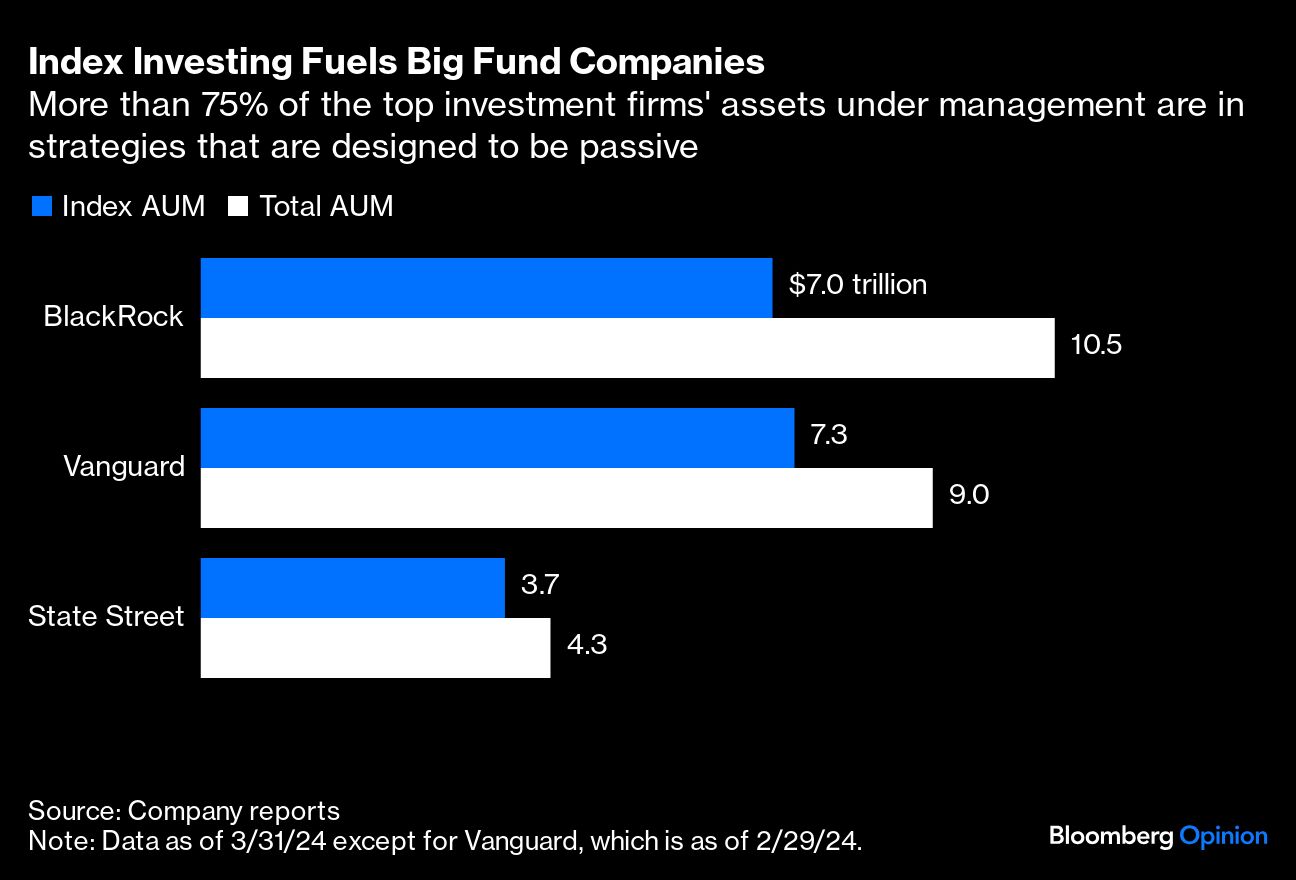

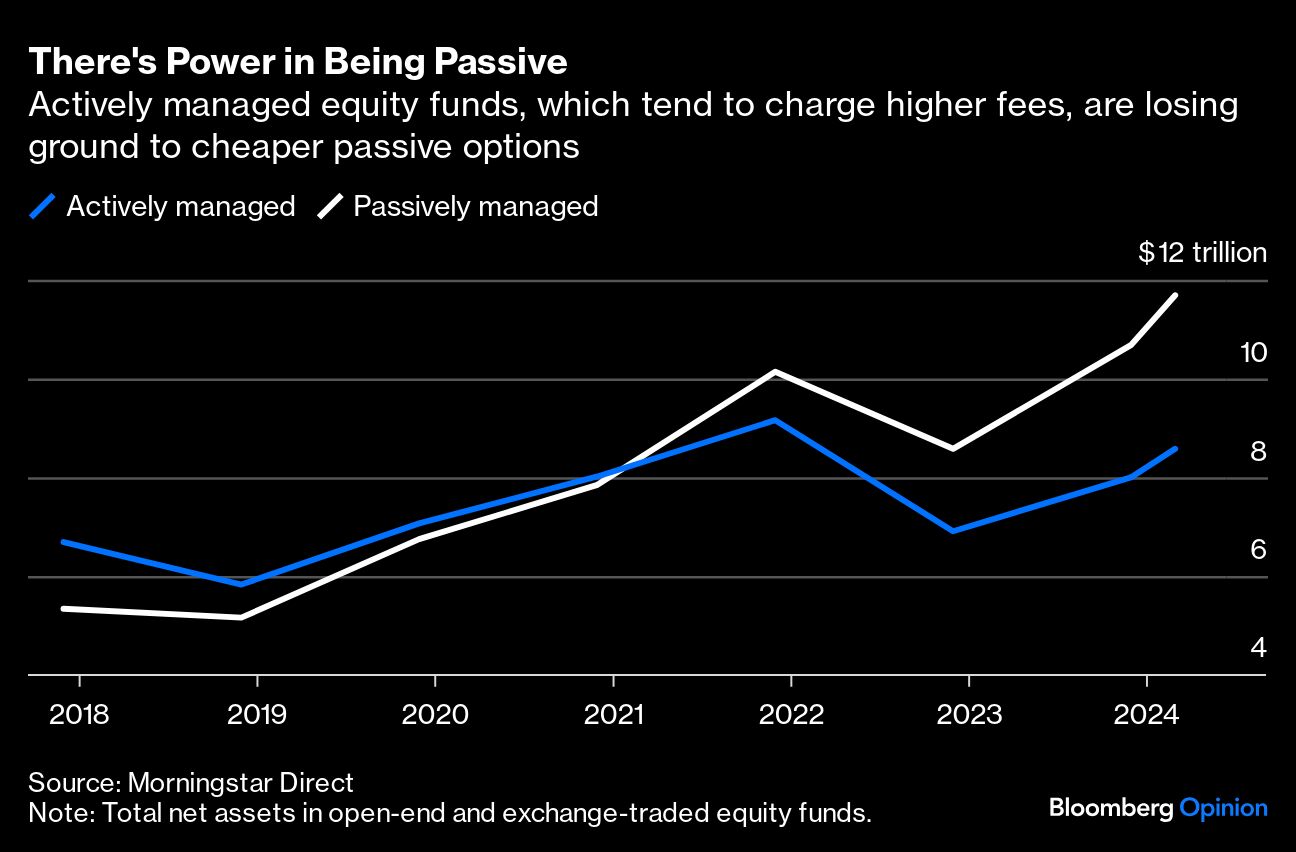

The rise of index funds has provided millions of Americans with a cheaper and more efficient way to invest. With more than $23 trillion in assets between them, BlackRock Inc., Vanguard Group Inc. and State Street Corp. have become the top shareholders in many US-listed companies.

That power has attracted critics ranging from Senator Bernie Sanders to the late Charlie Munger. Increasingly, the companies’ stakes in banks and energy utilities have gotten so big that they’ve triggered regulatory concerns. Policymakers now must tread a fine line: protect the immense value created by index funds while ensuring these companies aren’t abusing their power.

Regulators can impose onerous rules on any investor deemed to have significant influence or control over a utility or a bank. To avoid such oversight, funds have long received blanket authorizations from the Federal Energy Regulatory Commission and made passivity commitments to the Federal Reserve.

In recent years, however, suspicions have emerged that the “Big Three” firms might be meddling too much in the companies they own.

Criticism escalated after BlackRock Chief Executive Officer Larry Fink started advocating for more corporate involvement in fights over climate change, human rights and more. Republicans attacked the “woke” agenda, with some states blackballing BlackRock and others. Whatever one’s position on such issues, it became harder to see the companies’ “investment stewardship” teams as purely passive.

