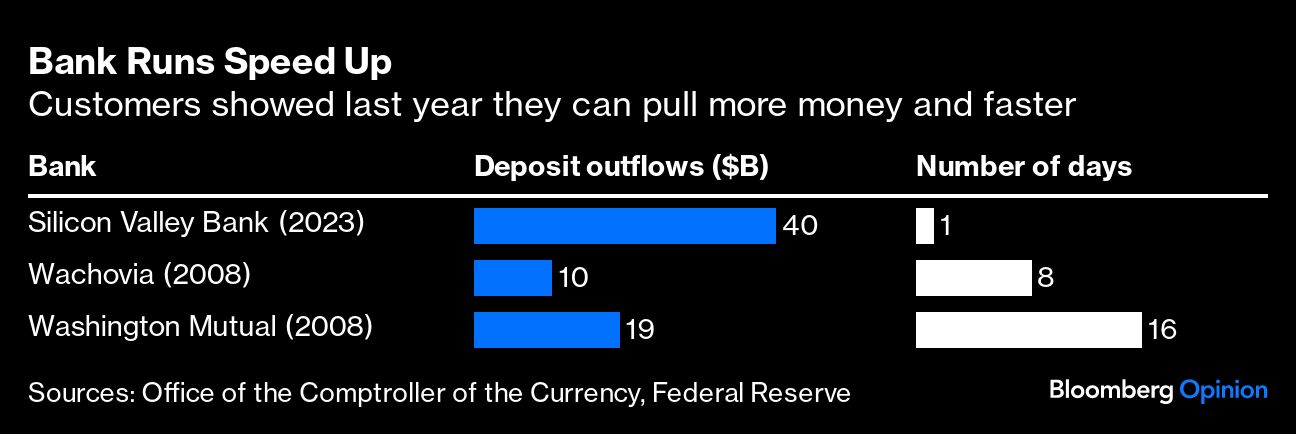

As New York Community Bancorp Inc. scrambles to shore up its capital to deal with potential loan losses, analysts are watching to see if depositors pull their money. It’s been almost a year since more than $40 billion was withdrawn from Silicon Valley Bank in a single day, with little consensus on a long-term solution for lenders faced with such a speedy digital bank run.

The good news is that regulators have recently hit on a viable strategy to address this risk. The bad news is that they might not take it far enough.

Bank runs remain thankfully rare, largely because deposits up to $250,000 are guaranteed by the Federal Deposit Insurance Corp. Yet customers with larger, uninsured balances are still prone to flee at signs of danger. Those deposits amounted to almost 45% of the total as of 2022. (In NYCB’s case, the latest figures were $22.9 billion, or 28%.) Some uninsured deposits are in business accounts used to pay workers and suppliers; it’s the other, nonoperational accounts that tend to be flightiest in a crisis.

To manage sudden withdrawals, banks keep some of their money in liquid assets, such as Treasuries, which are normally easy to sell or borrow against to convert to cash. In a true panic, though, buyers and lenders sometimes withdraw. That’s where central banks step in as lenders of last resort, supplying cash to solvent depositories as loans against good-quality collateral.

The Federal Reserve’s traditional tool for this task is the discount window. The problem is that the window has acquired a stigma over the years, making banks reluctant to access it for fear of spooking creditors, depositors and investors. Instead, they’ve turned to alternative lenders such as the Federal Home Loan Banks, public-private hybrids that, unlike the Fed, can face their own funding challenges during market disruptions. Some banks, including SVB, ceased to even have systems in place to borrow from the discount window in an emergency. The Fed has ended up creating new special lending programs each time a crisis comes along.