PATIENT EQUITY INVESTORS WERE REWARDED WORLDWIDE IN 2012

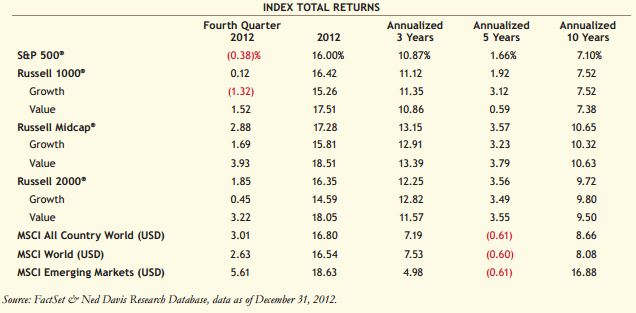

While the S&P 500 Index posted a slightly negative fourth-quarter return, the Index’s 16.0% return for all of 2012 was notable in the face of a long list of global fundamental concerns. Midcap and small cap stocks performed better during the fi nal three months of the year, posting gains of roughly 2.0%-3.0%. The fourth quarter outperformance of smaller stocks was enough to overtake the S&P 500 for the year, but just fractionally. In fact, US investors were rewarded for patience regardless of positioning across the market capitalization or style spectrums. Mid-teen gains were the rule across the board, as shown in the table below. Global indices also performed well for the year, particularly in the second half. The MSCI World Index returned 16.5% in 2012, surpassing the S&P 500 fractionally due to better fourth-quarter performance. Emerging market stocks, after lagging over the past three years, posted among the strongest returns in the quarter. For the year, emerging markets were up nearly 19.0%.

Global equity markets performed well in the second half of the year, following a negative second quarter, as illustrated by the MSCI Indices in the table below. At mid-year, investors held renewed fears over financial conditions within the euro zone. Signs of slowing in China coupled with concerns as to the vitality of the US expansion also weighed on stocks. Fortunately, equities bottomed out in the June–July time frame, and currency-related fears subsided as well. European Central Bank (ECB) President Mario Draghi’s now legendary speech of July 26, in which he convinced investors that the ECB had the necessary tools to defend the euro, proved to be a major turning point for global equity markets.

Though 2012 was a strong year, a longer-term examination reveals only a low-single-digit gain for the S&P 500 in 2011, and negative returns for most global equity markets that year. As such, the three-year annualized returns, while respectable for US stocks, have remained on the low side for global equities. Of course, the five-year returns are most unimpressive since the measurement period commences at the end of 2007, only a few months after the S&P 500 and Dow Jones Industrial Average last achieved record high prices. Ten-year results are much more respectable, especially considering that they include the impact of the 2008-2009 global financial crisis. Moreover, as evidenced by the Russell MidCap and the MSCI Emering Markets Indices, small and midcap US stocks, and emerging market equities have outperformed the S&P 500 over the past decade. While the returns posted over the past decade may not compare to the mid-teens or higher returns of the 1980s and 1990s, many long-term investors may consider these results respectable given the long list of global economic challenges and the current low inflation environment.

SECTOR PERFORMANCE

The financials sector led the S&P 500 and the MSCI All Country World (ACWI) Indices for the year. The near 30.0% gains in 2012 signaled that global economic conditions were improving, or at least stabilizing. The low interest rate policies being maintained by many central banks have lent critical support to the global economy. And US economic data has shown slow but steady growth on balance since the recession ended in 2009. Financial stocks, especially the largest capitalization financials, began the year at low absolute and historical valuations, a factor supporting 2012 performance. Improving sentiment with the euro zone, linked in part to ECB policy initiatives, was another major contributor. And while the S&P 500 suffered from profit-taking in the technology sector during the fourth quarter, the Index’s financials gained nearly 6.0%, and financials within the MSCI-ACWI gained nearly 9.0%. We believe that the finance sector can be a leading indicator of equity market returns; the leadership of financials in the second half of the year has seemingly extended beyond the sector itself and strengthened the overall investment environment.

Consumer discretionary was the second-best performing sector in both the S&P 500 and the MSCI-ACWI, during 2012. This eclectic sector drew considerable strength from the improvement in the US housing industry, as many markets have shed excess inventories and some regions are beginning to see home price increases. The consumer has been a beneficiary of central bank monetary easing. Many consumers have refinanced their debt, generally bringing down monthly debt service payments and leaving room for continued growth in retail sales. Gasoline prices have been reasonably stable recently, another boost to consumer confidence. In fact, commodity prices have been generally quiet in recent months, ironically a likely factor in the underperformance of energy and materials last year.

EARNINGS GROWTH IS MODERATING

S&P 500 operating earnings reached a record high in 2011, surpassing the previous high achieved in 2006. 2012 should see record earnings as well, and we are awaiting earnings reports for the final quarter of the year. While earnings have roughly doubled from the cyclical low reached in 2008, the current run rate slightly above $100 per S&P share is just a mid-single-digit percentage higher than 2011 levels.

Margin expansion from the recession lows has largely played out. And revenue growth has been sluggish as US growth has remained muted. Growth in China has decelerated, although there have been signs of stabilization recently. Europe has remained weak, with some parts of the continent in recession. As we look ahead to 2013, we generally expect more of the same: sluggish and spotty growth, continued easy monetary policy and an environment in which businesses will have to work hard to grow beyond mid-single-digit rates. While many companies should continue to generate double-digit earnings growth, that number is likely to be fewer than in recent years as the recovery matures.

