Slumping exports, lackluster domestic consumption, and slowing urban migration contribute to lower growth expectations for China.

January 2013

With Chinese manufacturing capacity now saturated relative to global demand, and developed economies facing the consequences of over-indebtedness, external tailwinds to China's growth have passed.

China has completed a remarkable transformation over the past three decades, rising to become a global power and the world's second largest economy. From 1981 to 2011, China's real GDP rose at an annual rate of 10.2%.1 This growth began from a low base and was not without hiccups. But in the last decade, the GDP had grown to such a scale that it began to have a profound impact on the rest of the world, particularly with respect to China's demand for materials.

Although China remains poor in terms of per capita income, its scale, demographic profile, and accumulated political and economic imbalances suggest future growth may not match the pace of previous decades. A growth slowdown would likely have its biggest impact on the economies of countries such as Australia, Brazil, Canada, and Indonesia that have large trade exposure to China and/or commodities. Of course, lower commodity prices could be a boon to the U.S., Europe, Japan, and much of the developing world.

Why China's growth has peaked

In 2000, the Chinese government recapitalized the country's faltering banking system and bolstered pro-growth economic policies. Improving political relations combined with the sheer scale of the country's low-cost manufacturing potential and abundant cheap labor opened the door to rapid export growth.

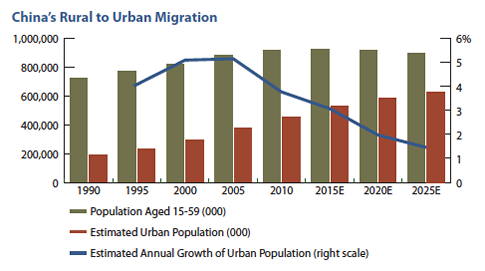

The human capital needed to support China's export boom and ancillary economic activity was provided by migration of younger rural workers to the southern and eastern port cities. In 2000, 36% of Chinese were classified as urban, a number that grew to 50% by 2010.2 Many workers remained migrants and lacked access to permanent urban housing. As the housing shortage accelerated, and the congestion of the major port cities capped any further benefit of increasing scale, the government responded by promoting the development of "2nd tier" cities. This phase of urban development accelerated sharply after the onset of the global financial crisis, with the unveiling of a massive stimulus plan to support economic growth in the face of slumping export demand. Much of this stimulus went toward public works — roads, rail, airports, and municipal infrastructure — while bank lending quotas fed real estate development.

We estimate the annual growth rate of the working-age urban population from 2001 to 2011 was 4.4%, but that it will slow to 2.5% annually in the coming decade. The lower rate of migration suggests China's economic growth should decline about 2%, assuming no change to the growth rate in productivity per worker. However, urban migration and worker productivity are closely linked because workers become much more productive when they move from a no-tech farm to a high-tech factory.

China's export boom accelerated after its 2001 acceptance into the World Trade Organization (WTO), with a large scale outsourced manufacturing transition that tapped its deep labor market. That transition is largely complete and may be reversing as Chinese labor costs have escalated. With Chinese manufacturing capacity now saturated relative to global demand, and developed economies facing the consequences of over-indebtedness, external tailwinds to China's growth have passed.

|

China's Inflation and Money Rates |

|||||||

|

2001-2011 |

|||||||

|

Annual inflation* |

4.25% |

||||||

|

Average deposit rate |

2.61% |

||||||

|

Average lending rate |

5.88% |

||||||

* Saturna's estimate of China's GDP deflator

Source: Bloomberg

China's growth over the last decade was also financed by high household savings rates and the negative real interest rates on bank deposits that financed cheap loans to state-owned enterprises. China's high savings rate has been a natural consequence of the low fertility rate caused by China's one-child policy and the lack of a social safety net in a Confucian society where working-age children are expected to support their older parents. When faced with the limit of only one child to meet that burden, urban families need to save a significant portion of their income instead of relying on offspring or nonexistent state pension systems.

Still, the absolute level of savings would not be so high were savers able to earn a real return on their deposits. But the central government has subsidized investment by holding deposit rates below the level of inflation. There have been few alternatives for most Chinese savers to protect the purchasing power of their savings other than simple bank deposits. The high savings rate provided ammunition for the central government to achieve its growth targets through quotas for lending by state-owned banks to other state-owned companies.

The high level of state-directed investment during the past decade caused capital investments as a share of Chinese GDP to rise from 35% to 46%. The household consumption share of GDP, however, plunged from 45% to 35%. Wages of Chinese workers grew slower than GDP, while inflation eroded the value of their savings, both of which limited the appetite for consumption.

