How many Wall Street buzzwords can you fit into one security? The limit is being tested by a new breed of options-fueled exchange-traded funds making inroads with the retail crowd.

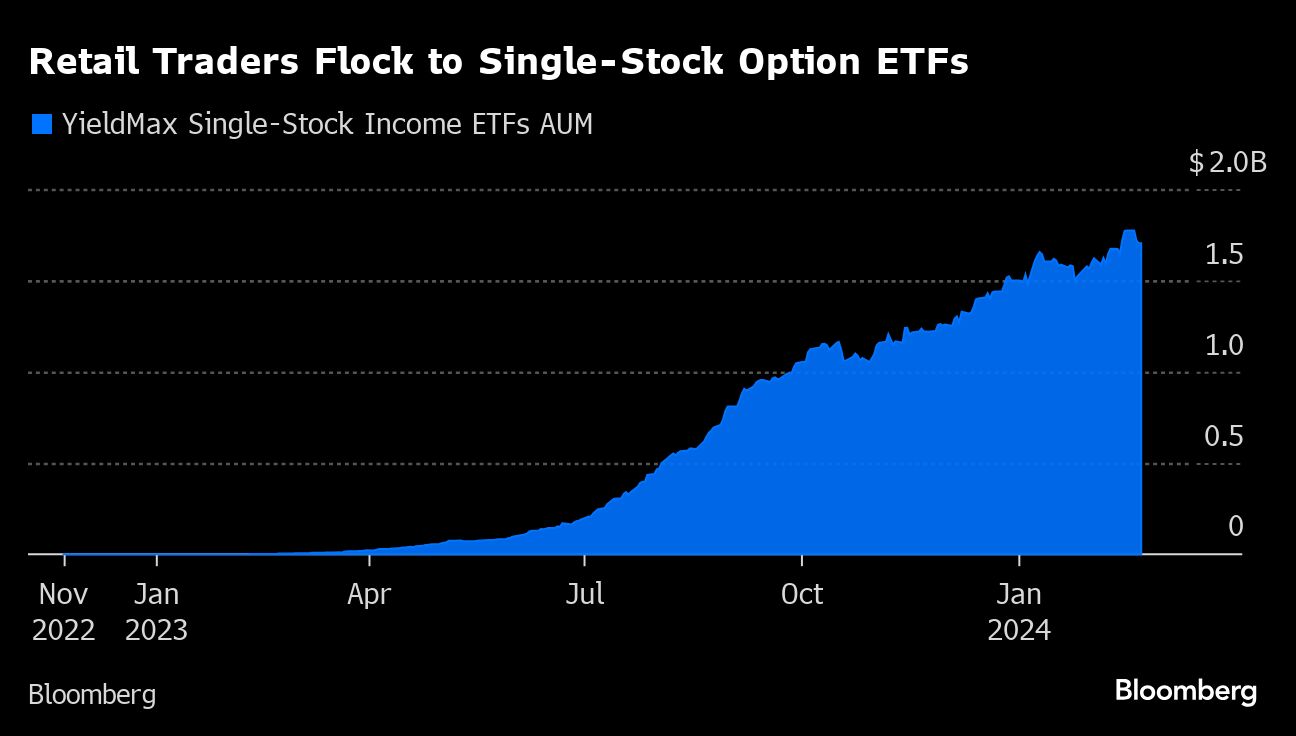

Nosebleed yields. Elevated volatility. Single-stock ETFs. They all come together in a parlay of complex risk taking marketed with mundane labels like the “option income strategy,” with around $1.7 billion flowing into such products since catching on last year. Issuers are planning more. Skeptics wonder if buyers know what they’re getting into.

The ETFs are the high-octane cousin of booming option strategies that trade in volatility: Hybrid funds that hold indexes of stocks and sell derivatives against them to generate yield. Unlike their index-linked brethren, though, the new incarnations put all their chips on one company, using the ETF structure to layer multiple options trades that are sold as a one-stop, cash-spewing investment.

Fans love the payouts, and overseers say the ETFs do what they’re supposed to do: generate income. “We didn’t invent covered calls,” says Jay Pestrichelli, chief executive of Zega Financial, a sub-adviser and portfolio manager for strategies offered by YieldMax funds. “They’ve been around for decades.”

