US Dollar’s Extended Reign Delivers Stark Wake-Up Call for Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe world’s financial markets are encountering a force they didn’t bet on for 2024: A strong dollar is back and looks set to stay.

Having entered the year predicting the greenback would decline, investors have been forced into a rethink by a red-hot US economy and sticky inflation requiring the Federal Reserve to hold off cutting interest rates.

With the International Monetary Fund predicting output stateside will grow at twice the clip of its Group-of-Seven peers, talk of “US exceptionalism” is rife and supporting stocks and bond yields, adding to the dollar’s appeal. And in a time of mounting geopolitical strife, the currency still stands as the ultimate currency haven.

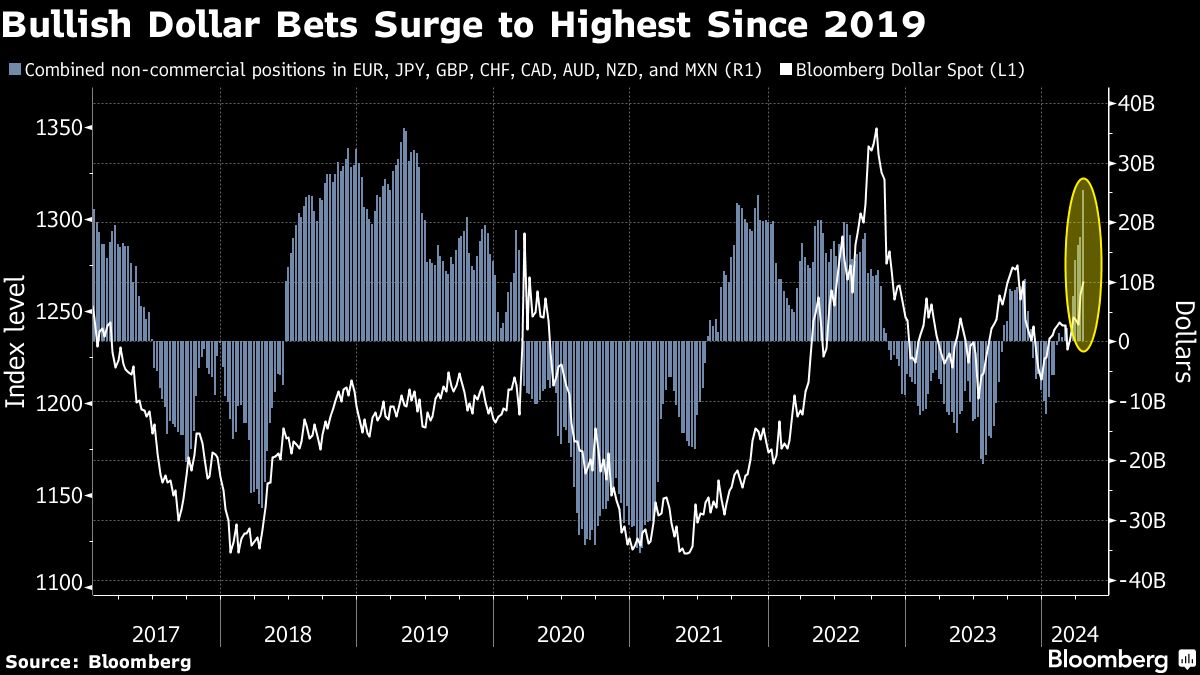

A Bloomberg dollar index has gained more than 4% this year, reflecting advances against all major developed and emerging-market counterparts. One popular gauge of trader sentiment pointed bearish at the start of the year, but has since flipped to become the most bullish since 2019, according to data from the Commodity Futures Trading Commission.

Among those recalibrating their strategies for the dollar is the world’s second-biggest money manager Vanguard Group Inc., which is now calling for sustained strength. UBS Asset Management says the dollar has probably got further to rise despite being 20% more expensive than it’s typically valued. Meantime, Wells Fargo Investment Institute capitulated on forecasts for weakness by year-end and now reckons it will extend its climb through 2025.

