This year’s hottest derivatives trade, and perhaps also its most divisive, stole the limelight one final time for 2023 as market watchers cast zero-day options as the villains behind Wednesday’s rally-ending slump in US equities.

With the S&P 500 Index in overbought territory and turnover curtailed by looming holidays, observers suggested hefty volumes in put options that expire within 24 hours, known as 0DTE options, were sufficient to spark a pullback on the market, the sharpest in almost three months. Such trades would prompt market makers on the other side of the transactions to hedge their exposure, pushing the market lower, the argument goes.

“We have been wary of 0DTE options for quite some time,” Matthew Tym, the head of equity derivatives trading at Cantor Fitzgerald LP, wrote in a note with colleague Paolo Zanello. “Today we saw a late day selloff that, we believe, could have been caused by or certainly exacerbated by 0DTE SPX options. Certainly the market environment was ripe for it.”

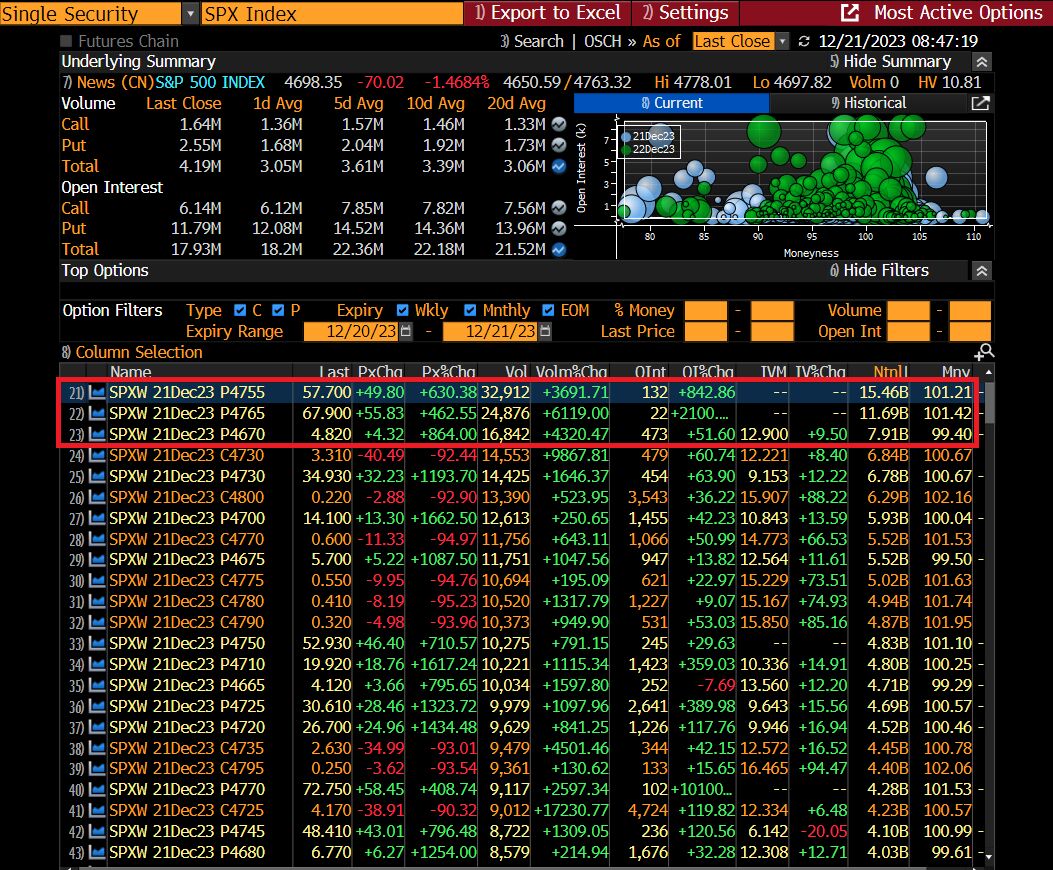

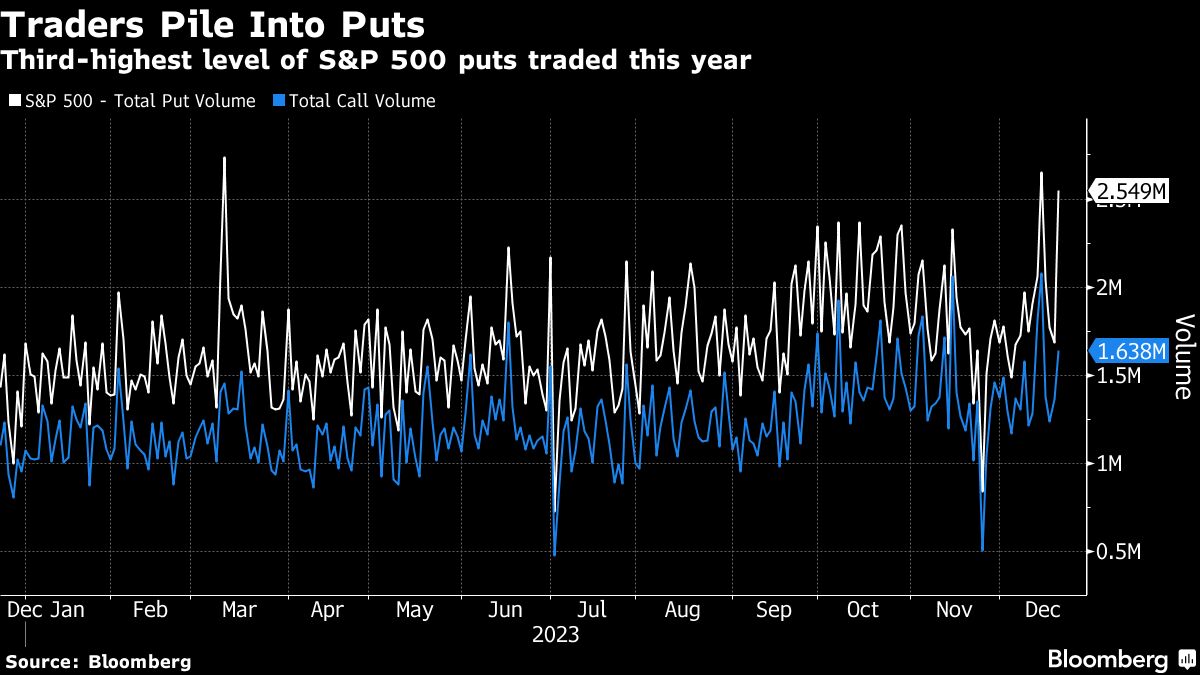

It was trades in put options, which give buyers the right but not the obligation to sell an underlying asset, around the 4,755-4,765 area that drew attention, they said. Data tracked by Bloomberg shows that puts on the S&P 500 with strike prices of 4,755 and 4,765 and expiring on Dec. 21 had notional value of $15.4 billion and $11.7 billion, by far the biggest value among put options as of last close. Wednesday’s total put volume on the S&P 500 was the third-highest of 2023.

