OUTLOOK

The final quarter of 2012 was the icing on the cake of an exceptional year for the credit sectors. Fourth quarter credit gains stemmed in part from uncommonly aggressive monetary policy responses in the third quarter. As economic growth continued to undershoot expectations, major central banks made clear that they were dissatisfied with the status quo of tepid economic growth and high unemployment. The Federal Reserve went so far as to tie its monetary policy to the level of the unemployment rate. Financial markets seemed encouraged that risky assets would ride the tailwind of unconventional central bank policies through 2013, at least. With markets appearing to discount aggressive policy easing for some time to come, assets across the credit spectrum enjoyed very good performance during the last three months of the year.

FIXED INCOME INVESTMENTS & THE GLOBAL THIRST FOR YIELD

From Treasurys to mortgages, investment grade and high yield credits, and emerging market debt, the low level of yields at once illustrates and reinforces the global thirst for yield. This thirst for yield has left many scratching their heads, pondering the hypothesis that unconventional monetary policies are, unequivocally, a recipe for runaway inflation. The only major inflation we have seen in recent years is bond price inflation.

We expect the global thirst for yield to persist in 2013; however, investors were treated to some outstanding bond returns in 2012 that are unlikely to repeat in 2013. The math of fixed income returns becomes more difficult with a steady decline in yields. Instead of high-single-digit returns on investment grade corporate bonds and even double-digit returns on high yield and emerging market bonds, investors need to adjust their expectations lower. Bonds can still generate positive returns, but going forward, a fixed income investor’s return should be closer to the yield a bond offers when it is purchased and should not incorporate much in the way of price appreciation.

Still, we believe some fixed income sectors could produce mid-single-digit returns in 2013, including bank loans, convertible bonds, high yield and RMBS. We continue to like the investment grade credit markets in the US and Europe but think emerging market companies that issue debt denominated in dollars and euros should perform better. Currently, there is not a lot of value in high-quality sovereign bonds such as Treasurys, bunds or gilts—unless a major economic downturn or financial accident develops; however, an event like this is not part of Loomis Sayles’ base-case outlook for 2013.

Selected sovereign bonds from Mexico, Italy, Poland, Turkey, Malaysia, Thailand and the Philippines could produce returns competitive with corporate credit risk in 2013. The drive lower in investment grade and high yield corporate bond yields should prompt investors to scour the globe for alternatives, and local currency emerging market bonds should continue to see flows. We suggest investors do their currency research, as there were some high-profile emerging currency flops in 2012: Brazil, South Africa and Indonesia.

AN END TO THE BOND BULL MARKET?

When will this bond bull market end? In our view, not until global final demand rises to a self-sustaining level on the back of consumers and companies willing to borrow, spend, invest and hire. Unfortunately, at this point, we do not think 2013 will usher in that aggressive rise in demand. So, while we do expect lower returns in fixed income compared to 2012, we do not expect the much-feared bear market.