So far, congressional efforts to rein in index funds haven’t gotten very far. Bills proposed in the Senate and the House would each require funds to pass their voting powers to their underlying investors. Although the companies are piloting systems that give investors a choice in how to vote, participation is still low. Many Americans just don’t want to think that much about the S&P 500 fund in their retirement account.

Meanwhile, FERC is considering revising its policy on blanket authorizations. Board members of the Federal Deposit Insurance Corp. have also discussed the need for a more muscular approach to scrutinizing investors’ influence on banks.

For their part, the fund companies insist that they refrain from influencing or controlling the companies in which they own shares. But they continue to vote in corporate elections and to “engage” privately with boards and management, prompting questions about the role they’re playing on behalf of millions of Americans who are simply looking to hold a broad spectrum of stocks. Meanwhile, regulators disagree on what passive shareholders should be allowed to do.

Congress should strictly limit the role of any asset manager that’s claiming to act as a “passive” shareholder. Voting decisions should be devolved to end investors as much as possible; the rest should default to either supporting management or else be cast at the last minute as “mirror votes” that simply replicate the voting patterns of all other stockholders. Engagement with company leaders should be restricted to ensuring effective corporate governance and rigorously documented and disclosed.

Passive fund management provides an essential tool for retirement planning. It’s too valuable to lose to political squabbles. Congress can help protect it by ensuring funds follow an investing rule of thumb: Sometimes it’s best to leave well enough alone.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by The Editors