The big news in the $20 trillion US property market last week was that, for the first time since the financial crisis, investors suffered losses on top-rated bonds backed by the mortgage on an office building. Don’t panic. Signs are emerging that we may be closer to the end than the beginning of a shakeout in commercial real estate.

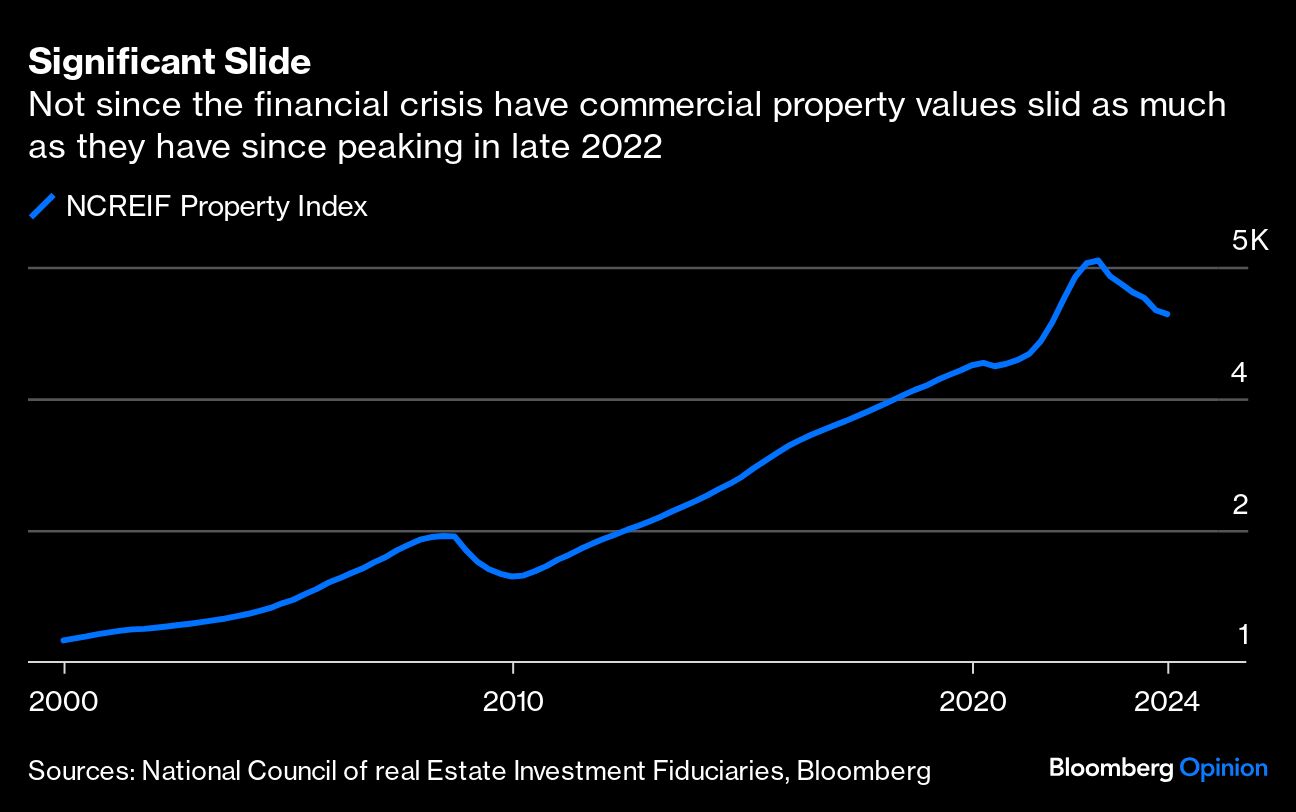

It’s been a tough couple of years. A widely followed index of commercial property prices, published by the National Council of Real Estate Fiduciaries, tumbled 12% from its peak in 2022 after the Federal Reserve began rapidly tightening monetary policy. Lending evaporated as higher borrowing costs wreaked havoc with the balance sheets of regional banks, the primary financiers of these properties. On top of that, the pandemic changed how we lived, worked and shopped, leading to higher vacancy rates for many landlords.

With the sector in disarray, transaction activity collapsed. Now, there’s evidence emerging that the market has bottomed. Upward revisions to recent monthly deal volumes reported by MSCI Real Assets are an encouraging sign, according to analysts at JPMorgan Chase & Co. The figure for March was revised higher from originally reported data by 9.5% to $25.8 billion, excluding “entity” transactions such as public company mergers and acquisitions. JPMorgan forecasts April’s numbers will be revised higher by 30% to $22.2 billion, representing less than a 1% decline from a year earlier. “We think that is a good place to start the second quarter,” the analysts wrote in a research report dated May 22.

