High-Tech Trading Firms Race to Grab Bond Market Turf

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThey subdued stocks, claimed a chunk of foreign exchange and muscled into the commodity market. Now high-tech trading firms like Citadel Securities LLC and Jane Street are pushing deeper than ever into fixed income.

Riding a wave of digitization and a boom in ETFs, electronic market makers — who keep securities moving by continuously buying and selling in lightning-fast transactions — are expanding their reach in government bond trading and finally gaining ground in the once-untouchable world of corporate debt.

In the process they’re storming territory ruled by Wall Street’s biggest banks, throwing everything from client relationships to transaction costs into flux and scooping up staff alongside market share — even as the march of so-called electronification stirs concerns about financial stability.

At Jane Street, a $1.4 billion bond sale in April gave a rare glimpse into the notoriously secretive business. Documents for the debt, the proceeds of which will go toward further expansion, show the firm has earmarked fixed income and in particular government bonds as “particularly high growth” areas. It has also been rapidly climbing the league table of market makers in credit, helped by its dominance in the ETF business.

Citadel Securities says the number of institutional clients using its fixed-income services has jumped more than 15% since it started making markets in investment grade corporate bonds last year. Already one of the top dealers for Treasuries, the sibling to Ken Griffin’s hedge fund will soon launch into European and UK government debt. It also plans to begin portfolio trading — a red-hot technique for moving big baskets of securities in one swoop — before entering high-yield credit.

“It’s part of the evolution that frankly started many decades ago in equities and soon after that in FX,” said Av Bhavsar, the global head of fixed income and cross-asset distribution at Citadel Securities. “Given the advancement of technology in fixed-income markets, it seems like a pretty natural thing that you will have new participants in the delivery of these products.”