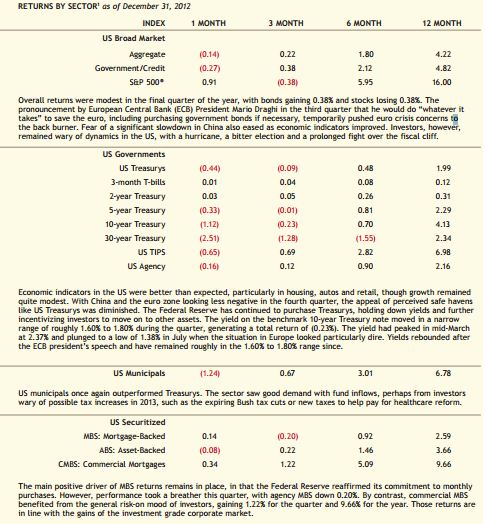

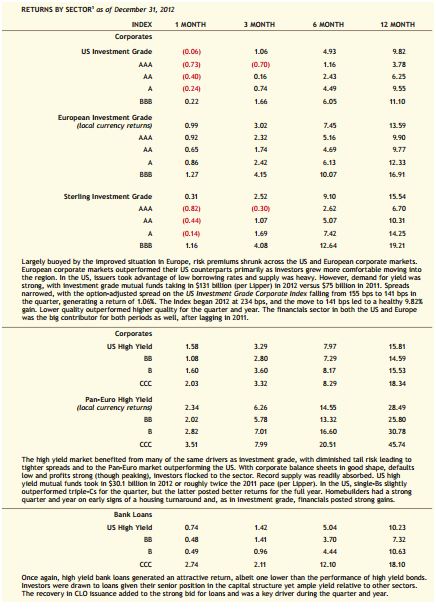

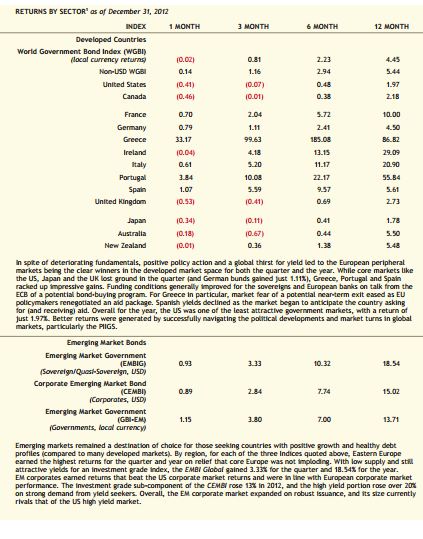

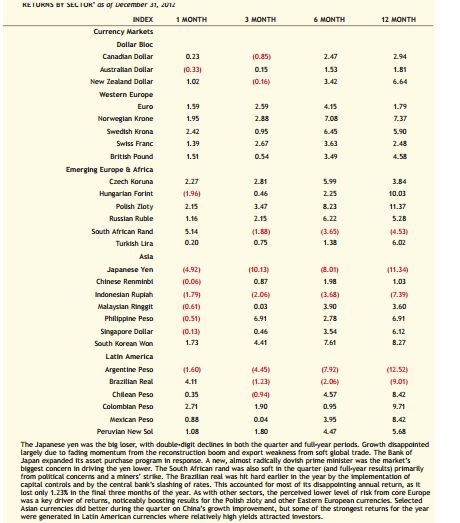

FOURTH QUARTER REVIEW

1All returns sourced from Barclays Indices except: World Government Bond (Citigroup), Emerging Market Bond (JPMorganChase), and S&P 500 (FactSet).

1 All returns sourced from Barclays Indices except: World Government Bond (Citigroup), Emerging Market Bond (JPMorganChase), and S&P 500 (FactSet)

Past performance is no guarantee of future results.

All indexes are unmanaged, do not incur fees, and you cannot invest directly in an index.

This commentary is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein

reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P., or any

portfolio manager. Investment recommendations may be inconsistent with these opinions. There can be no assurance that developments will transpire as forecasted

and actual results will be different. Data and analysis does not represent the actual or expected future performance of any investment product. We believe the

information, including that obtained from outside sources, to be correct, but we cannot guarantee its accuracy. The information is subject to change at any time

without notice.

INDEX DEFINITIONS

Barclays US Aggregate Bond Index is a broad-based benchmark that measures the investment grade, US-dollar-denominated, fixed-rate taxable bond market including Treasurys, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS, and CMBS.

Barclays US Government/Credit Index includes Treasurys (i.e., public obligations of the US Treasury that have remaining maturities of more than one year), government-related issues (i.e., agency, sovereign, supranational, and local authority debt), and corporates. Barclays US Treasury Index includes public obligations of the US Treasury with at least one year until final maturity, excluding certain special issues such as state and local government series bonds (SLGs), US Treasury TIPS and STRIPS.

Barclays US Agency Index includes agency securities that are publicly issued by US government agencies, quasi-federal corporations, and corporate or foreign debt guaranteed by the US government (such as USAID securities). Barclays US Municipal Index covers the US-dollar-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and prerefunded bonds.

Barclays US Securitized Index consists of the US MBS Index, the Erisa-eligible CMBS Index, and the fixed-rate ABS Index. The US MortgageBacked Securities (MBS) Index covers agency mortgage-backed pass-through securities (both fixed-rate and hybrid ARM) issued by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC). The US CMBS Investment Grade Index measures the market of conduit and fusion CMBS deals with a minimum current deal size of $300mn. The fixed-rate ABS Index includes securities backed by assets including credit and charge card, auto loan, home equity loan and stranded-cost utility.

Barclays US Corporate Index is a broad-based benchmark that measures the investment grade, fixed-rate, taxable, corporate bond market. It includes

US-dollar-denominated securities publicly issued by US and non-US industrial, utility, and financial issuers that meet specifi ed maturity, liquidity, and quality

requirements.

Barclays Euro Corporate Index tracks the fixed-rate, investment-grade euro-denominated corporate bond market. Inclusion is based on the currency of the issue, not the domicile of the issuer. The index includes publicly issued securities from industrial, utility, and financial companies that meet specified maturity, liquidity and quality requirements.

Barclays Sterling Aggregate Corporate Index is a broad-based benchmark that measures the investment grade, fi xed-rate, taxable, corporate sterling-denominated bond market. Inclusion is based on the currency of the issue, not the domicile of the issuer. The Index includes publically issued securities from industrial, utility, and financial companies that meet specified maturity, liquidity and quality requirements.

Barclays US Corporate High-Yield Index measures the market of US-dollar-denominated, non-investment grade, fixed-rate, taxable corporate bonds.

Securities are classified as high yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below, excluding emerging market debt. Barclays Pan-European High-Yield Index measures the market of non-investment grade, fixed-rate corporate bonds denominated in the following currencies: euro, Pounds sterling, Norwegian krone, Swedish krona, and Swiss franc. Securities are classifed as high yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below. Inclusion is based on the currency of issue, and not the domicile of the issuer.

Barclays US High Yield Loan Index tracks the market for dollar-denominated floating-rate leveraged loans. Instead of individual securities, the US High Yield Loan Index is composed of loan tranches that may contain multiple contracts at the borrower level.

Standard & Poor’s 500 (S&P 500®) Index is a market capitalization-weighted Index of 500 common stocks chosen for market size, liquidity, and industry group representation to measure broad US equity performance. Citigroup World Government Bond Index (WGBI) measures the market for the US and most developed nation government bond markets. The index is market capitalization weighted and has a minimum credit quality of A-/A3 by either S&P or Moody’s and a minimum maturity of one year. Included is fixed-rate sovereign debt denominated in the domestic currency. JPMorgan Emerging Markets Bond Index Global (EMBIG) measures the market for US-dollar-denominated Brady bonds, Eurobonds, and traded loans issued by sovereign and quasi-sovereign entities of qualifying emerging market countries.

JPMorgan Corporate Emerging Markets Bond Index (CEMBI) is a market capitalization weighted index consisting of US-dollar-denominated emerging market corporate bonds.

JPMorgan Government Bond Index-Emerging Markets (GBI-EM) tracks local currency bonds issued by emerging market governments.

MALR010021

© Loomis Sayles