“If other countries can’t match the growth and inflation of the US, there’s just no other option than to buy the dollar,” said Ales Koutny, head of international rates at Vanguard. “What was a very tactical trade for us before has become much more of a long-term structural view regarding sustained dollar and US economic strength.”

The greenback’s resurgence has come on the back of a slew of signs that the US economy swerved the slowdown many anticipated. The labor market has stayed tight and manufacturing activity continues to expand. The resulting persistence in inflation has led Fed Chair Jerome Powell and fellow policymakers to wait longer than expected to cut rates.

New York Fed President John Williams has even suggested the possibility of resuming rate hikes if warranted.

“At the beginning of the year I was more of a dollar bear, but that’s no longer the case,” said Rajeev De Mello, global macro portfolio manager at Gama Asset Management SA. “Powell’s comments definitely changed things.”

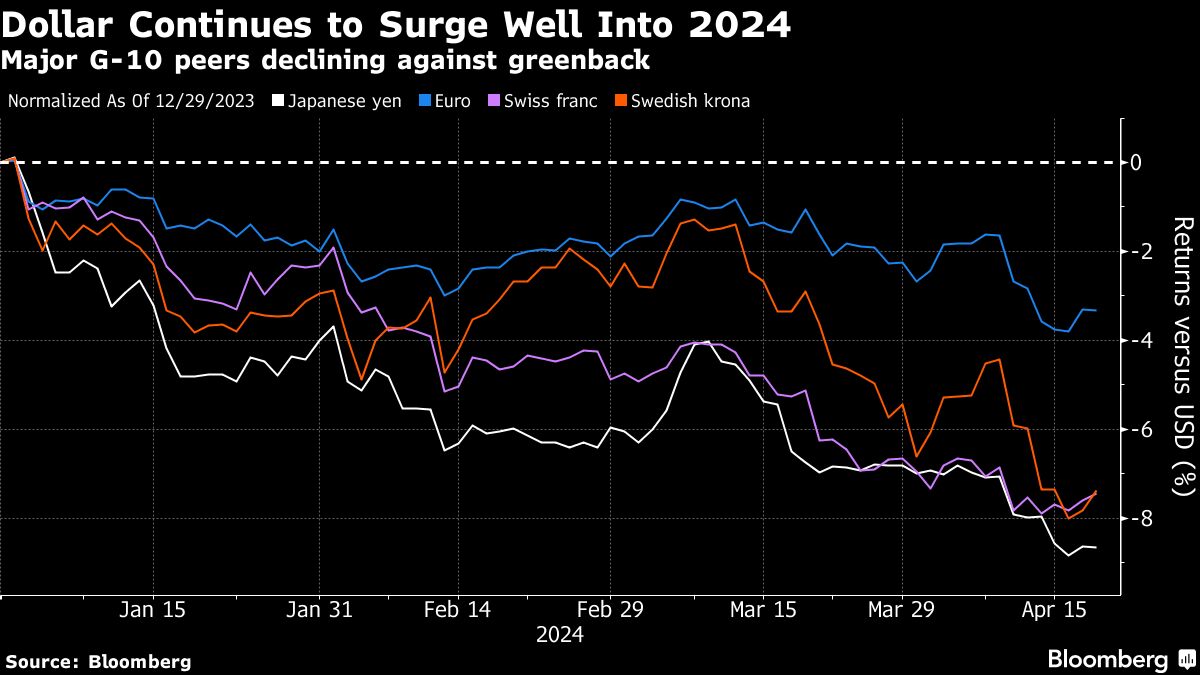

Of course, the surge in the world’s reserve currency inflicts a price on its counterparts and their economies, which traders are also scrambling to address. India and Nigeria are among the countries seeing their exchange rates plumb record lows, while threats of intervention are being heard from Japan to Poland.

