US federal government debt ended 2023 at a record $34 trillion. The worries are bipartisan, with both Republicans and Democrats hearing about out-of-control borrowing from their constituents. In fact, almost six in 10 Americans say reducing it should be a top priority, according to a survey by the Pew Research Center. So, it’s not a surprise that Congress is moving closer to passing a budget for fiscal year 2024 that would cap spending at $1.59 trillion which is a bit less than the $1.7 trillion in fiscal 2023.

But many of reasons why lawmakers and voters have concerns about the size of the nation’s debt – concerns that have been around for many decades - are misguided and undermine a constructive conversation about the priorities for the country. Debt is neither inherently good nor bad. As such, the question is not what’s the right level of borrowing, but rather what’s the economic return on the borrowing or the societal goals it advances.

Take the child tax credit. When the Biden administration increased borrowing to expand the deduction to as much as $3,600 per child from its previous amount of $2,000, the child poverty rate tumbled to as low as around 5% in 2021 from almost 13% in 2019, making it easier for families to provide the basics, such as food, clothing and school supplies. When the program expired at the end of 2021, the rate shot up to 12.6%. Or consider the tens of billions of dollars in grants and contracts the government handed out help fund the development of mRNA technology that was used in the Covid-19 vaccines. The return on that investment to society is incalculable. And would the economy have been so surprisingly strong the past few years without the extra borrowing, avoiding a damaging recession that would have thrown millions out of work?

For an example of deficit spending that might be viewed as bad, research suggests that tax breaks for companies, which decrease tax revenue and thereby increase the budget deficit, may exacerbate income inequality rather than the intended outcome of encouraging companies to boost capital spending to strengthen their businesses and the economy.

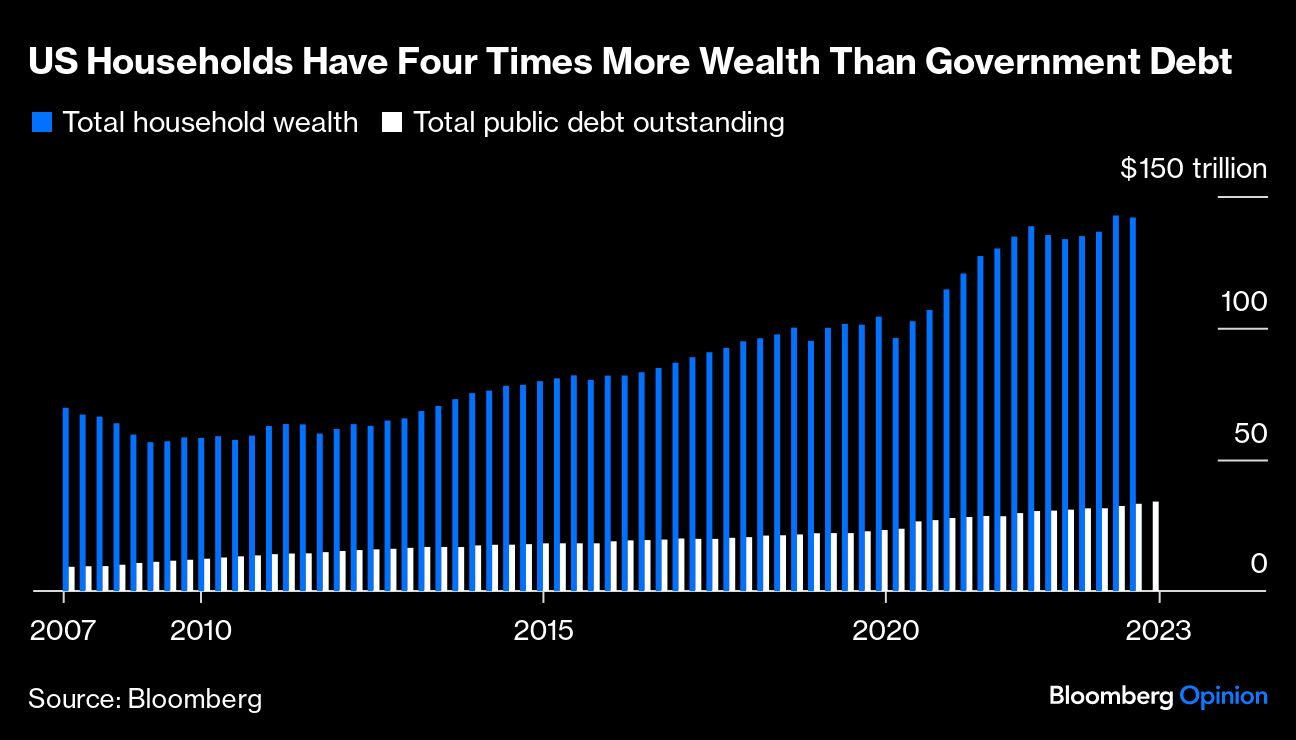

Regardless, the amount of US debt must be put in context. Yes, $34 trillion is big number, but $142 trillion is even bigger and much more important because it represents the total wealth of Americans —a massive resource that helps fund government debt and deficits.