Optimistic observers of Chinese growth point out that the accumulated stock of capital and infrastructure remains low compared to the developed world on a per capita basis. The biggest flaw with this perspective is that the extraordinary scale and pace of capital accumulation over the last decade eventually overwhelmed production of raw materials, driving their prices sharply higher. The multi-year timeframe of large scale investments and the momentum of investment spending is likely to have resulted in numerous projects that will not generate economic returns above their escalating costs. The specter of ghost cities such as Ordos in Inner Mongolia is a visual manifestation of this phenomenon, but the full scale is tricky to nail down. Economic intuition strongly counsels, however, that subsidized investment with rapidly escalating input costs will result in negative return projects, and a decreasing pool of attractive projects from which to choose.

China Growth Forecast: 2012-2022

China's economic fate in the coming years may resemble countries such as Korea and Japan that also experienced investment-led booms through a combination of high savings rates and repressed consumption. Their economies did not immediately rebound as their investment booms waned, and China, too, may find it difficult to maneuver to raise consumption growth. We suggest a baseline case for China's GDP growth over the coming decade could be 4-6%, which is at least 2-4% below consensus forecasts of economists. Slower economic growth combined with much slower growth in demand for materials via capital investment may pose trouble for countries and industries with large exposures to China's raw material demand.

Footnotes

1 Source: World Bank

2 Census shows China's population hits 1.339b. China Daily, April 28, 2011. http://www.chinadaily.com.cn/imqq/china/2011-04/28/content_12412491.htm

Copyright 2013 Saturna Capital Corporation and/or its affiliates. All rights reserved. Vol. 7 · No. 1

Saturna Capital publishes From The Yardarm Market Commentary & Analysis monthly. To subscribe, click here.

Saturna Capital does not share subscriber information with third parties.

Important Disclaimers and Disclosures

This report is intended only for the information of the reader, and is not to be used for or considered as an offer or the solicitation of an offer to sell or buy any securities or other financial instruments of any kind, including without limitation, any mutual fund or other product offered, sponsored, created, or managed by Saturna Capital Corporation or its subsidiaries or affiliates ("Saturna"). This report is not intended for distribution to, or use by, any person or entity who is a citizen or resident of, or located in, any locality, state, country, or other jurisdiction in which such distribution, publication, availability, or use would be contrary to law or regulation or which would subject Saturna to any registration or licensing requirement within such jurisdiction.

This document should not be considered as providing investment advice or services, or any service offered by Saturna. Saturna may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. Saturna will not treat recipients as its customers by virtue of their reading or receiving the report.

Nothing in this report constitutes investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to a particular investor's circumstances or otherwise constitutes a personal recommendation to any investor. Saturna does not offer advice on the tax consequences of any investment.

All material presented in this report, unless specifically indicated otherwise, is under copyright to Saturna. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of Saturna. Unless otherwise indicated, all trademarks, service marks and logos used in this report are trademarks or service marks of Saturna.

The information in this report was obtained from sources Saturna believes to be reliable and Saturna believes the information and opinions in the material are accurate and complete as of the date of this material. However, information and opinions contained herein will change over time and without notice. Saturna has no obligation to update or amend any information or opinions at any time. Saturna makes no representations as to the accuracy or completeness of this material, nor does it have any responsibility to ensure that any other materials, including any containing materially different information, are brought to the attention of any recipient of this report.

Under no circumstances shall Saturna, its employees, or any affiliate, be responsible for any investment decision by any recipient. This material is distributed on condition that it will not form the sole basis for any investment decision by any recipient. Any recipient who is not a market professional or institutional investor should seek the advice of an independent financial advisor prior to taking any investment based on this report or for any necessary explanation of its contents.

Saturna does not provide tax, legal or accounting advice. Investors should consult their own tax, legal and accounting advisers before engaging in any transaction. In compliance with IRS requirements, recipients are notified that any discussion of U.S. federal tax issues contained or referred to herein is not intended or written to be used for the purpose of (A) avoiding penalties that may be imposed under the Internal Revenue Code; nor (B) promoting, marketing or recommending to another party any transaction or matter discussed herein.

Past performance does not imply or guarantee future performance, and no representation or warranty, express or implied is made regarding future performance. The price, and value of, and income from, any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of foreign securities and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments. Investors in securities such as ADRs — the values of which are influenced by currency volatility — effectively assume this risk.

Please consider an investment's objectives, risks, charges, and expenses carefully before investing. To obtain this and other important information about the Amana, Sextant and Idaho funds in a current prospectus or summary prospectus, please visit www.saturna.com or call toll free 1-800/SATURNA. Please read the prospectus or summary prospectus carefully before investing.

The Amana, Sextant and Idaho Tax-Exempt Funds are distributed by Saturna Brokerage Services, member FINRA / SIPC. Saturna Brokerage Services is a wholly-owned subsidiary of Saturna Capital Corporation, adviser to the Amana, Sextant and Idaho Tax-Exempt Funds.

© Saturna Capital