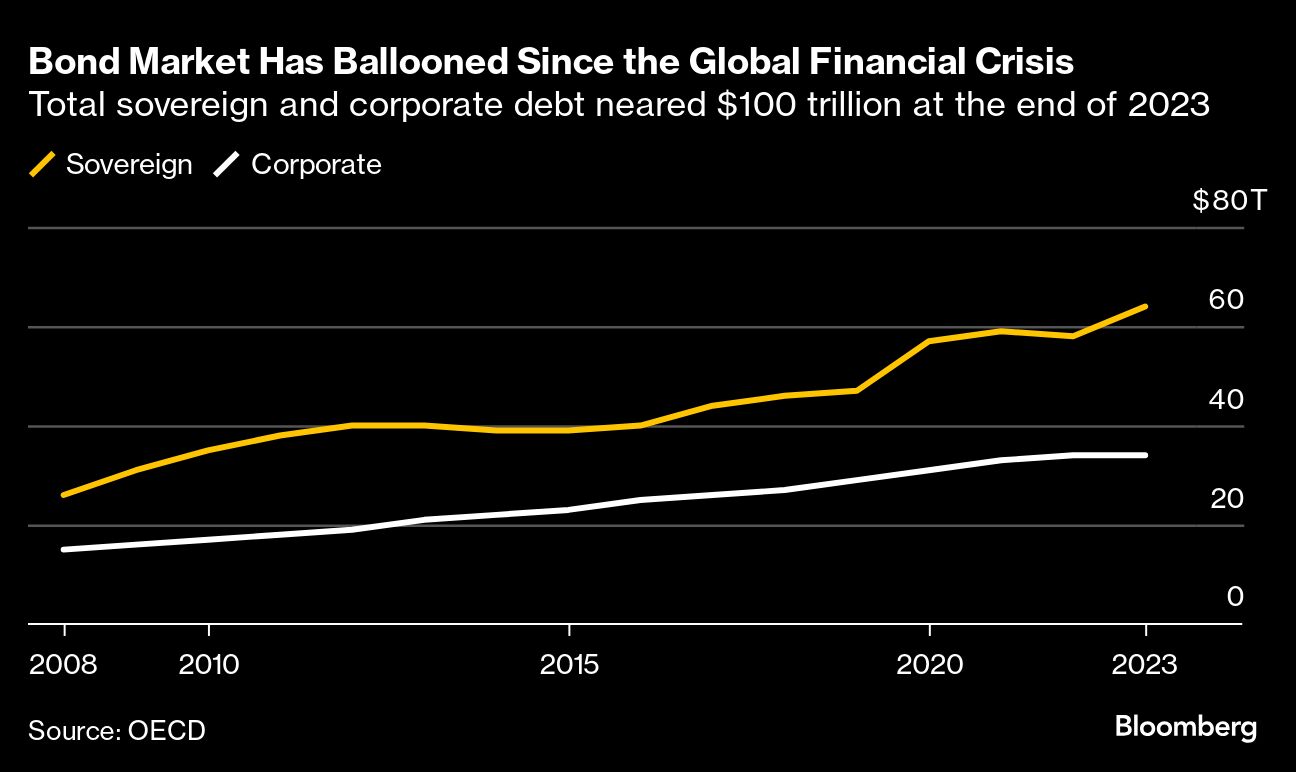

Alongside the likes of Flow Traders Ltd., Virtu Financial Inc. and Millennium Advisors LLC, these players are powering a shift in the very structure of the global fixed-income arena, which has ballooned to become a $100 trillion market.

Electronic Evolution

With a market far more complicated than that of equities, no centralized exchanges and huge pockets of illiquidity, trading bonds of all stripes has long been a highly profitable affair largely conducted between banks and their clients via phone or message.

But under pressure from buy-side firms looking for cheaper, faster execution, and as tighter regulation curtailed bank activity, trading platforms at the heart of the business began digitizing and opening up to new liquidity providers. Traders working from home during Covid lockdowns lent momentum to this electronic shift.