The pessimists will counter by pointing to the amount of interest the government is paying to service its debt. In fiscal 2023 that ended Sept. 30, the figure was also a record - $882.6 billion, to be exact. Again, context matters. Although the amount has doubled since 2016, it was a manageable 3.4% of gross domestic product, less than the 4.3% level of the late 1990s when the government was running budget surpluses instead of deficits like now, according to data compiled by Bloomberg.

Sure enough, whenever there’s a debate about government borrowing, it’s inevitably put in the context of the financial constraints faced by households. But the correct context for how the federal government makes decisions about debt is not the same as how households make decisions about debt. Stephanie Kelton, professor of economics at Stony Brook University, rightly argues that this is one of the many “ myths” embedded in the discussion about the federal debt. The government can easily service its debt because of its unlimited taxing authority and ability to issue more US Treasury securities to repay maturing securities. Conversely, households can’t just increase their incomes to a desired level at will.

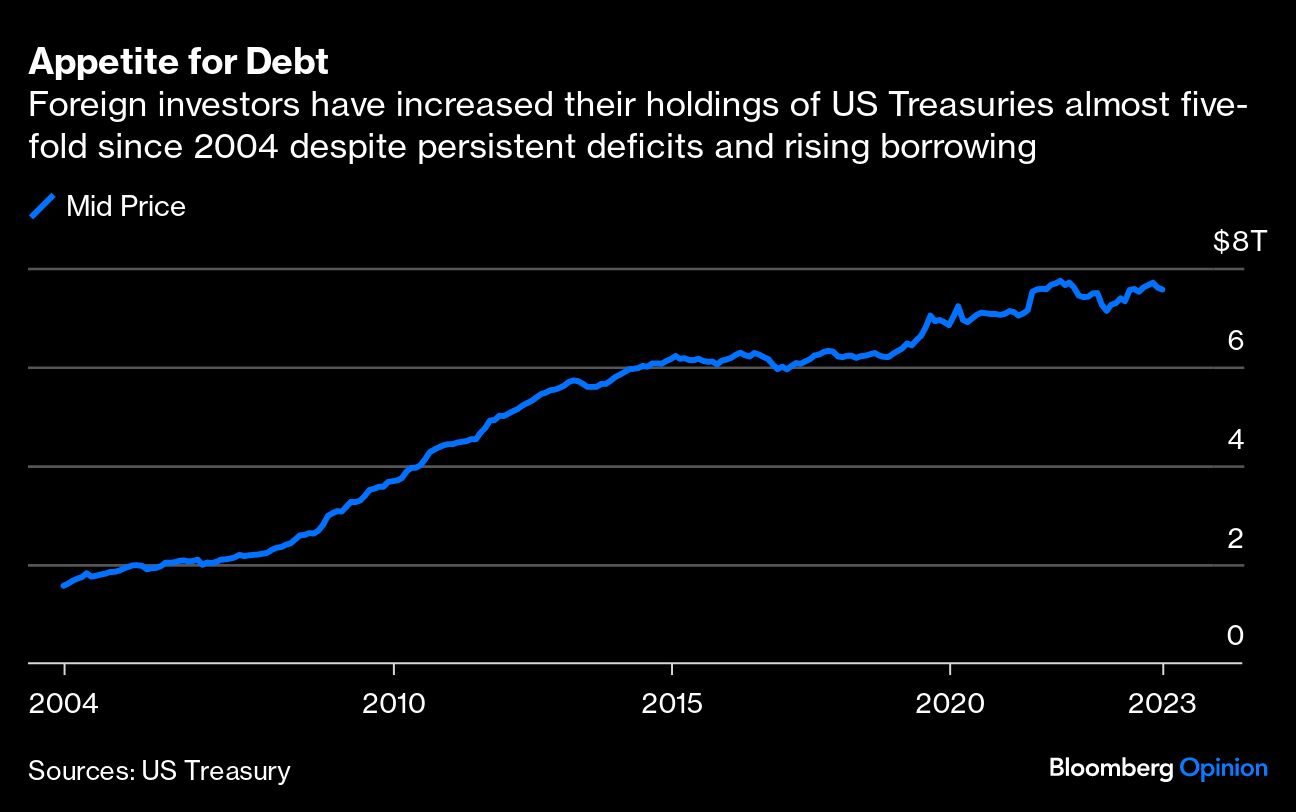

Rather than the level of borrowing, political gamesmanship over the federal debt is a far greater risk to the economy. The United States has earned what’s known as an “ exorbitant privilege” in the post-World War II era, meaning that there is always demand from investors around the world for US Treasuries in good times and bad. That privilege was earned by the US promoting a dynamic economy, adhering to the rule of law and being a stable democracy. As such, the dollar accounts for around 60% of global foreign-exchange reserves, three times that of the No. 2 reserve currency, the euro.

More important than reducing the debt or balancing the budget would be efforts by lawmakers to protect the US’s exorbitant privilege. Those in Congress creating high drama over the nation’s borrowing and budgets have caused some to question whether Treasuries are really the world’s safest assets. In stripping the US of its AAA credit ratings, both S&P Global Ratings and Fitch Ratings cited concern about rising political dysfunction following several debt-ceiling standoffs.

Politics is the real threat, not the level of borrowing. A country that prioritizes the size of the federal debt has bad priorities.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Claudia Sahm