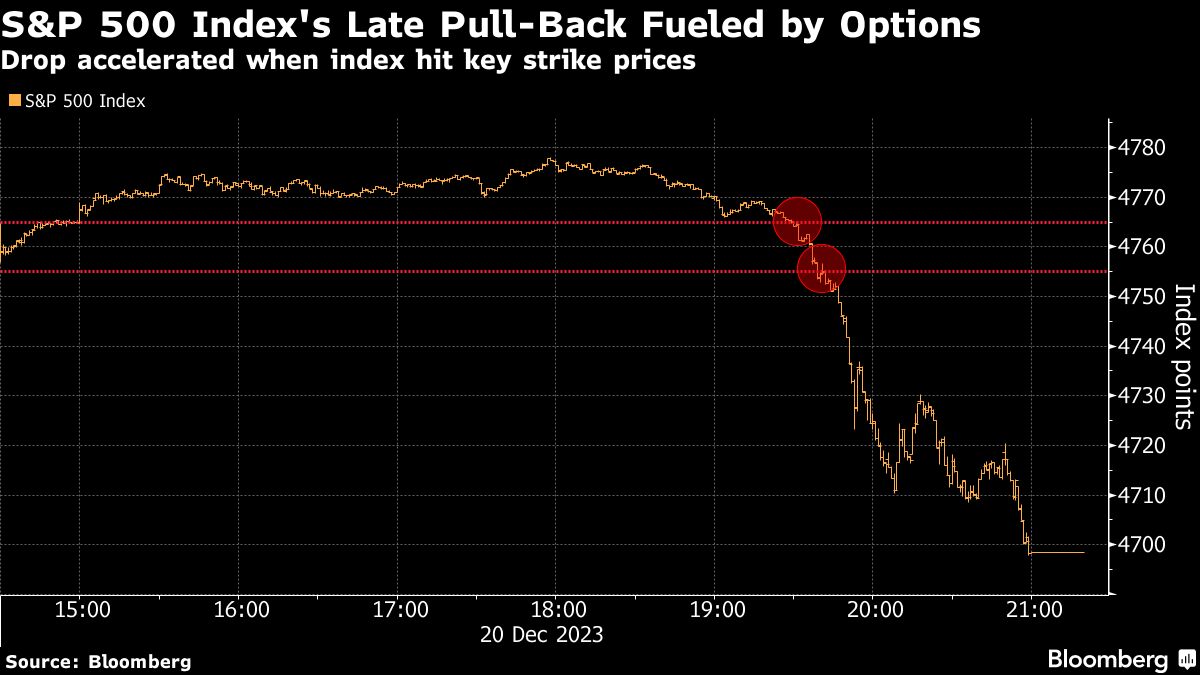

The S&P gauge slid from as high as 4,778.01 intraday to close at 4,698.35. Its 1.5% drop from the previous close was the biggest since Sept. 26. Relative strength readings on the gauge had been hovering at levels typically seen before a decline. Wall Street’s measure of volatility — the VIX — rose sharply from near multi-year lows.

A number of strategists had warned about the risk of a pullback following the market’s almost-uninterrupted rally since late October, which had left the indexes stretched. On Tuesday, RBC Capital Markets strategist Lori Calvasina said risks of a pullback were now flashing red, while Fed officials have been trying to temper expectations of rate cuts in the past week.

“Long put 0DTE on the S&P 500 is likely one of the catalysts that triggered the significant bearish reversal seen across the benchmark US stock indexes yesterday, on top of short-term overbought conditions and thin trading environment ahead of the year-end holiday season,” Kelvin Wong, a senior markets analyst at Oanda said.

Given the selloff on Wednesday, a number of investors may bet on a further drop by buying more zero-day put options, prompting market makers to ultimately sell the S&P 500 via futures and mechanically fuel the pullback, Wong said, “thus, creating a potential negative feedback loop back into the S&P 500.”

What Bloomberg’s Strategists Say...

“There was pretty good volume in 0DTE puts today, and when we went through the 4,755-4,750 level, there was a good volume of futures to sell. In an illiquid holiday market, it seems pretty clear that the appetite to absorb the flow was scant, and we were off to the races. At the very least it has reminded the street the playing in the stock market entails two-way risk, a fact that’s been all too easy to forget over the past seven weeks or so,” Cameron Crise, macro strategist.

Amid an explosion in trading of zero-day contracts for every weekday this year, debate continues to rage on their broader impact. For institutional investors, “zero-day-to-expiry” options offer a way to hedge short-term risk and pursue strategies based on darting in and out of positions. For retail investors, they offer a way to make big bets with little money down that can pay off quickly — or not.

While the likes of JPMorgan Chase & Co.’s Marko Kolanovic have warned that the popularity of the product risks reprising past shocks such as the 2018 Volmageddon episode, Cboe Global Markets says there’s scant evidence that the buying and selling of the derivatives is destabilizing the underlying market.

Options analysis firm SpotGamma said in a post on social media platform X that 0DTE options drove the decline in the US equity benchmark. Rocky Fishman, founder of derivatives analytical company Asym 500, pointed out that the daily 0DTE volume was the highest since early October — $900 billion — which was noteworthy given the lack of specific economic news during the day.

Its a 0DTE driven plunge in the S&P. you can see the spread here between bearish 0DTE flow (teal) is identical to that of all flow (purple) informing us that the bulk of flow on this downdraft is all todays expiration. pic.twitter.com/WFGuRY2Cj8

— SpotGamma (@spotgamma) December 20, 2023

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul Dobson, Michael Msika