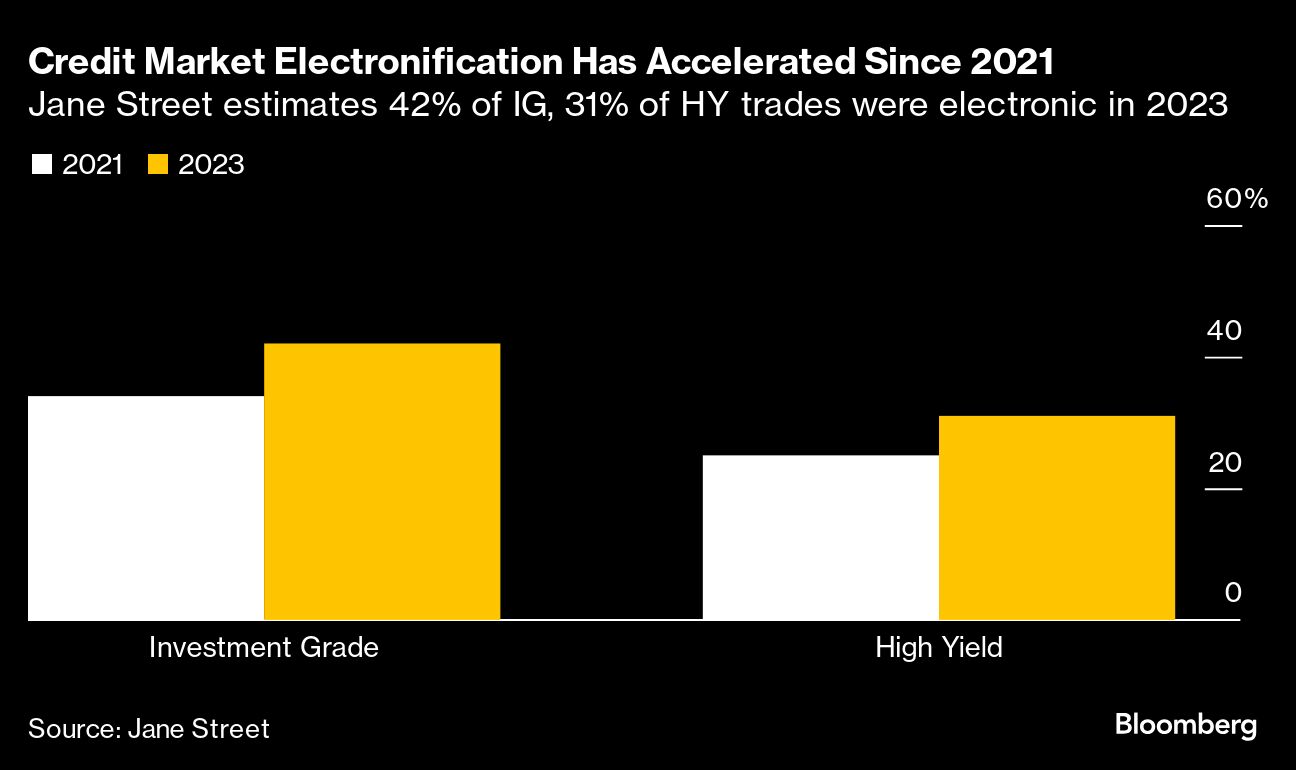

Jane Street estimates in its debt document that the percentage of investment-grade bonds traded electronically in the US jumped to 42% in 2023 from 34% two years earlier. In high-yield debt it was 31%, up from 25%. Coalition Greenwich says 64% of US Treasury trades were handled electronically in 2023, up from 45% before the pandemic struck.

Not all electronic trades are handled by non-banks, or alternative liquidity providers, and the fragmented market makes visibility difficult. But their speed and algorithmic expertise means they’re claiming a bigger and bigger share, as data from leading electronic-trading platforms show.

At MarketAxess, 35% of investment grade and high-yield credit trades last year were handled by non-traditional liquidity providers, up from 27% two years earlier. Tradeweb, which this week reported huge jumps in average trading activity for April from a year earlier, estimates that of the volume traded by the top 10 dealers on its platform in 2023, the share of fully electronic US credit handled by non-banks had roughly doubled in five years to around 10%. In government bonds it has jumped to nearly the same level from zero in 2019.

Data provided by Bloomberg's Electronic Trading Solutions business, which is part of Bloomberg LP, parent of Bloomberg News, shows 10% of the government bonds traded by its top 30 dealers is now by non-banks, while the cohort handles 11% of trades among the top 50 credit dealers.

Buyside Buy-In

Electronic market makers deploy cutting-edge technology to quote prices for high numbers of bonds and to execute trades at ultra-fast speeds and razor-thin spreads. While that drives down the profitability of every transaction, they make up for it with greater volumes.

The same tools also help them “internalize” more activity — fill orders from their own inventory — which can reduce a transaction’s discernible impact on the market. That’s a big draw to asset managers who want to offload or establish positions without creating a stir.

“There’s this narrative of us pushing into fixed-income markets, but there’s also a pull story from the client side,” said Bhavsar, who previously spent nearly three decades at Goldman Sachs Group, where he founded the cross asset sales desk.

After its entry into the investment grade corporate bond market last year, Citadel Securities is making rapid progress. Sam Berberian joined the firm to lead credit-trading in October following five years at Citigroup Inc., and since then the team has added around 35 people across sales, technology, quant research and operations.

At $67 billion Jupiter Asset Management, Mike Poole says the firm has been stepping up its use of non-bank liquidity over the last year after previously only ever trading with top tier investment banks. “Consistency and having confidence that you can get something done at that level, while minimizing leakage” are the big draws, the head of trading said.

That chimes with what other asset managers say. Legal & General Investment Management Ltd. sees alternative liquidity providers becoming increasingly relevant for risk-transfer activities. Swiss money manager Syz Group said it’s routing double the amount of fixed-income trades through alternative liquidity providers compared to three years ago.

“Quantitative algorithms enable them to have a comprehensive and detailed view of the market at any time,” said Valerie Noel, head of trading at $26 billion Syz. That’s an “invaluable strength for accurately pricing a wide range of worldwide bonds,” she said.