Yet critics say the complexity masks often desultory returns over time, warning the dividends can be offset by losses elsewhere, making the investment proposition a little hard to fathom.

“People see these bonkers distribution figures and start counting their riches, not realizing that there’s potentially a significant offset,” said Jeffrey Ptak, chief ratings officer at Morningstar Research Services. “There is the question of why someone would want to engage in this type of activity to begin with.”

While defying easy explanation, the ETFs resemble a situation where someone owns a stock and sells side bets on how much it will rise or fall. Money received on those wagers is sent back to owners depending on how much the shares swing. Overseers bill them as a way to pocket regular income while foregoing potential upside, a trade with appeal to anyone who sees a slow and steady upside for the stock.

One of the highest-yielding single-name products on paper is the YieldMax COIN Option Income Strategy ETF. Its annualized announced gross dividend reached a high of 168.8% at the start of this month, amid fresh pangs of volatility in the Coinbase Global Inc. stock price. These kind of yields have made the securities a topic of intense online interest and a catnip for retail investors.

Daniel Cash, a 35-year-old real-estate contractor in Massachusetts, says he’s sent $30,000 to the products in his brokerage and retirement accounts.

“They are paying outrageous dividends,” Cash said in a telephone interview. “These funds are just destroying the competition.”

But while yields sent out by ETFs running the strategy may be high, they are far from pure upside for people who own them. Like most dividends, the payouts are closely tied to the price of the underlying holdings, with gains in one impacting the value of the other.

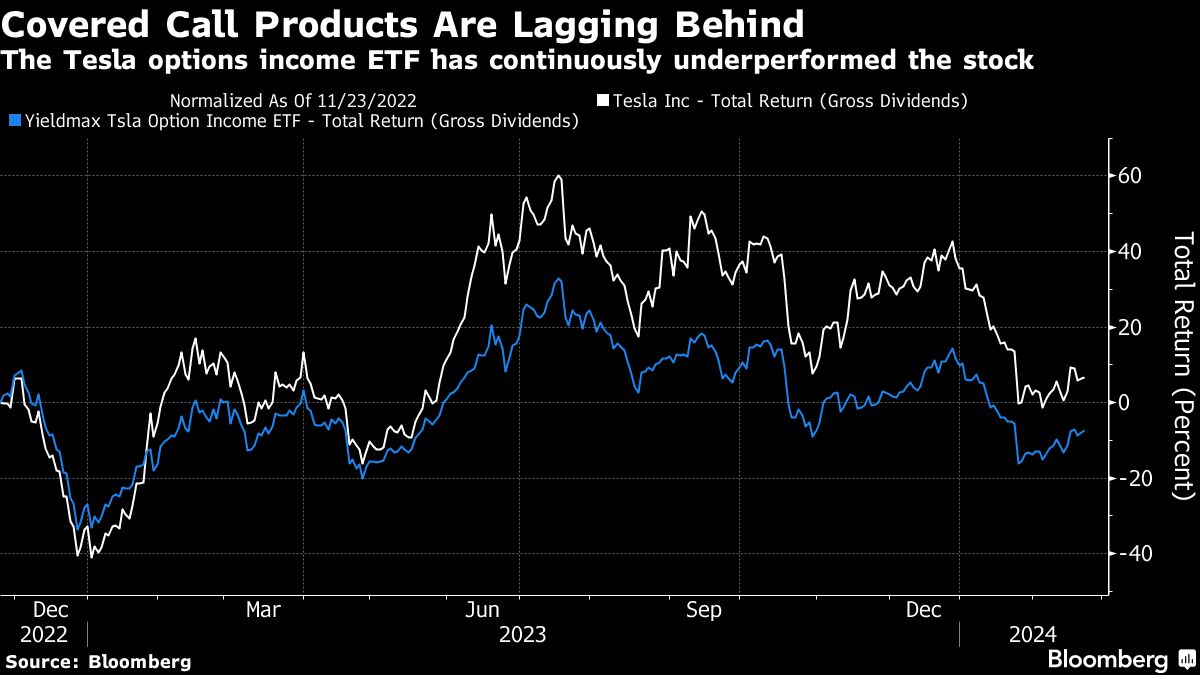

A security such as the Yieldmax TSLA Option Income ETF illustrates the issue. Over the last 12 months the fund dangled a “89% yield” when viewed in isolation. But alongside that came a steep decline in the price of the ETF itself. The result was an all-in loss of around 2% — almost identical to the drop in Tesla itself over the same period.

