Investors’ lingering fears of recession have prompted Wall Street banks to hawk a complex hedge: exotic options that pay off if stocks fall and bond yields also drop.

These options are relatively cheap now, in part, because correlations between equities and rates have been low. But investors should also consider them because US stock valuations look stretched by many measures, according to banks including JPMorgan Chase & Co. and Citigroup Inc. On top of that, questions about how soon the Federal Reserve will start cutting rates could result in wild market swings.

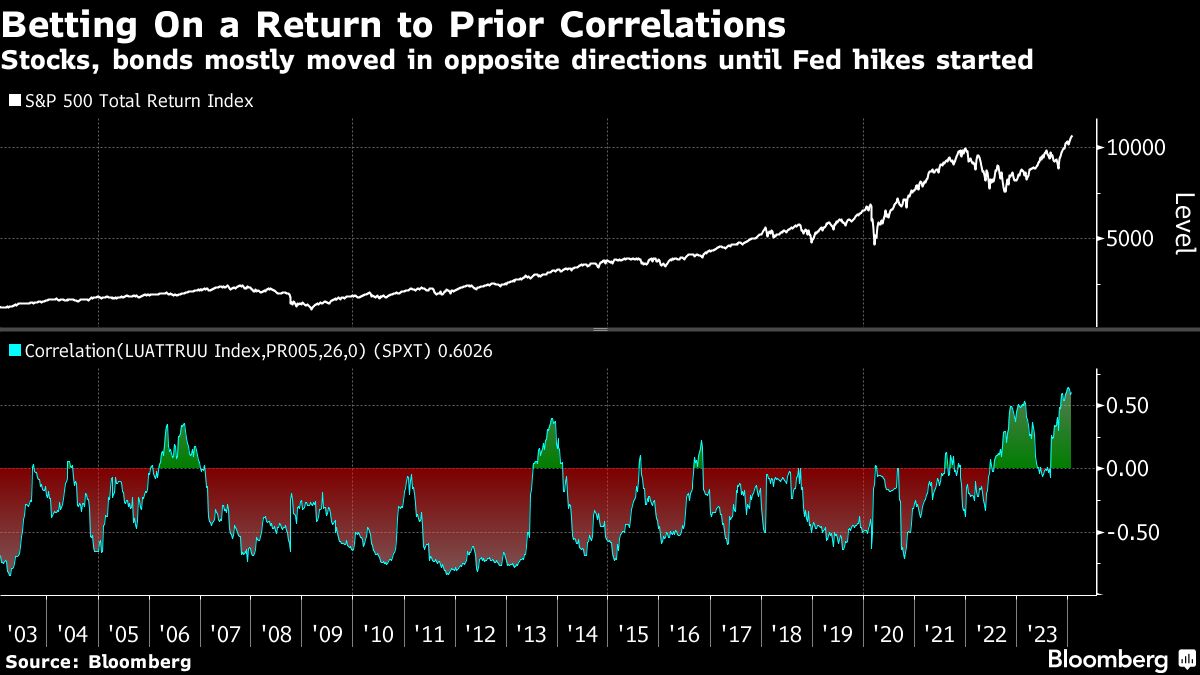

Buying the options amounts to betting that stock and bond prices will move in opposite directions. That relationship has been true for much of the last 20 years, a period of relative price stability, but inflation often breaks down that inverse movement, and the last two years were no exception: the Federal Reserve started hiking rates and asset values broadly fell in tandem.

Exotic options trades are growing a little more popular because “there’s a feeling we might be going back to a more normal order of things. That does generate some attention,” said Peter van Dooijeweert, head of defensive and tactical alpha at Man Group, a hedge fund manager.

Here’s one example of how the trade might work: An investor buys a put option, protecting against the S&P falling by 10% or more.

But the option only kicks in if the two-year swap rate, at around 4.2% as of Monday, falls about 0.5 percentage point from current levels.

For $100 of index value guaranteed, or notional value, such a contract costs 48 cents, according to data compiled by Bloomberg. Meanwhile, a simple put that protects against the S&P falling by 10% or more — yet is not tied to rates — will set an investor back by 81% of the notional. So the exotic contract comes at about a 40% discount.

“They’re interesting because of the environment we’re in,” said Stuart Kaiser, Citigroup Inc.’s head of US equity trading strategy, adding that the firm anticipates a recession in mid-2024. In such a scenario, options that pay out if stocks dip and bonds rally look attractive.

“We just went through a big inflation scare,” Kaiser said. “There’s still uncertainty about how this is going to play out. If a client has a strong view either way on that outcome, this is a way for them to express that view.”

Banks are pitching these trades to sophisticated investors like hedge funds that can trade over-the-counter derivatives. Because the positions tend to be custom-made to an investor’s specifications, exiting them can be relatively more expensive than it might be to trade a simpler listed option.

Some investors are skeptical. Man Group’s van Dooijeweert said it’s better to get downside protection that isn’t tied to rates, because plain equity puts are still relatively cheap.

“Why be cute?” asked van Dooijeweert. “Our general view is we should only add complexity when we get enough of a discount for it.”

But to some investors and strategists, the potential for cheaper hedging can be attractive. Nitin Saksena, head of US equity derivatives research at Bank of America called out S&P 500 puts tied to two-year rates. Depending on how one constructs the contracts, the options could pay off if markets prove wrong about how quickly the Federal Reserve cuts rates or if the central bank does cut rates aggressively in the case of recession.

“What feels different is just how much inflation, policy and rates has been front and center in the past two years,” Saksena said. “People have flocked to the product because of how volatile and active the macro environment has been.”

A message from Advisor Perspectives and VettaFi: Advisors: You're Invited to Exchange! Nothing would be a better start to the new year than if you joined us at Exchange, an in-person conference for members of the financial services community in Miami, Florida on February 11-14th. For a limited time, we're offering you a free Exchange ticket!* Register today with code WINTER24 to claim your pass.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Carly Wanna, Elena Popina