Deals are following leasing activity, which is picking up. Even in the highly troubled office sector, property brokerage Jones Lang LaSalle Inc. reports that leasing volumes jumped 7% in the first quarter from a year earlier. “The year started with some positive momentum highlighted by an increase in bidders and the closing of several large deals in North America,” Jones Lang President and Chief Executive Officer Christian Ulbrich said during an earnings update earlier this month. “These green shoots encapsulate investors’ willingness to deploy capital when market conditions warrant,” he said, adding that “there has been a growing number of bidders across most sectors in early 2024.”

Blackstone Inc. is among firms allocating big money to commercial real estate on the belief that the bottom is in. “There’s bad news coming, but it’s the aftermath of the shipwreck that’s already happened,” Kathleen McCarthy Baldwin, its global co-head of real estate said at the Milken Institute Global Conference in Beverly Hills, California, this month. Goldman Sachs Group Inc., which has a long and storied history in the property market, just raised $3.6 billion for a fund that will provide real estate debt financing.

What about those losses in the AAA portion of a $308 million commercial mortgage-backed security tied to 1740 Broadway in midtown Manhattan? Isn’t that a sign that the worst is yet to come? Perhaps, but it’s worth noting that investors are coming back to these bonds, judging the yields offered adequately compensate them for the risks involved. This year through late April, investors scooped up $24.6 billion of CMBS offerings, 170% more than the same period of 2023, according to Bloomberg News, allowing the banking system to offload some of its real estate risk to investors.

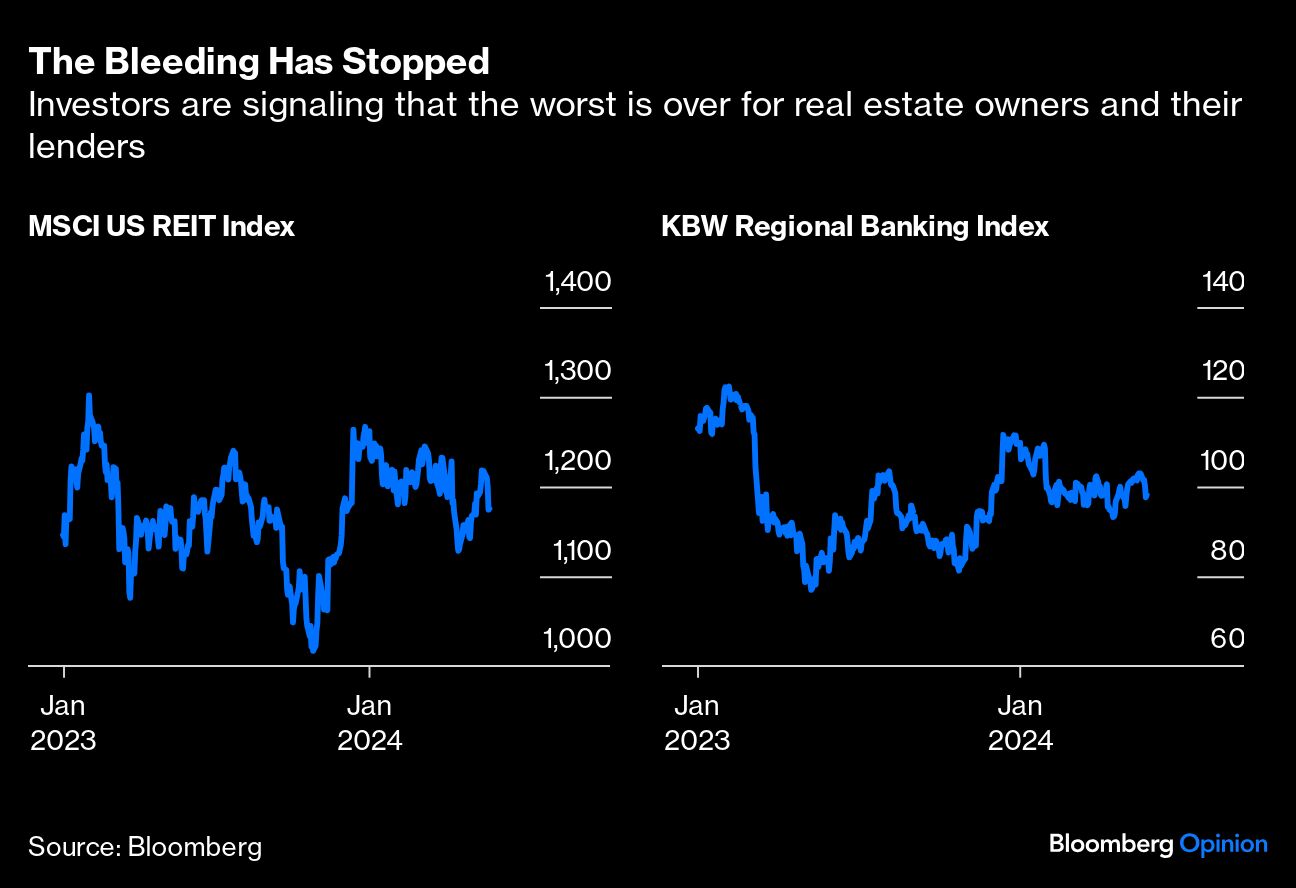

This is important because a healthy banking system is the bedrock of a healthy economy. Regional lenders, the biggest providers of financing for commercial real estate, have recouped about half their losses following the collapse of Silicon Valley Bank, Signature Bank and a few others early last year.

