funds returning 5%. And Corporate America slowed the pace of buybacks in the third quarter, according to Bank of America.

“It doesn’t seem like stock investors want to get in front of the daily spike in rates,” said Dan Eye, chief investment officer at Fort Pitt Capital Group. “The interest-rate environment needs to calm down before investors can focus on earnings season being a potential catalyst for stocks to move either higher or lower.”

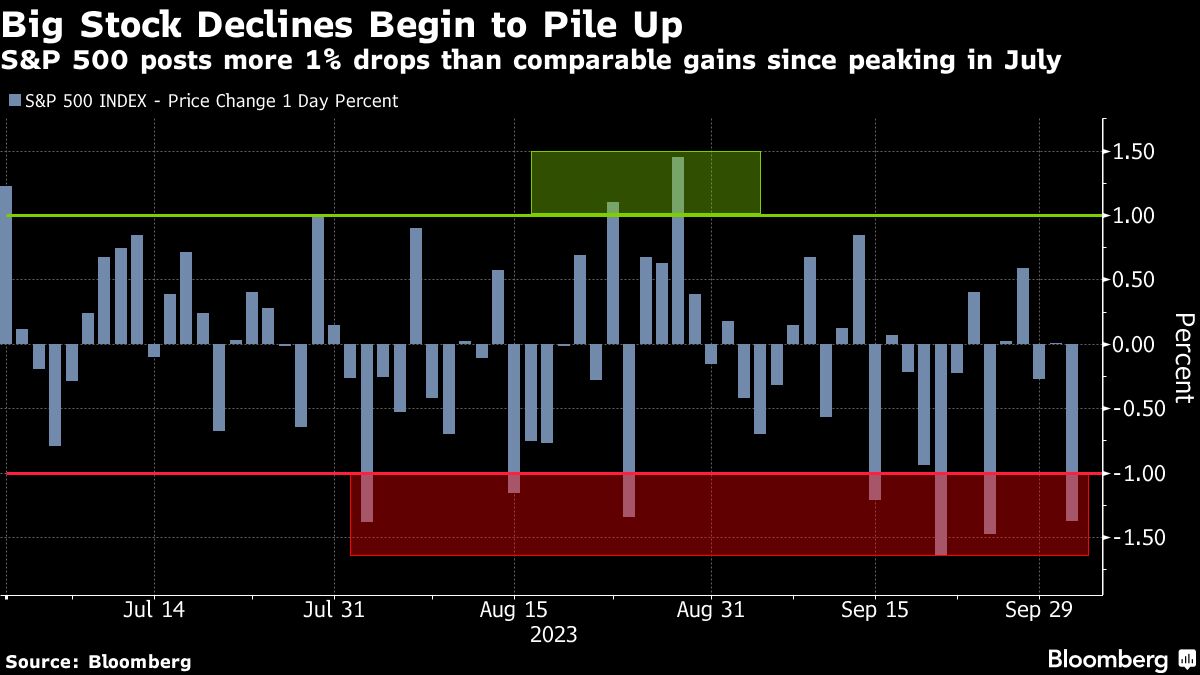

The rout Tuesday was the seventh loss of at least 1% since August, after just three in the second quarter. The stock market’s put-to-call ratio — a gauge of tracking the volume of bearish versus bullish options — has stayed above 1 for seven out of nine days.

Other signs of stress are mounting. The S&P 500 is less than 30 points above its average price over the past 200 days, and breaching that level could set off sharp declines. The index has been over it for 137 sessions, the longest run since the post-pandemic surge that started in June 2020.

Positioning is not likely to help. A measure of how discretionary and systematic investors are positioned tracked by Deutsche Bank AG dropped to underweight last week. The intensity of the move was similar to what happened during the March banking crisis and a June 2022 rout triggered by recession worries.

“Investors are worried that if rates stay higher for longer and we slow down the economy far enough to battle inflation, we’ll slide into a full-blown recession,” said Kim Forrest, founder and chief investment officer at Bokeh Capital Partners. “There is a lot of fear about what could go wrong.”

With stress mounting, the selling has turned indiscriminate. Even the Magnificent Seven megacap tech companies that carried the market for eight months have started to buckle. Since the S&P 500’s near-term peak in July, Apple Inc. is has plunged 12%, while Microsoft Corp. and Amazon.com Inc. are down around 7%.

Anyone seeking safer corners of the market is finding little help. Companies known for their defensive qualities — strong balance sheets or proprietors of products in demand during all economic cycles — are lower. Utilities, which typically do well in these periods, are in a deep slump as investors choose lofty bond yields over their dividends.

Goldman Sachs Group Inc. this week joined Morgan Stanley and JPMorgan Chase & Co. in warning that elevated rates could spark further declines in equities. They pointed to the divergence between the S&P 500 stock index and 10-year real rates approaching the steepest in almost two decades, with the exception of 2020.

Savita Subramanian, Bank of America Corp.’s head of US equity and quantitative strategy, is the outlier, seeing investors’ ultra gloomy mood as reason to buy. A contrarian sentiment indicator from the firm is at a level that’s been followed by positive 12-month forward returns 95% of the time.

“It seems like everything is piling on right at the wrong moment, so to speak, for markets,” Joseph Quinlan, head of CIO market strategy at Merrill and Bank of America Private Bank, said at the Greenwich Economic Forum. “There’s this piling on effect that’s weighing on the market and market sentiment.”

