Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

In a previous article, we described cashflow-matched bond strategies and showed how they can be an effective way to generate retirement income. We also showed that adding these strategies to a total return portfolio can help improve risk-adjusted returns, compared to relying solely on a total return portfolio. Perhaps counterintuitively, purposefully consuming principal during retirement can lead to better outcomes for retirees.

One question we heard a lot: What are some practical ‘real-life’ scenarios? For example, if a client needs $50,000 or $100,000 or $500,000 per year, how much might they need to invest in a cashflow-matched bond strategy?

Below, we introduce the Price of Certainty: How much do you need to invest to achieve a particular set of cashflows over time, with varying degrees of certainty?

Translating Assets Into Predictable Future Cashflows

Let’s look at the textbook retirement income problem: A 65-year-old is planning to age 95 and needs $40,000 per year growing at 2% per year. The traditional answer is the 4% rule: $1 million is required to meet that income objective, with some (undetermined) probability of running out or adjusting spending before the end of the 30 years.

This rule was originally devised in the 1990s so that a balanced portfolio could reliably sustain 30 years of inflation-adjusted spending, even in bad historical cases. Despite this stress testing, it still has a meaningful probability of failing to sustain full spending, depending on the capital-market assumptions used. What if there is another strategy that could both reduce risk and require less than $1 million?

Enter cashflow-matched bond strategies. In contrast to the 4% rule, these strategies look to match the cashflows that are contractually generated from bonds — coupons and principal at maturity — to the client’s desired cashflows. This means the client plans to draw down principal over time until the assets run out, according to a predefined schedule. For example, a 30-year solution would look to run out of money after 30 years, by design.

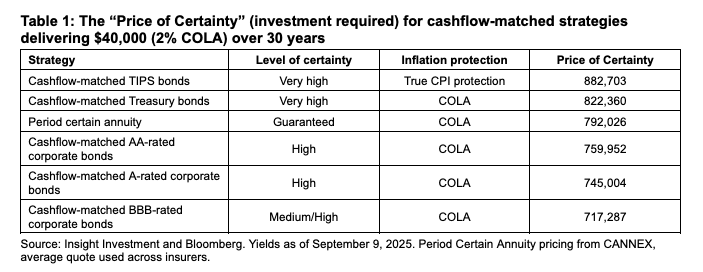

How much does this “cost” in terms of required investment? In other words, what is the “Price of Certainty” — the investment needed for a given desired cashflow? The answer depends on the type of investments used in the cashflow-matched strategy. We include different flavors of bonds, as well as an annuity, to reflect different levels of certainty and inflation protection (Table 1).

By investing around $822,000 in cashflow-matched Treasury bonds, an investor can receive $40,000 per year, with a 2% cost-of-living adjustment (COLA), until age 95 (see Table 1). If an investor is willing to invest in BBB-rated bonds and take some credit risk, the investor only needs around $717,000.

The average annuity, guaranteed by an insurer, is in the middle of the pack: It offers a guarantee, but at the cost of illiquidity, inflexibility and contractual complexity.

Comparing Cashflow-Matched Strategies to the 4% Rule

All the cashflow-matched strategies, as well as the annuity, have a lower Price of Certainty (meaning they require a smaller investment) than the $1 million investment required by the 4% rule.

One reason is that cashflow-matched strategies assume you want to completely exhaust the invested assets by age 95. In contrast, the 4% rule (and similar total return-based strategies) attempts to solve for two objectives with one portfolio: Both income during retirement and asset growth for longevity or legacy after age 95.

While the 4% rule and cashflow-matched strategies are not exactly like-for-like, we can still find a way to compare them to help decide which might be the more effective approach.

Suppose your 65-year-old client has $1 million and invests in the A-rated cashflow-matched strategy in Table 1. They would need around $745,000. The remaining $255,000 could be invested for legacy or longevity purposes. If it’s invested ultra-conservatively in a zero-coupon 30-year Treasury, the $255,000 grows to $1.1 million by age 95 (ignoring taxes). So, a “high certainty” strategy using $1 million means your client has high certainty of achieving the income they want and ending up with $1.1 million at age 95 for longevity or legacy purposes.

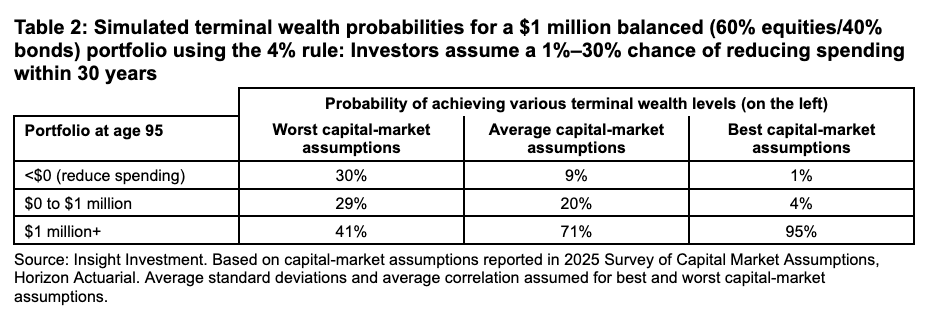

In contrast, the 4% rule would say that with $1 million, your client would have a ~70%–99% chance of being able to spend the full $40,000 with a 2% COLA per year, depending on how optimistic your capital-market assumptions are (see row 1 of Table 2).