ETF Boom

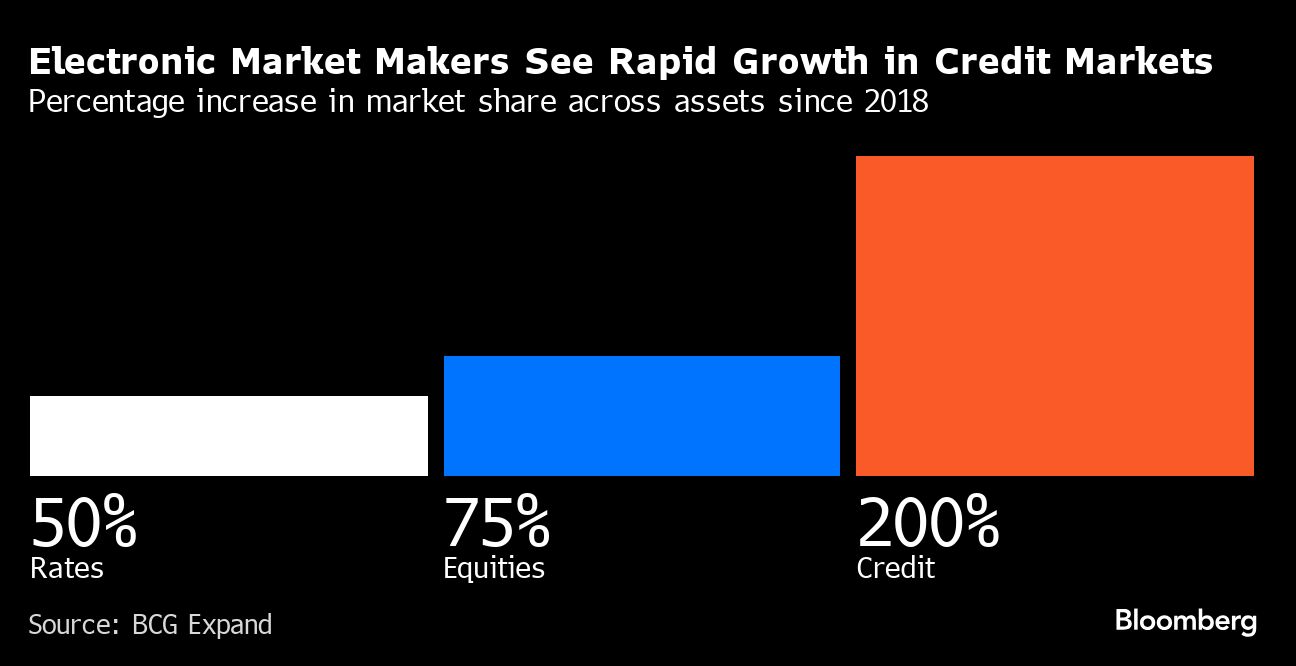

Expand Research, a Boston Consulting Group company, estimates that non-bank market makers have grown their share of government bond trading by more than 50% since 2018 and increased their slice of credit activity by over 200%. A surge in the use of fixed-income ETFs, where electronic market makers are key players behind the scenes, has been key to that trend.

Jane Street accounted for 41% of all primary market activity in US fixed-income ETFs last year, the firm said in its debt document. That “has helped us expand our bond inventory, which in turn allows us to provide meaningful liquidity in the underlying market,” it wrote.

“We’ve built a lot of techniques and technology, devoted resources to scale the business,” said Matthew Berger, Jane Street’s head of fixed income. MarketAxess data show it’s among the top 10 dealers for both volume and count of investment-grade bond trades in 2024 so far, while in high-yield transactions it’s in the top three.

Virtu, another well-established ETF market maker, is also in the top 10 for investment-grade trades at MarketAxess. Having launched its corporate credit operation in 2022, it now executes more than 1,000 trades a day on the major electronic platforms. Year-to-date activity is currently about double a year ago, the firm said.

“Our technology-driven approach allows our team to uniquely manage risk and connect flows across institutions, retail, portfolio trades, and ETFs in a way that is efficient, automated, and scalable,” said Phil Hartman, head of credit sales.

Critical Role

The electronic players don’t have it all their own way, since over half of credit trades and about a third of government bond transactions still take place over the phone.