“They’re looking for these big shock-and-awe income numbers but at the end of the day, if you don’t make any total return, it’s really uninvestable,” said Hamilton Reiner, who runs the sprawling $32 billion JPMorgan Equity Premium Income ETF, an options-enhanced strategy tied to the S&P 500. “No matter how you get there — income, appreciation, something else — you need to make money.”

That critique misconstrues the purpose of the ETFs, which isn’t to track the underlying but rather to serve as a yield-generating alternative to equity allocations, says Pestrichelli of Zega Financial. It’s a mistake to compare their performance against the stocks they’re linked to, the thinking goes.

“It’s an alternative. It’s an aggressive alternative. It’s almost like the underlying just happens to be the vehicle we’re using to generate the yield but it’s not about beating the underlying,” he said. “It’s not even stated in the prospectus. The prospectus is about income.”

A look at TSLY’s holdings shows most of its assets are held in Treasury bonds, essentially serving as collateral for the options bets that the strategy employs. The ETF has a long so-called synthetic options position on Tesla — combining puts and calls with the same strike price. It also shorts Tesla call options to help generate the income the funds pay.

Securities that buy and sell options while holding a slug of Treasuries may be a reasonable, if fancy, way of meeting the primary objective stated in the YieldMax prospectus to “seek current income.” But getting a handle on how the ETF is apt to move in a given set of economic and market circumstances is a tall order, even for experts.

“It’s an income product. Nobody should try to time it,” said industry expert Dave Nadig. “You’re exposed to all of the equity risk and you sacrificed upside in exchange for some level of income.”

Even the question of how much yield an investor should expect to collect is complicated. The YieldMax products aim to generate income that matches the implied volatility of the underlying stock, so if Tesla shares have an implied volatility of 60, the target for the the annual distribution rate will be 60%. In other words, the more the volatile the equity, the higher the potential payout is — in isolation.

“Even though this is an easy to access ETF, it doesn’t simplify the dynamics of the underlying option strategy,” Pestrichelli said. “Knowing things like the impact of implied volatility, upside limitations from call selling, and downside risk are important characteristics investors should understand before investing.”

Such single-name yield enhancement products are part of the broader covered-call ETF universe of volatility-linked strategies that offer income along the way. While the new versions employ similar strategies to securities like JPMorgan Equity Premium Income ETF (JEPI) and Global X Nasdaq 100 Covered Call ETF (QYLD), many of the single-stock names don’t own the underlying security outright. They also have none of the diversification a product based on an index offers.

“The complexity is harder to assess,” said Rocky Fishman, founder of derivatives analytics firm Asym 500. “It’s hard for investors to know exactly what options positions are in the funds at a given time.”

Since inception two of the most popular products have lagged behind their underlying stocks. CONY has returned 65% since its arrival in August but has trailed Coinbase’s 116% gain for the same period by a big margin. TSLY has had a 7% loss on a total return basis since its November 2022 launch, while Tesla Inc. has returned 8% for the same period. Meanwhile, YieldMax announced a reverse stock split effective at the end of February as a way to boost the ETF’s share price, which has tumbled in recent months.

Aaron Faby, a 43-year-old tech professional, has first-hand experience of the volatility. He bought options-income ETFs tied to Coinbase and Tesla after hearing about beefy income payments on YouTube. The hefty dividend started coming in, but the losses were so severe that the income wasn’t enough to compensate for the price drop.

“I was in the red the whole time,” said Faby, who sold all his shares of such products less than five months after the initial purchase. “The fund kept going down over time — so I realized I was just getting my money back and paying taxes on it.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Denitsa Tsekova, Katie Greifeld