A steady march higher in markets was snapped by a stretch of jarring volatility as traders gave hints there’s a limit to their appetite for hot economic data.

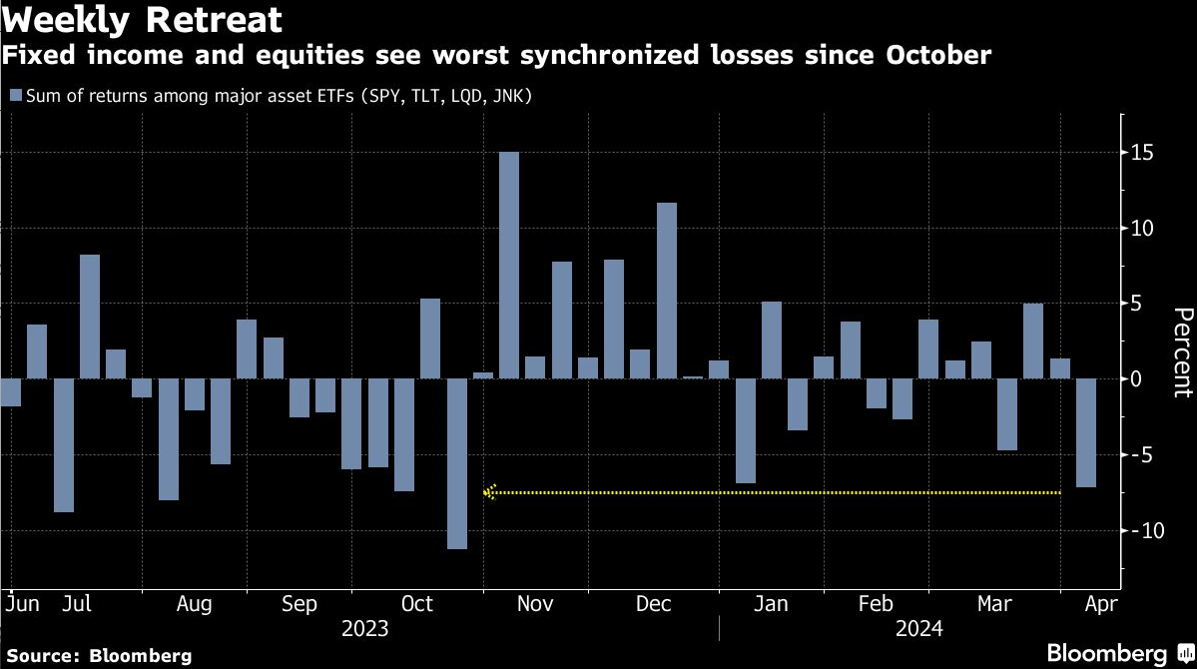

While a Friday rally in equities spared cross-asset investors their worst week since 2022, it capped a series of extreme market moves. Stocks and bonds staged their worst synchronized drop of the year on Monday and Tuesday, while Thursday saw the biggest reversal of an S&P 500 rally since August. An exchange-traded fund tracking long-dated Treasuries suffered its worst week since October as 10-year yields reached the highest in more than four months.

Rather than recession anxiety, the culprit was robust reports on job openings and factory output — as well as a surge in oil — that raised doubts the Federal Reserve has room to cut interest rates anytime soon.

An emerging issue for bulls is the impact of markets themselves on the economy, according to Torsten Slok, the Apollo Global Management economist who has repeatedly warned that gains in asset prices are working against central bankers’ goals.

“The tailwind from easing financial conditions is overwhelming and neutralizing the rate hikes from last year,” Slok, who in March predicted no rate cuts this year, said in a phone interview. “It’s not surprising that the economy is re-accelerating and, therefore, rates will have to stay higher.”

The broad rally across assets that has added $13 trillion in financial wealth since October looked shakier this week as inflation angst resurfaced, with Brent crude climbing above $90 a barrel. Another solid jobs report Friday on the heels of an unexpected expansion in manufacturing triggered a hawkish repricing in bonds. Traders are now pushing back bets on when the Fed will start cutting rates to September, paring odds for June or July.

The ICE BofA MOVE Index, which tracks expected turbulence in US bonds via options on interest-rate swaps, bounced from a two-year low to snap a six-week slide.

Subtle shifts in investor behavior appeared in the stock market, marking a switch after traders spent months buying the dip and piling in to bullish options. On Thursday, when the S&P 500 wiped out a 0.8% gain to end the session more than 1% lower, the Cboe Volatility Index, a gauge of options cost known as VIX, jumped to its highest since November.

“Clearly, the market is getting anxious about what the Fed is going to do,” said Raphael Thuin, head of capital market strategies at Tikehau Capital. “The Goldilocks market that investors are hoping for may not be a reality.”

In the eyes of contrarians who have watched asset gains spread to risky corners from cryptocurrencies to meme stocks, a sweeping retreat is overdue. Bolstered by optimism that the Fed will be able to bring inflation toward its 2% target without snuffing out growth, $176 billion of fresh money was poured into fixed income and equity ETFs in the first quarter, more than doubled from a year ago, data compiled by Bloomberg Intelligence show.

And Citigroup Inc.’s Levkovich Index — which tracks reams of data from retail sentiment to options trading and fund positioning — recently entered euphoria territory for the first time in more than two years.

Stretched sentiment in and of itself may not be reason enough for equity gains to reverse. But as the bull camp gets crowded, weak hands can be quickly vanquished. Hedge funds, for instance, stepped up bearish wagers against individual stocks, with short selling rising at the fastest pace in six months, according to data from Goldman Sachs Inc.’s prime brokerage unit.

Adding to trepidation is a chorus of policymakers including Fed Chair Jerome Powell signaling that they are in no rush to lower interest rates. Most notable was Minneapolis Fed President Neel Kashkari, who — though not a voter on monetary policy this year — still managed to raise eyebrows by saying interest-rate cuts may not be needed this year at all if progress on inflation stalls. Dallas Fed President Lorie Logan on Friday said it’s too soon to consider cutting interest rates, citing recent high inflation readings.

“This is definitely a ‘good is bad’ environment,” said Michael O’Rourke, chief market strategist at JonesTrading. “Although Chairman Powell said that recent hot inflation and economic data do not ‘materially change the overall picture,’ there is some change. Several more hot data points are likely to tip that balance and push rate cut expectations further out.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Isabelle Lee, Lu Wang, Denitsa Tsekova