The advantage of this strategy is that in many scenarios retirees end up with a lot more than the $1 million at age 95 (again, depending on which capital-market assumptions you trust). But your client would also have around a 1%–30% chance of “running out,” (i.e., being forced to spend less than the $40,000 with a 2% COLA per year before age 95), and potentially having little to nothing left for longevity and legacy purposes thereafter.

We believe that many retirees would opt for certainty and choose to rely less on notoriously fickle capital-market assumptions. In other words, we expect they would prefer a high degree of certainty of both spending the full $40,000, with a 2% COLA per year, as well as having $1.1 million at age 95 to cover longevity and legacy needs; all with similar liquidity to a total return portfolio.

Demonstrating the Resilience of Cashflow-Matched Strategies

As with all investments, cashflow-matched strategies come with some risk. But unlike traditional portfolios, volatility is not a good risk metric for these strategies, in our view, as the bonds are typically held to maturity. In the case of corporate bond cashflow-matched strategies, the biggest risk investors face is default risk: If the issuer of a bond defaults and does not make their contractual payments, then the strategy may fail to deliver the targeted cashflow.

To evaluate this risk, we can look at historical default rates using Moody’s data going back to 1970. Of course, if an active credit selection process can achieve lower defaults than historical defaults by selecting the “right” issuers (i.e., issuers that don’t default) and diversifying adequately, the risk of missed payments can be mitigated.

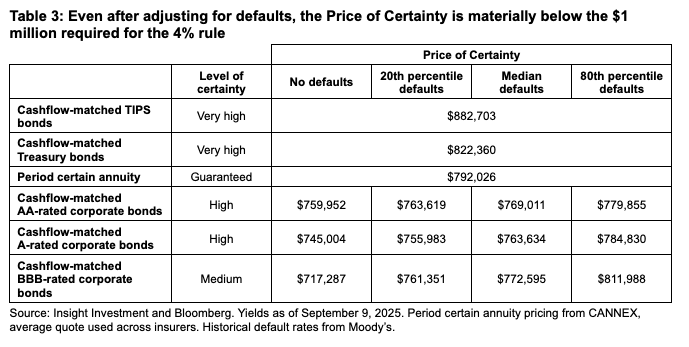

Table 3 illustrates the Price of Certainty adjusted for different default scenarios according to the percentile of historical defaults. For example, the 50th percentile (median) default scenario means that bonds in the portfolio experience the median default rate each year. In contrast, 80th percentile means bonds experience the 80th percentile default scenario every year.

While this is an unrealistic scenario because bond default rates drift randomly over time and do not follow any specific path, it is nonetheless instructive to see what an exaggerated best/worst conceivable historical case yields for the illustrative cashflow-matched strategies we have been considering.

To account for defaults, we increase the Price of Certainty based on the default scenario. For example, if a particular default scenario has 5% losses from defaults over 20 years, then we increase the Price of Certainty to compensate for these losses.

Our results show that even with significant default assumptions (80th percentile defaults every year), corporate bond cashflow-matched solutions are attractive relative to annuities and Treasuries. The implication is that investors appear to be more than well-compensated for assuming investment-grade corporate default risks. Even with these default assumptions, cashflow-matched strategies require far less than the $1 million required under the 4% rule, leaving space for separate longevity or legacy portfolios.

Cashflow-Matched Strategies May Be a Good Fit for Many Retirees

We believe cashflow-matched strategies could represent an appealing addition or alternative to the 4% rule for clients requiring income in retirement. Particularly in this yield environment, cashflow-matched strategies appear to be able to deliver income with high levels of certainty at lower costs than the 4% rule — leaving significant room for longevity/legacy objectives.

Operationally, cashflow-matched strategies can also be easy to maintain since advisors do not need to rebalance portfolios for income. Cashflow-matching allows advisors to deliver an annuity-like solution, without the guarantee, but also without the headaches, inflexibility, and costs that can come with annuities. This approach can be a win-win solution for both clients and advisors.

Massimo Young, CFA, is head of Personal Bond at Insight Investment. He can be reached at [email protected]. Ing-Chea Ang is a senior quantitative analyst at Insight Investment. He can be reached at [email protected].

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Massimo Young, Ing-Chea Ang

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.