Jane Street says it uses humans to provide “high-touch” services when clients require it. Citadel Securities launched a voice-trading option in February alongside its electronic offering, hoping for a bigger view of the trading landscape that will help make it more competitive overall.

The big Wall Street banks also retain a critical role in the issuance of new bonds and in the provision of research, even as post-crisis regulations designed to make the financial system safer have reduced their capacity as liquidity suppliers.

For many transactions, tech-powered challengers still depend on banks for help with services such as custody, clearing and settlement. That means new players are often among the top clients of a bank’s prime brokerage, even as they cause pain for its trading desk.

Alternative liquidity providers are “becoming much more relevant to institutional asset managers like ourselves,” said Ed Wicks, head of trading at LGIM. But “there’s a huge role for the investment banks and there always will be,” he said.

New Normal

The so-called “electronification” of fixed income is stirring concern in some quarters.

The International Capital Market Association said in March the move toward electronic trading and automation in fixed income is contributing to increased instability in the market. Its analysis of European sovereign bonds found “episodic heightened volatility, with rapid evaporation of liquidity, and a sharp repricing of risk” was accepted as the new normal by participants.

At the Healthy Markets Association, a trade group that includes pension funds and other asset managers, CEO Tyler Gellasch reckons the shift has given rise to more transparent, more efficient trading. But it has also brought in “the risks of who has got the balance sheet and how much the market is dependent on the intermediaries,” he said.

The worry is that liquidity providers with constrained balance sheets may pull back from markets in difficult conditions. Analysis of credit trading during the Covid-spurred selloff of 2020 showed evidence of both a decline in liquidity and a temporary switch to over-the-phone transactions at the height of the turmoil.

But the exact drivers of these patterns are not certain, and the debate is far from clear cut. As a general principle, more liquidity providers in the market should be a net positive, and some firms point out that when bid-ask spreads widen at times of stress, non-banks actually have more flexibility to deploy their balance sheets than their heavily regulated counterparts.

Meanwhile, the electronification of fixed income may have now passed an invisible threshold that gives it the breadth and depth to endure big shocks. In a December blog post, Iseult Conlin, Tradeweb’s head of US institutional credit, pointed out that electronic credit trading held strong during the banking turmoil of early 2023, suggesting “a newfound durability” that didn’t exist three years ago.

Regardless, Sally Bartunek, a New-York based fixed income trader at $160 billion Ninety One Asset Management, argues banks are likely to retain the lion’s share of the bond business simply because of their deep pockets.

“The alternative providers will show a price if they like it, but when we need balance sheets it’s the banks that will give it to us,” she said. “Our core liquidity providers remain the bulge-bracket banks by a long shot.”

Fighting Back

Trading is a lucrative business that banks won’t give up without a fight.

JPMorgan Chase & Co. has built out its electronic offering to US Treasury investors, while Citigroup formed a new algorithmic trading team within its rates division. At Bank of America, the lender has boosted capital spending and aggressively expanded its trading desks as it rises to the challenge of new high-speed players.

“Their tech/quant led approach is creating healthy competition in the marketplace which ultimately is better for our clients,” said Snigdha Singh, Bank of America Corp.’s co-head of EMEA FICC trading. “We’ve been investing heavily in our platform and product offering to remain competitive.”

Yet at Millennium Advisors, another of the electronic upstarts that also appears high in the MarketAxess league table for investment-grade corporate bond trades, Group CEO Laurent Paulhac reckons it can be tough for a traditional liquidity provider to keep up with firms like his.

Millennium currently trades fixed-income instruments with about 1,600 counterparties and, by focusing on smaller transactions that big banks might pass up, grew its trade count 29% in 2023 while volume jumped 75% from the prior year. But the firm is also constantly innovating, Paulhac said, such as creating new algorithms to make portfolio and other popular forms of trading faster and more efficient. He argues Millennium’s small size allows it to push through changes much faster than the old guard.

“Banks aren’t able to do that,” said Paulhac. “It’s hard when you have 20,000 employees instead of 100.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All