WE SEE HIGHER STOCK PRICES AHEAD, BUT NOT WITHOUT CHALLENGES

While earnings growth has been moderating, equity valuation indicators continue to suggest that stocks are attractively valued relative to history. And the S&P 500 dividend yield, currently above 2% and growing, has remained attractive relative to many investment alternatives in our view. The equity risk premium has remained on the high side by historical standards, constraining the overall market multiple. However, we view relatively attractive valuations as an opportunity for investors to accumulate equity positions for the long term. While the cycle of large positive earnings revisions for the broad market has mostly played out, there are many companies with fundamental prospects well above that of the average company. Dividend growth has been a major positive for equities over the past couple of years, and we expect dividend growth in 2013 should exceed operating earnings growth. Corporate dividend payout ratios are still low by historical standards, and balance sheets have remained very strong on average. Including special dividends and accelerated payments, Standard & Poor’s estimates that dividends per S&P 500 share were $31.25 in 2012 compared to $26.43 in 2011. This yearly gain of 18.2% is the largest single-year gain in recent history. In our opinion, dividends are poised to reach the $33-$34 level, or higher, in 2013. Though the recent “fiscal cliff” compromise will result in higher tax rates on dividend income beginning in 2013, the rate is manageable in our view, especially considering the potential for companies to raise dividends in the future and the fact that many investors hold dividend-paying shares in tax-deferred accounts.

Where might the S&P 500 be valued in the next couple years? The range of potential outcomes is wide. We believe the equity investing environment is poised to remain constructive. Central banks have provided liquidity, we have slow but steady growth in the US, potential stabilization in Europe and signs of improvement in China. Our central case assumes no recession in 2013; hurdling the fiscal cliff in Washington takes one potential systemic risk off the table. Of course, federal debt ceiling negotiations lie immediately ahead for the US, and equity market volatility may accompany them. We cannot know how the debt ceiling debate will turn out, but we see this as yet another factor constraining equity valuations and providing potential opportunities at attractive prices.

The long-term average price earnings ratio of the S&P 500 has been about 15x operating earnings (although, it rarely trades at that level). Assuming our view of slow growth materializes, and events in Washington do not derail the economy, a P/E multiple of 15x with earnings above the $100 level and growing at mid-single-digit rates could potentially generate high-single-digit annual returns for the next couple of years, including dividends. Periodic equity selloffs could provide opportunities to judiciously add to favored positions. While we cannot make a strong case for P/E multiple expansion until economic growth accelerates, central banks and policy makers appear to be doing what they can to support economic fundamentals. As the preceding ten-year return table illustrates, holding for the long term can potentially conquer periodic stretches of weak performance.

Past performance is no guarantee of future results.

Indexes are unmanaged and do not incur fees. It is not possible to invest directly in an index. This commentary is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P., or any portfolio manager. Investment recommendations may be inconsistent with these opinions. There can be no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis do not represent the actual or expected future performance of any investment product. We believe the information, including that obtained from outside sources, to be correct, but we cannot guarantee its accuracy. The information is subject to change at any time without notice.

INDEX DEFINITIONS

Russell 1000®

Index measures the performance of the large cap segment of the US equity universe and includes approximately 1,000 of the largest securities based on a combination of their market cap and current index membership.

Russell 2000®

Index measures the performance of the small cap segment of the US equity universe and includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership.

Russell 1000®

Growth Index measures the performance of the large cap growth segment of the US equity universe and includes Russell 1000 companies with higher price-to-book ratios and forecasted growth values.

Russell 2000®

Growth Index measures the performance of the small cap growth segment of the US equity universe and includes those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values.

Russell 1000®

Value Index measures the performance of the large cap value segment of the US equity universe and includes those Russell 1000 companies with lower price-to-book ratios and lower forecasted growth values.

Russell 2000®

Value Index measures the performance of the small cap value segment of the US equity universe and includes those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values.

Russell Midcap®

Index measures the performance of the mid-cap segment of the US equity universe and is a subset of the Russell 1000 Index that includes approximately 800 of the smallest securities based on a combination of their market cap and current index membership.

Russell Midcap®

Growth Index measures the performance of the mid-cap growth segment of the US equity universe. It includes those Russell Midcap Index companies with higher price-to-book ratios and higher forecasted growth values.

Russell Midcap®

Value Index measures the performance of the of the mid-cap value segment of the US equity universe. It includes those Russell Midcap Index companies with lower price-to-book ratios and lower forecasted growth values.

Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group.

Standard & Poor’s (S&P 500® ) Index is a market capitalization-weighted Index of 500 common stocks chosen for market size, liquidity, and industry group representation to measure broad US equity performance.

S&P 500® is a registered service mark of McGraw-Hill Companies, Inc. MSCI World Index is an unmanaged index measuring global developed market equity performance.

MSCI Emerging Markets Index is a free float-adjusted market cap index measuring equity market performance of emerging markets. MSCI All Country World is a market cap weighted index of stocks from developed and emerging markets providing a broad measure of global equitymarket performance.

MALR010027

© Loomis Sayles