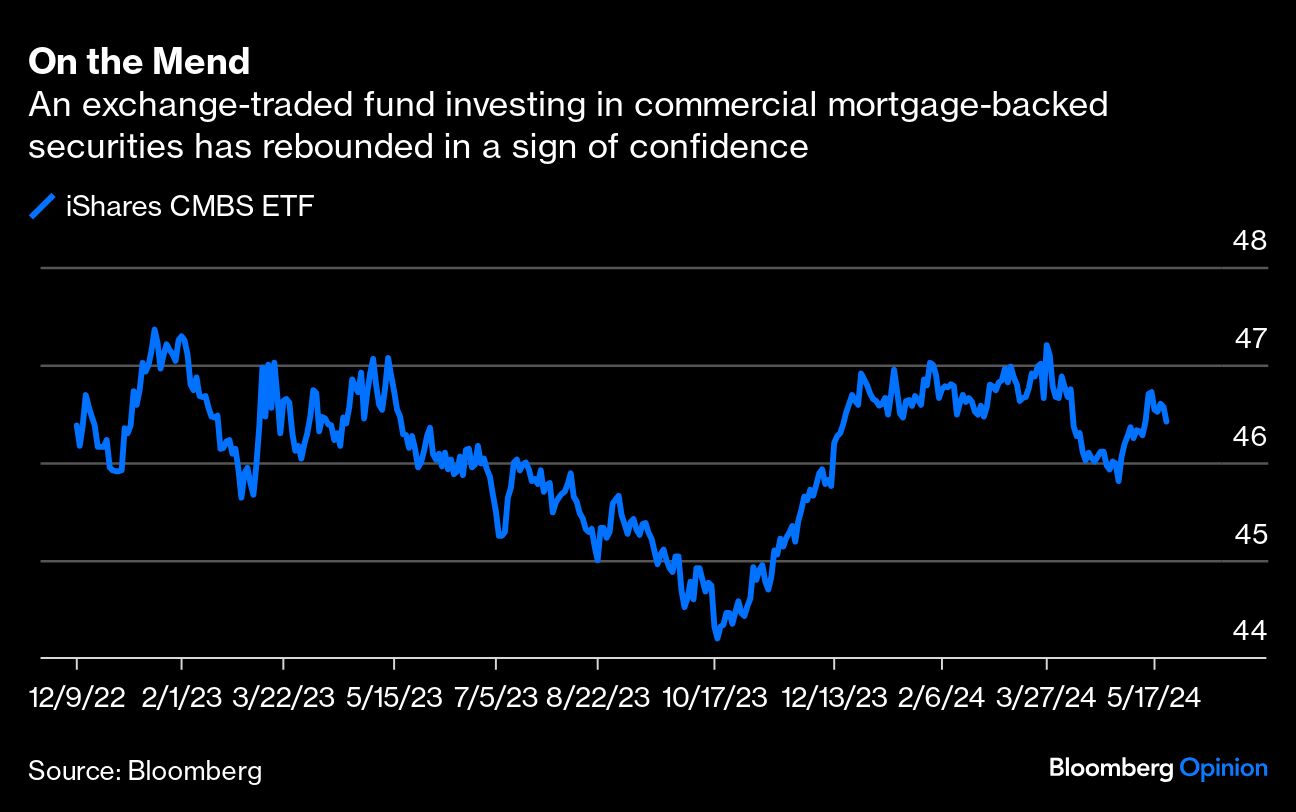

Growing confidence among investors that the worst is past has seen the iShares CMBS ETF climb 5.1% from its low last year on Oct. 18, and spreads on CMBS securities with BBB ratings shrink from the recent peak of 9.69 percentage points in early January to 7.27 percentage points. Another positive sign comes from the MSCI REIT Index that tracks the shares of publicly traded real estate investment trusts. It is also up from its lows last year in October, rising almost 16%.

No doubt some of the performance in CMBS, REITs and banks is tied to speculation the Fed may soon lower benchmark rates, offering relief to borrowers. And those gains could turn into losses if the central bank is unable to tame inflation and delays rate cuts. That would be problematic for borrowers that by the estimate of the Mortgage Bankers Association need to refinance some $929 billion of commercial and multifamily real estate loans this year.

The real estate market has been like a slow-moving train wreck, which is not necessarily a bad thing. Yes, the fallout has been extensive and continues to inflict pain as shown by 1740 Broadway. But most everyone has had time to change course to avoid as much of the wreck as possible. So while it may be too early to sound the all-clear, it’s probably not too early to say full-blown crisis averted.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Robert Burgess