Bond traders who powered a ferocious rally in the $26 trillion US Treasury market are about to find out if they’ve gotten ahead of themselves.

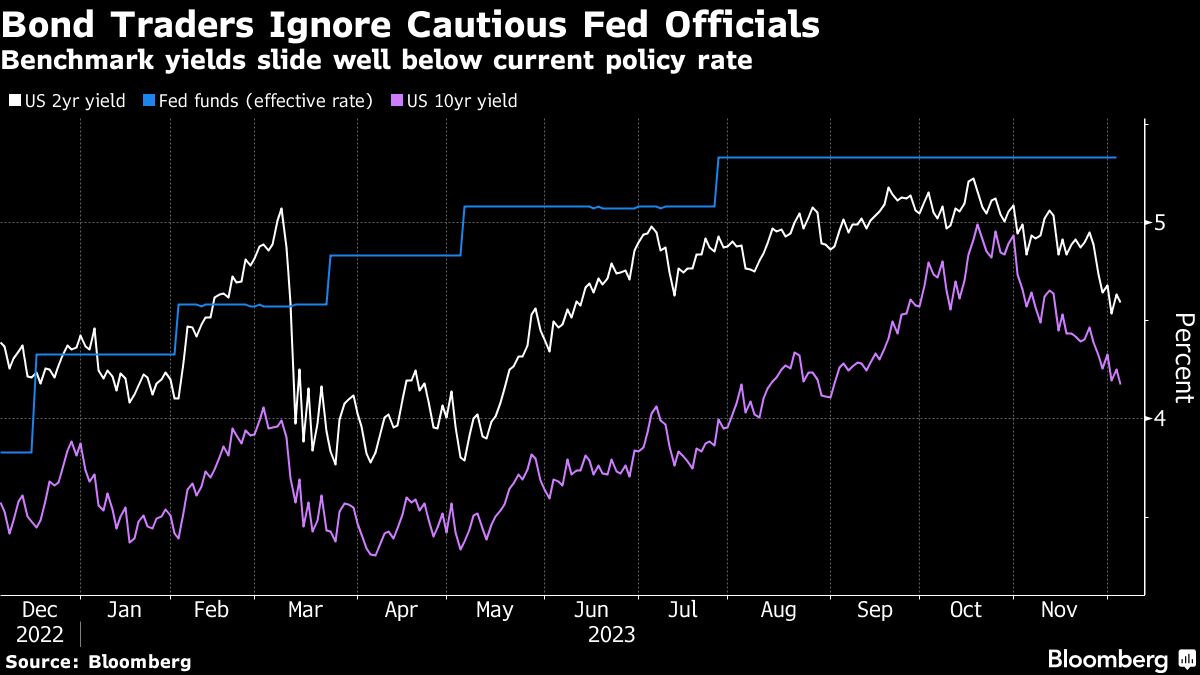

Softening inflation and employment data in the past month have convinced investors that the Federal Reserve is done raising interest rates and ignited bets that cuts of at least 1.25 percentage points are in store over the next 12 months. Treasury yields, which touched highs of 5% as recently as October, have declined sharply, with the US 10-year benchmark sliding more than three-quarters of a percentage point.

Now into the mix comes a key report Friday on the US labor market, which bulls hope will provide fresh evidence of a cooling economy. The bond market is already pricing in more than twice as much monetary easing in 2024 as Fed officials themselves, who while signaling they’re likely done raising rates have also been quick to caution that any talk of cuts is premature for now.

Traders remain unfazed: A JPMorgan Chase & Co. survey released earlier this week showed clients maintaining their largest net long positions since Nov. 13.

Friday’s report is expected to show moderating employment and wage growth in November but no major deterioration in hiring. Given the recent run-up in bonds, there’s a risk of a market reversal — at least initially — on any surprises that challenge traders’ bullish narrative.

“This rally in Treasuries needs to be validated,” said Kevin Flanagan, head of fixed-income strategy at WisdomTree. “The bar has been raised now in terms of the economic and inflation numbers coming in, and they’re going to have to show that the momentum of a slowdown is picking up.”

Payrolls probably grew by 183,000 last month, after increasing 150,000 in October, while the unemployment rate held steady at 3.9%, according to the median forecast of economists surveyed by Bloomberg. The end of strikes by autoworkers and Hollywood actors boosted payrolls last month by 41,300 after depressing them in October, according to the Bureau of Labor Statistics. After taking that into account, the underlying pace of payroll gains looks to be slowing.

“A stronger payrolls and still-elevated inflation expectations will likely apply bearish pressure to rates into next week’s US CPI report and the FOMC, ECB, BOE meetings,” said Evelyne Gomez-Liechti, multi-asset strategist at Mizuho International Plc. “US and EU market inflation expectations have been decoupling lately, after a period of being overly compressed. The divergence may continue if today’s numbers remain high.”

WisdomTree’s Flanagan adds a resilient jobs report “will continue to provide the Fed with cover as to not have to move prematurely in cutting rates.

It would also highlight a bond market perhaps running too far ahead of the central bank, and in danger of repeating a pattern seen during this latest tightening cycle of betting too soon on a Fed course change.

“Today’s payrolls report will set the scene for the rest of 2023,” said Padhraic Garvey, head of research for the Americas at ING, adding that the rapid move down in Treasury yields “really needs some validation” from the data.

On Thursday, a largely in-line report on US jobless claims left market expectations intact. The debate remains about the scale of rate cuts, an outcome ultimately driven by how much hiring and inflation slows. With a 10-year yield now below 4.2%, “the market seems to be priced for a strong near-term deterioration,” said John Brady, managing director at RJ O’Brien.

Fed Meeting

Fed officials are observing a self-imposed quiet period ahead of next week’s policy meeting, which also coincides with fresh data on US consumer prices. Armed with the latest jobs and inflation reports, the central bank will update its quarterly summary of economic projections and predicted path of interest rates.

Fed watchers believe the central bank will leave policy steady at its meeting next week and that it’s next move will be a cut. Some opined that Fed officials aren’t pushing back hard against expectations of easing next year because that’s the same direction they think policy is ultimately headed.

In almost any economic scenario — crash landing, soft landing, or no landing — inflation is likely to keep decelerating next year, driven by ebbing rental costs, Bank of America chief US economist Michael Gapen said. He expects Fed officials to pencil in three rate cuts for 2024 in the summary of economic projections they’ll release next week. “I’m calling it a shift from a hawkish hold to a dovish hold,” he said.

What Bloomberg Intelligence Says...

“Rate markets priced for deep cuts in early 2024 may get a shock next week if the Federal Reserve reiterates that it will keep interest rates at their peak well into next year,” Ira F. Jersey and Will Hoffman, BI strategists.

Subadra Rajappa, head of US rates strategy told Bloomberg Television they expect 150 basis points of cuts next year, with “a recession penciled in.” She said “risks are skewed asymmetrically in rates to the downside,” and they expect 3.75% on the 10-year by mid 2024.

The asymmetry means even a solid payroll number may only spur a limited rise in Treasury yields as traders stick to their guns and expect a slowing economy gathering momentum.

The market has “gone from a mode of selling into strength to now buying on the dips,” said Flanagan. Still, “to break through 4% on 10-year yields, given what has been priced now, you are going to need to see genuine signs of a hard landing at this stage of the game,” with payrolls either negative or barely positive.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Michael Mackenzie, Rich Miller