Politicians crave the spotlight, but it is unfortunate that investors watch the show. 2012, like 2011, was another year in which Washington theatrics scared investors. As a result, investors largely missed out on above average equity returns. Corporate profits and valuations, and not Washington, continue to be the primary drivers of equity returns.We think there are several important points to consider when reviewing 2012 performance, and when structuring portfolios for 2013.

The US economy doesn’t stink. In fact, it is reasonably strong.

Politicians love to claim that the economy is performing poorly, and that we “have to get the economy rolling.”However, the latest GDP report of 3.1% over the past year is higher than the 30-year average of 2.9%.The US economy is actually growing faster than average!

Early-cycle sectors of the economy, such as housing and autos, have been showing marked improvement.Consumer confidence has significantly risen.Corporate profits have held up reasonably well despite a stronger US dollar and weakening non-US economies.Inflation remains very subdued.

Uncertainty is good!

Many have suggested that the “uncertainty” surrounding Washington and the fiscal cliff has deterred both financial and real investment within the US economy.This uncertainty, though, has tautologically translated into attractive equity valuations that, we feel, present investors with good opportunities.Has there ever been a time in US stock market history when investors were “certain” and equities were undervalued?We doubt it.

As we have previously pointed out, the S&P 500 is presently discounting 5-6% inflation for the next twelve months despite that inflation is currently less than 2%.This shows the level of fear among investors, but also shows to us the level of opportunity.

“Austerity” will not necessarily hurt the economy and the markets.

Many commentators have mentioned that the coming fiscal “austerity” will hurt the economy and the financial markets.We are not convinced because bull markets are not always based on the combination ofstimulative monetary and stimulativefiscal policy.For example, the 1982 bull market was based on very tight monetary policy (Chairman Volker aggressively tightened monetary policy to fight inflation) and verystimulativefiscal policy (the Reagan-era budget deficits which were, at the time, the largest peacetime budget deficits in history).

Fiscal austerity is bound to happen in some form over the next several years, but the Fed seems intent on keeping monetary policy loose.Without inflation and inflation expectations meaningfully accelerating, it is hard to see how the Fed would quickly reverse course.

Don’t ignore the US Industrial Renaissance

In the December issue ofThe Atlantic, JeffImmelt, GE’s CEO, is quoted as writing that outsourcing is “quickly becoming mostly outdated as a business model…” (See, Fishman, Charles. “TheInsourcing Boom”.The Atlantic.December 2012.)

We continue to believe that US manufacturing companies will gain market share as the decade progresses, and this remains one of our favorite investment themes.Closing wage differentials, lower energy costs, cheaper distribution costs, and political stability are all factors that companies are increasingly considering when locating new plant and equipment.

Washington’s theater is clouding, what we think is, one of the most interesting investment stories.We continue to favor small and mid-cap industrial and manufacturing companies.

We can’t emphasize enough that we view Washington as a sideshow (perhaps a very adequate analogy!), and that investors might be better served by focusing on fundamentals rather than politics.History shows well that corporate profits and valuations, and not Washington, ultimately drive equity returns.

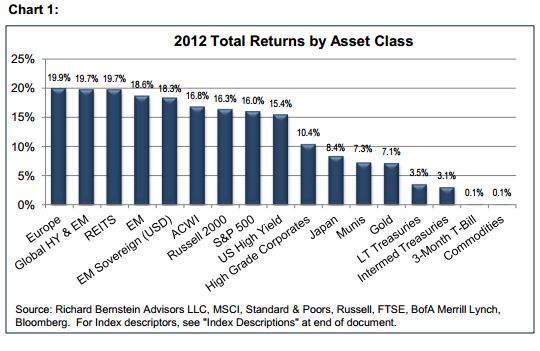

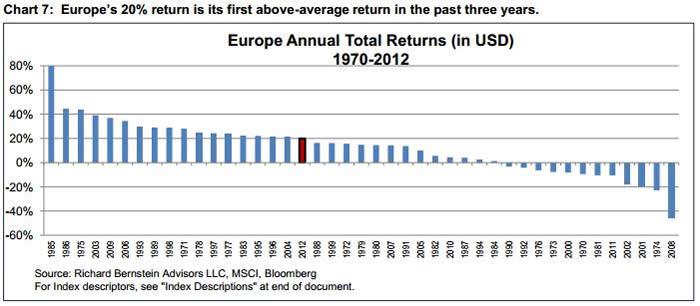

European stocks outperformed everything

Perhaps the biggest surprise at year end was that Europe’s stock performance outpaced that of other regions of the world. In fact, European stocks were the best performing major asset class.Corporate fundamentals continue to deteriorate in Europe, but it is probably worth watching those fundamentals closely for any improvement in 2013.