Central banks in developed markets such as Australia, the euro-area and UK may find their room for lowering rates limited if weaker exchange rates fan domestic inflation. Those countries burdened by foreign debt, including the Maldives and Bolivia, as well as those heavily reliant on American imports, may be among the most hurt.

In a sign of growing anxiety caused by the greenback’s rapid ascent, the Group of Seven nations earlier this month reaffirmed their common stance over the potential damage of disorderly currency moves. It came after US Treasury Secretary Janet Yellen acknowledged the concerns of Japan and South Korea over sharp declines in their currencies, which may offer Tokyo and Seoul more scope to defend the yen and won.

On Monday, the Bloomberg dollar gauge headed for a third day of gains amid a calendar light on data and Fed commentary ahead of next week’s policy meeting.

High Yields

As markets scale back bets on Fed easing, Treasury yields have soared again in recent weeks, sending benchmark yields to near 5%. The surge has been a major driver of the dollar’s appeal, which has also benefited from ceaseless inflows into US stocks amid the frenzy for artificial intelligence.

“What’s unique now is that the dollar is such a high yielder,” said Peter Vassallo, portfolio manager at BNP Paribas Asset Management. “If you’re a global allocator and running your portfolio, what a slam dunk to improve your risk-adjusted returns: buy shorter-term US debt, unhedged.”

In contrast to reduced expectations for Fed easing, European Central Bank President Christine Lagarde has indicated policymakers may be in a position to lower rates in June. Meantime, Japan is so far behind the US in growth that even a historic decision to end the world’s last negative rates failed to prevent the yen from hitting a 34-year low.

“The interest environment in the US is just so much more attractive,” said Ed Al-Hussainy, global rates strategist at Columbia Threadneedle Investments. “The US dollar offers a very high rate of return.”

Haven Demand

Another tailwind for the dollar is its role as an unrivaled sanctuary for investors seeking refuge at times of political or financial turmoil. The currency’s haven status was on full display Friday, surging after Israel launched a retaliatory strike on Iran less than a week after Tehran’s rocket and drone barrage.

Helping to explain the dollar’s haven status is the widely-followed ‘dollar smile’ theory coined by Stephen Jen, chief executive of Eurizon SLJ Capital Ltd. Jen’s thesis is that the dollar rises when the US economy is either booming or in a deep slump, with weakness during periods of moderate growth.

Heightened geopolitical risks are working together with a booming economy to create “a curlier smile, with steeper tails,” creating more of a U-shape, Jen said in an interview. “For every level of US outperformance, the dollar should be stronger, because of that safe haven premium coming from geopolitical risk.”

US growth hasn’t decelerated so the dollar will stay on the “right side” of the smile for longer, he said.

At Morgan Stanley, that key side of the dollar smile, the strength of the US economy, has led currency strategists to go long the greenback against the euro and Chinese yuan.

“The growth cycle in the US has moved to a higher plane in light of strong immigration, productivity and investment,” James Lord and team wrote in a recent note. “The eurozone does not show a similar trend while the deterioration in China’s outlook is clear.”

What Bloomberg Strategists Say...

The underlying strength of the greenback will linger as long as US exceptionalism and stubborn inflation persists.

Mary Nicola, Markets Live strategist

“So long as the US economy is stronger than its G7 brethren, the dollar will be strong relative to other G7 currencies,” said University of California at Berkeley economist Barry Eichengreen. “ Not everyone may be happy with this, but there is little that can be done about it.”

The author of “Exorbitant Privilege: The Rise and Fall of the Dollar” doesn’t expect strength in the US currency to lead to confrontations, but does see growing debt servicing difficulties for developing countries with dollar-denominated debts.

But to some observers, including Clocktower Group’s Marko Papic, US currency strength may offer a “silver lining” for Europe, China and Japan. “It would help engender a global recovery given that most of the rest of the world is export oriented,” said the alternative asset manager’s chief strategist.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Read more articles by Ruth Carson, Naomi Tajitsu, Carter Johnson, Tania Chen

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All