The worst selloff of longer-term Treasuries in more than four decades is putting a spotlight on the market’s biggest missing buyer: the Federal Reserve.

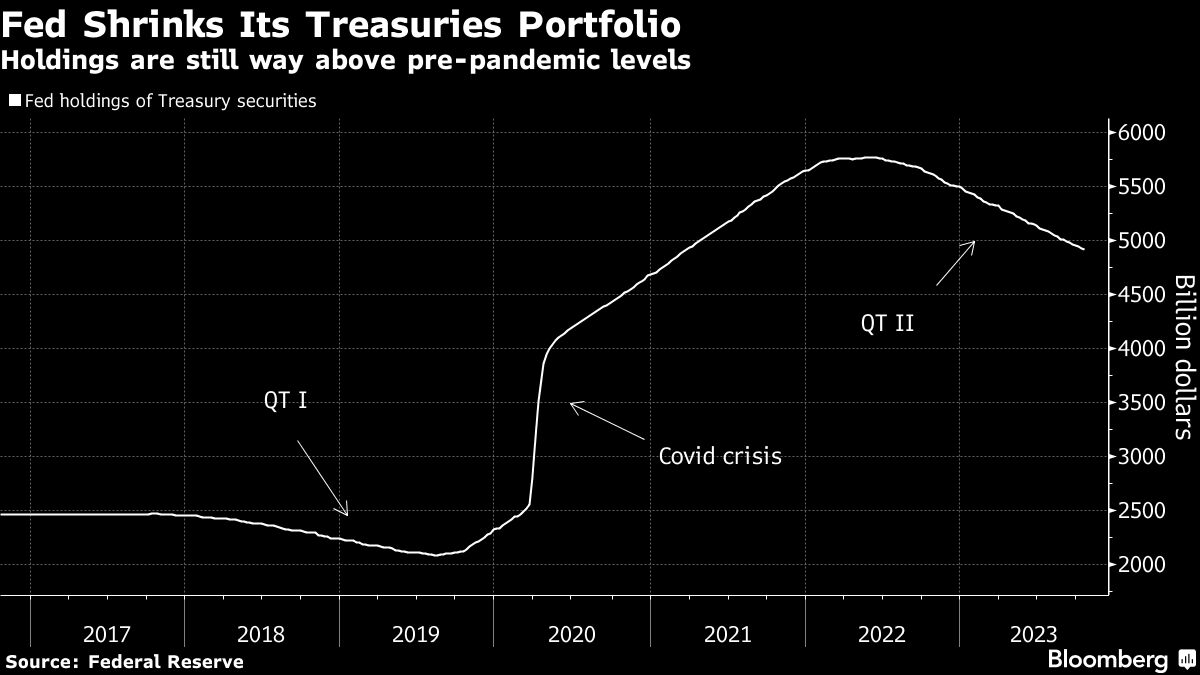

The Fed is shrinking its portfolio of government securities at a $720 billion annual pace, making the Treasury Department’s job of funding a near-$2 trillion federal deficit all the harder. Quantitative tightening, as the Fed’s program is known, ended earlier than officials expected the last time it was executed, and some market participants predict the same this time.

While Fed Chair Jerome Powell and fellow policymakers have indicated the surge in longer-term Treasury yields may reduce the case for continuing to hike the central bank’s benchmark interest rate, they’ve made no such suggestion for QT. Instead, they’ve said the process could keep going even after rate cuts have begun.

With 10-year yields surging past 5% for the first time since 2007 this week — and having climbed at the fastest pace since 1982 — the Fed may come under pressure to reconsider. At stake is the threat of surging borrowing costs ushering a harder landing for the economy, an outcome that would imperil riskier assets such as equities and corporate credit.

“They can change that very quickly if they need to — if the bond vigilantes continue to send a message,” Jack McIntyre, portfolio manager at Brandywine Global Investment Management, said of the Fed and QT. “Supply is important right now, and it’s supply during QT and that’s the interesting thing.”