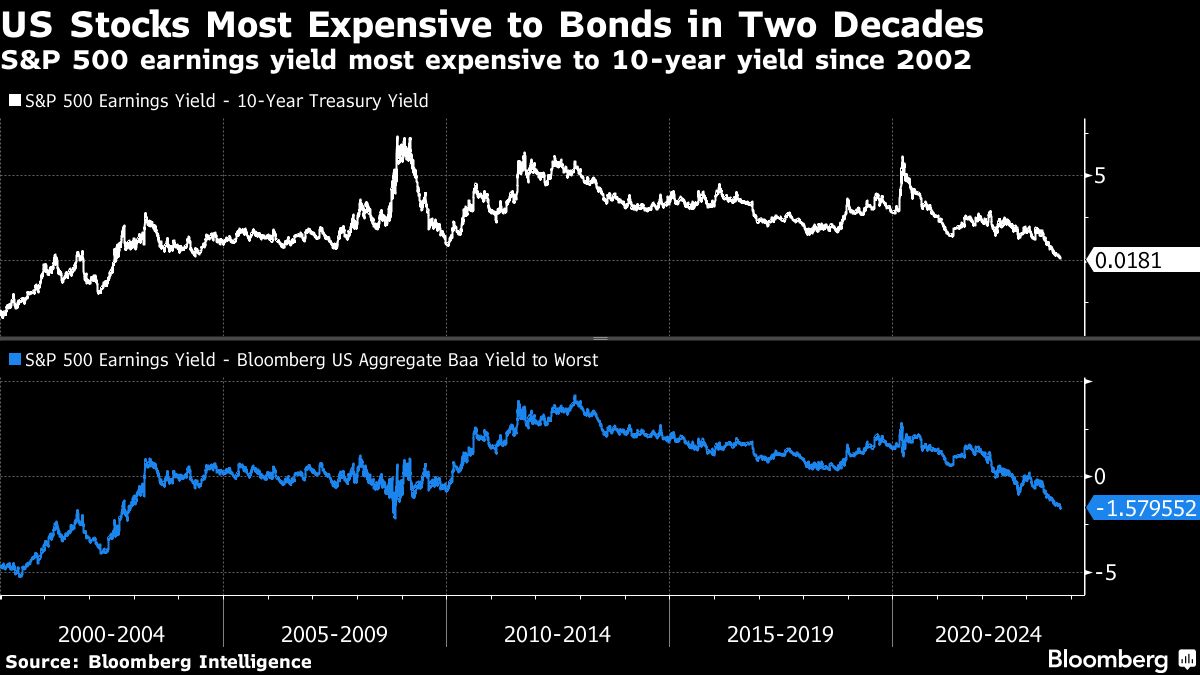

Still, stocks look expensive. A trailing earnings yield of 4.7% on the S&P 500 is virtually on par with the 10-year Treasury yield, putting equities prices at highest they’ve been relative to bonds since 2002, data compiled by Bloomberg Intelligence show. If earnings multiples continue to be held back by high borrowing costs, it may take the broad equities benchmark three years to eclipse its 2022 record, the BI data show.

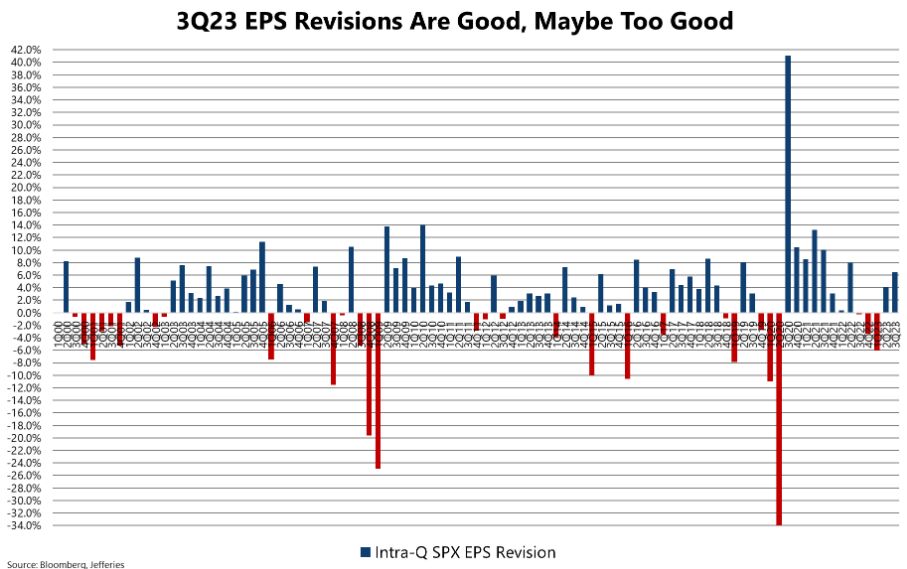

Of course, none of this means dip-buyers won’t emerge. But it’s unlikely that the third-quarter earnings season is going to provide much of a tonic. Yes, estimates for corporate profits have been rising in recent weeks, but investors are growing concerned that companies won’t be able to match the higher expectations with the average revision north of 5% and 10 of the 11 S&P 500 groups seeing improved forecasts.

Data from Jefferies back that up. The firm’s numbers show third-quarter earnings estimates for S&P 500 companies have been revised higher by 6.5% during the three-month period through September. That’s twice the average long-term level of 3.1% for this quarter. Normally, upwardly revised earnings bode well for the market. The S&P 500 tends to rise when revisions exceed the average. But sharp upward adjustments, higher than 5%, portend declines more often than not, the firm said. performance falls when revisions exceed 5%.

“S&P 500 revisions look hot, maybe too hot,” Jefferies strategists including Andrew Greenebaum wrote in a note to clients over the weekend. “That might mean the bar is too high.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Elena Popina, Jessica Menton,Alexandra Semenova