Nvidia’s Wild Stock Swings Put AI Rally Stamina in Spotlight

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsBig swings in Nvidia Corp. shares have reignited debate about the staying power of the chipmaker’s rally. While the stock’s valuation and threat of competition are major concerns, one variable is key: durability of demand.

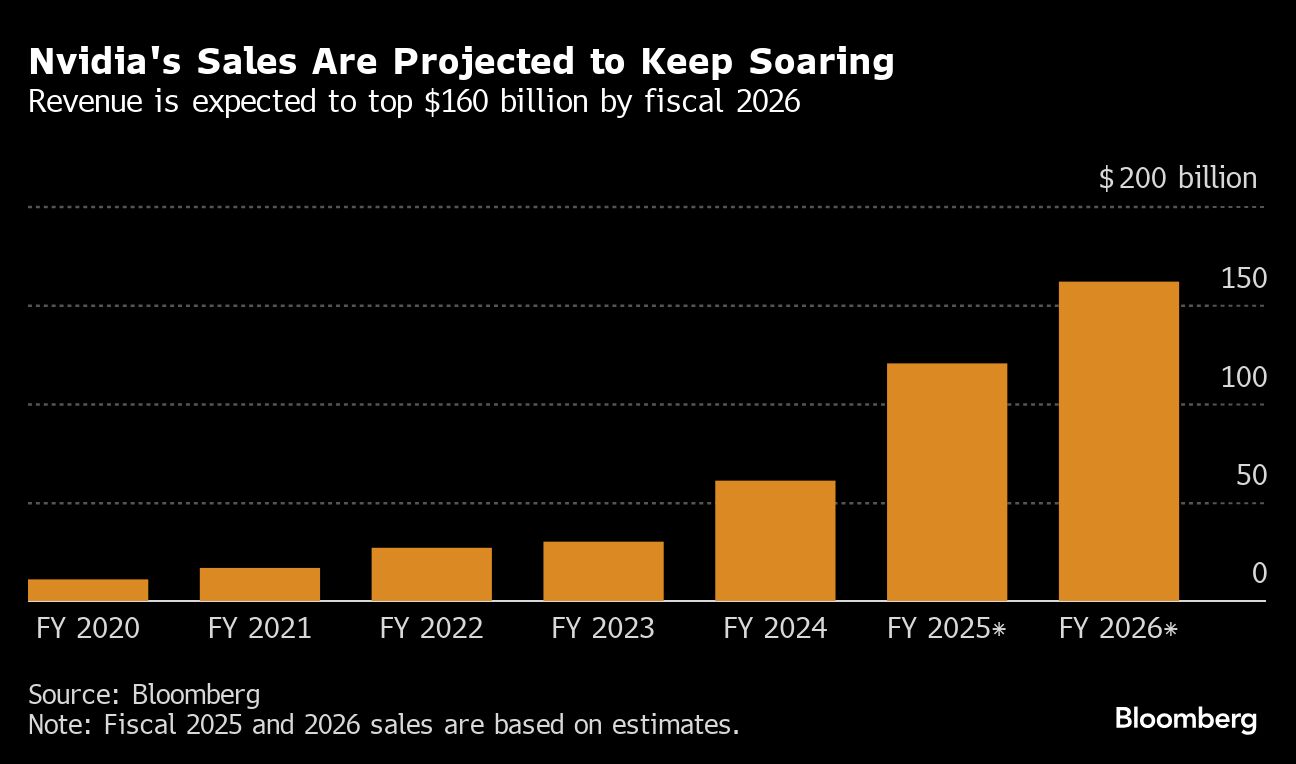

For more than a year, Nvidia’s customers have been snatching up all of the AI accelerator chips the company can produce. That fueled a doubling in Nvidia’s revenue in its last fiscal year to $61 billion and sales are projected to nearly double again in the current period.

To bullish investors, that spending is only just beginning as more companies seek ways to utilize artificial intelligence to help expand their businesses, create new products and improve efficiency. Nvidia’s resulting revenue and profit growth in that scenario would power the stock higher.

For bears, there’s still plenty of uncertainty about whether AI can live up to the hype and start delivering sufficient returns on investment. If not, demand is destined to cool and lead to a reckoning for Nvidia’s lofty valuation, which at 23 times projected sales is the most expensive in the S&P 500 Index.

It’s that scenario which Michael Kirkbride, partner and portfolio manager at Evercore Wealth Management, says is his biggest fear about Nvidia, even though he remains bullish on the stock.

“The longer term risk for all of this — and this is a multi-year risk — is that AI turns out to be a bust,” he said. “If AI turns out to be not the next internet and turns out to be the next telco, this will be a lot of ill money spent.”

Kirkbride is referring to the costly build-out of telecommunications networks in the 1990s in anticipation of a rapid internet traffic increase, which ultimately materialized at a much slower pace. Heavy spending and overly optimistic projections helped propel stocks like Cisco Systems Inc. to levels it still hasn’t surpassed more than two decades later.

Investors got a taste of what a reckoning for Nvidia shares might look like when the chipmaker, seemingly out of the blue, plunged 13% over the span of just three days, erasing $430 billion in market value. The shares snapped back on Tuesday and after edging higher again on Wednesday, have recouped about half their losses from the selloff. Nvidia shares fell in premarket trading Thursday after results from fellow chipmaker Micron Technology Inc.

Nvidia’s biggest customers — Microsoft Corp., Meta Platforms Inc., Amazon.com Inc., and Alphabet Inc. — have collectively plowed more than $150 billion into capital expenditures in the past four quarters. A big chunk of that is going to Nvidia, which dominates the market for chips that do the heavy lifting in AI computing.

Not only have those companies pledged to keep buying this year, many of them say they plan to spend even more.

For Steve Eisman, the Neuberger Berman senior portfolio manager who correctly bet against subprime mortgages before the 2008 financial crisis, that spending outlook gives Nvidia shares plenty of runway to keep rallying.

D.A. Davidson’s Gil Luria is less certain. One of the few analysts on Wall Street with a hold rating on Nvidia, Luria acknowledges that cloud services providers like Microsoft and Amazon are likely to remain “insatiable” for the next year or two but after that he sees more uncertainty.

“Those customers will have to deliver a very significant return on investment to justify more data center equipment and data center spending,” Luria said. “Until that happens the expectations for Nvidia for 2026 and beyond look very, very ambitious,” he added, noting that so far, their returns are paltry in comparison to spending.

John Belton, a portfolio manager at Gabelli Funds, acknowledges that insufficient return on investment from customers could become a problem for Nvidia down the road, but he sees no reason to bail on the stock now.

“We are cognizant of the long-term dynamics and we do monitor them, but we’re not going to sell a name with such strong fundamental momentum, where we think things are going to get even better in the near term.”

Tech Chart of the Day

Shares in Micron Technology Inc., the largest US maker of computer memory chips, declined in premarket trading after its forecast disappointed investors. Though Micron is getting a boost from the AI computing boom, demand is still sluggish in its traditional markets, such as personal computers and smartphones. Those areas are only beginning to recover from a historic slump last year.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All