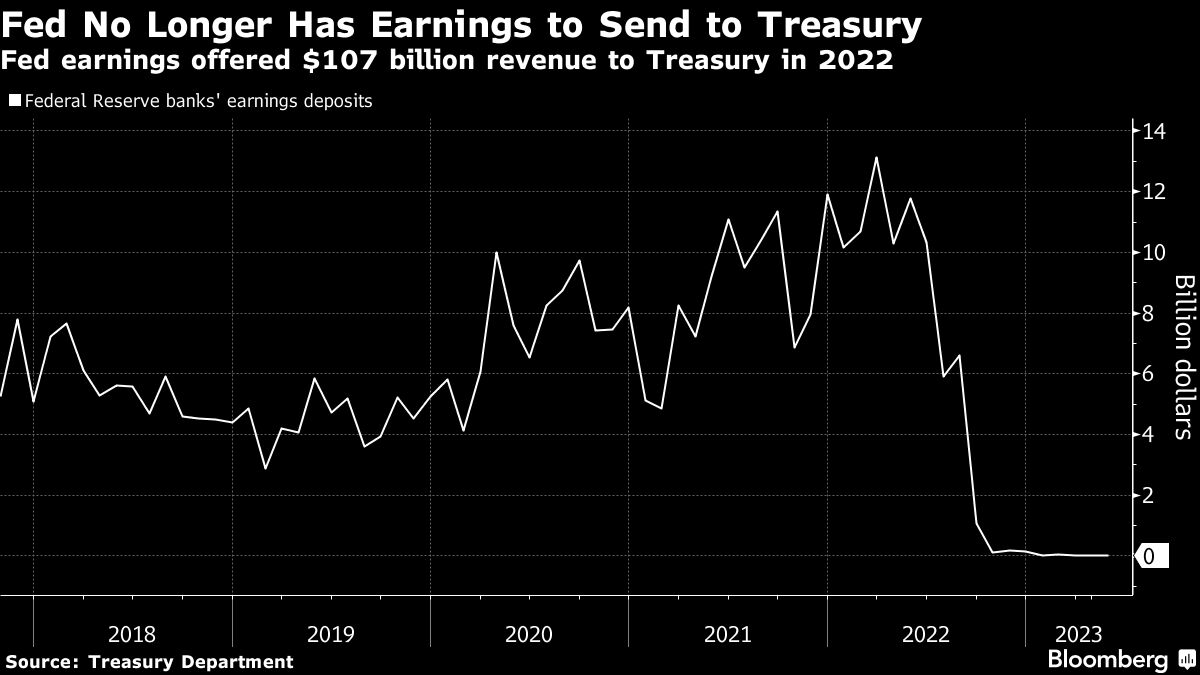

Powell told US lawmakers earlier this year he was “very conscious” of the need to shrink the Fed’s balance sheet and not just leave it bloated after each easing cycle. The cost of the Fed’s past quantitative easing is now clear: it’s paying high interest on the bank reserves that QE created — leaving about a $100 billion hole in the Treasury’s revenues.

And there’s still too much liquidity, by the calculation of former New York Fed President William Dudley. He estimates reserves in the banking system are about 12% of US gross domestic product, compared with 7% in September 2019.

“A lot of people in the market are saying ‘when will the Fed stop QT?’ — Not any time soon,” Dudley, a Bloomberg Opinion columnist, said on Bloomberg Television last week.

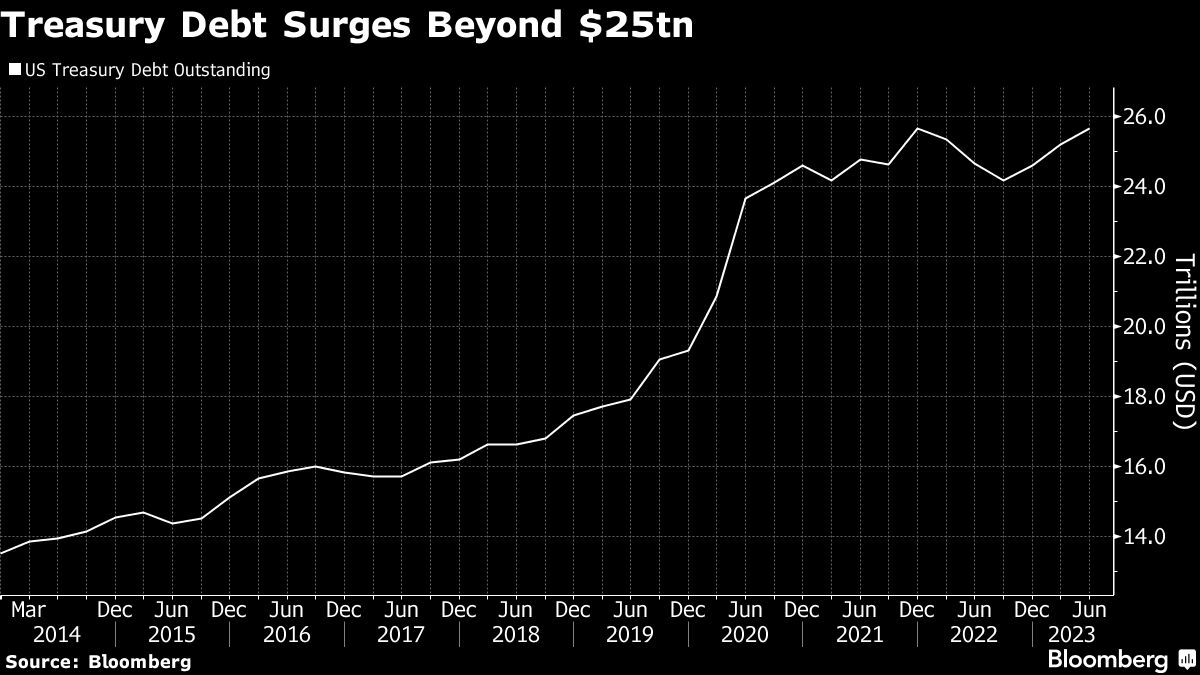

That offers no solace to the $25.8 trillion US Treasuries market, which has seen signs of growing reticence among buyers of absorbing the increasing sizes of longer-dated debt. Auctions of 10- and 30-year Treasuries were poorly received this month. And supply will keep increasing, thanks to a widening budget deficit. The gap reached $1.7 trillion in the fiscal year that ended last month.

“Further gradual increases in coupon auction sizes will likely be necessary in future quarters,” Josh Frost, the assistant secretary for financial markets at the US Treasury, said in remarks last month. The department’s latest borrowing plans are due for release on Nov. 1.

Meantime, other one-time big buyers are also missing in action, including Japanese investors. The marginal buyers nowadays are the likes of hedge funds and others that tend to be more price sensitive — one of the dynamics driving yields up.

A market where longer-dated yields climb in the absence of notable rallies means that QT “is potentially problematic,” said Alan Ruskin, chief international strategist at Deutsche Bank AG. It also could force “more bank hedging and unrealized losses for financial lenders, and higher bond yields,” he said. “That has the makings of a potentially vicious cycle.”

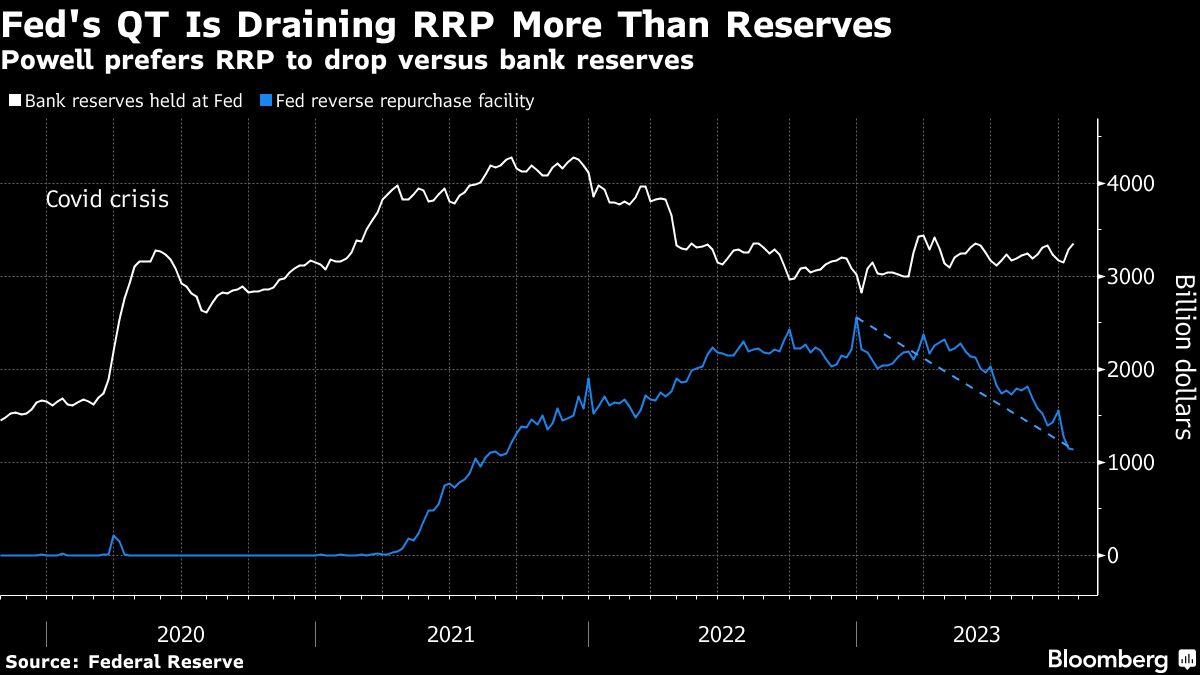

What’s offering comfort to Fed officials, for now, is that liquidity is mainly draining from the Fed’s reverse repurchase program, known as the RRP — where money market funds and others park cash — rather than from bank reserves, which are more closely tied to the economy. It was a slide in reserves in 2019 that triggered such problems in US financial plumbing that the Fed called off QT.

Policymakers have a dashboard of metrics they watch to know when reserves are reaching a scarce level, Dallas Fed President Lorie Logan, who previously oversaw management of the balance sheet at the New York Fed, said last week at a Money Marketeers event.

“There’s quite a bit of time still to go,” Logan said. For now, she said she’s focused on the RRP and “waiting for that to get down closer to zero.”

“Bank reserves have declined only modestly since the Fed’s quantitative tightening began last June,” said Daleep Singh, chief global economist at PGIM Fixed Income, who previously worked at the New York Fed and US Treasury. “But eventually, as the RRP facility is drained,” all else equal, “the Fed’s portfolio runoff will place downward pressure on bank reserves.” That may trigger problems for the financial system, he said.

Ten-year yields were around 4.82% late Tuesday in New York, up more than three-quarters of a percentage point since the end of August. Joyce Chang, chair of global research at JPMorgan Chase & Co., wrote in a note that QT is “an under-appreciated risk contributing to higher yields for longer.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Michael Mackenzie, Liz Capo McCormick, Jonnelle Marte