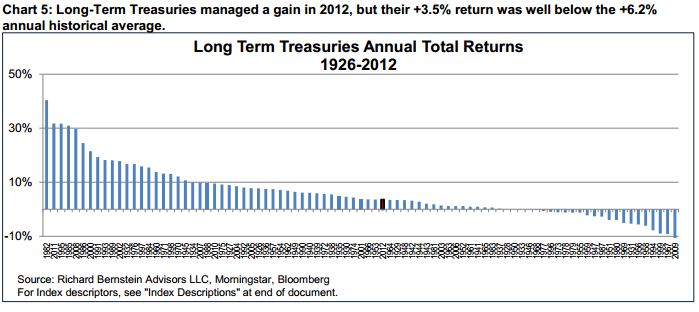

Bond Bubble?Not in Treasuries.

Many observers have claimed that there is a bubble in the bond market.We continue to disagree with such statements because:

The current bond market doesn’t seem to fit the historical characteristics of financial bubbles.Importantly, bubbles historically transcend society and are not simply financial market events.The bond market has not become a widespread societal event.

According to data from ISI, bond portfolios in aggregate have consistently had durations shorter than benchmark for the past seven years.If there were indeed a bond bubble, one would expect durations to be extraordinarily long.

Treasury returns are not abnormal.In Chart 5 in the appendix, 2012’s treasury bond returns were actually quite normal relative to history.

There do seem to be abnormally high flows into short-duration bond funds, but these funds generally do not focus on treasuries.

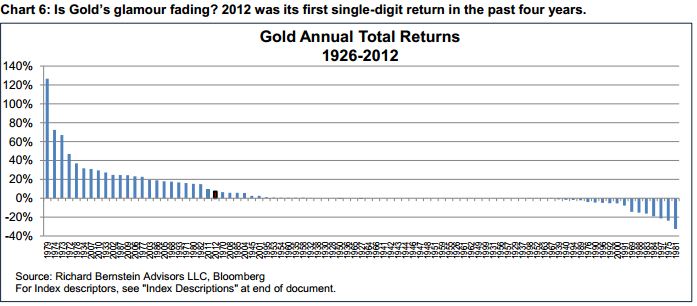

Munisoutperformed Gold – again!

We remain quite puzzled with US dollar-based investors’ enthusiasm for gold.Gold is expensive on a real basis, and came close to the all-time high in real prices set in 1980.The US dollar has been stable for almost five years, as the trough in the Dollar Index (DXY) was in April 2008.

More importantly, investors are ignoring the opportunity costs associated with investing in gold.The S&P 500 outperformed gold in 2012 and even municipal bonds have now outperformed gold in each of the past two years.

Appendix:

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends.An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results.Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500®Standard & Poor’s (S&P) 500®Index.The S&P 500®Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

US Large Company Stocks :The Morningstar “Ibbotson Large Company Stocks Index”is comprised of the S&P 500 returns fromMarch 1957 on.Prior to March 1957, the index is comprised ofthe returns of the S&P Composite index of 90 of the largest US stocks.

Russell 2000: Russell 2000 Index.The Russell 2000 Index is an unmanaged, market-capitalization-weighted index designed to measure the performance of the small-cap segment of the US equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index.

US Small Company Stocks :The Morningstar “Ibbotson Small Company Stocks Index” is comprised of the total returns of the DFA U.S. Micro Cap Portfolio net of fees and expenses from April 2001 thru current.From January 1982-March 2001, the index was represented by the DFA U.S. Small Company 9-10 Portfolio, from 1926 -1981, the index was represented by the NYSE Fifth Quintile Return series.This is comprised of the stocks making up the fifth quintile (9-10 decile) ranked bymarket capitalizationThe index is designed to represent the returns of a broad cross section of U.S. Small companies on a market-cap weighted basis.

Large Cap Growth:The Russell 1000 Growth Index.The Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell 1000 Growth Index is constructed to provide a comprehensive and unbiased barometer for the large-cap growth segment. The Index is completely reconstituted annually to ensure new and growing equities are included and that the represented companies continue to reflect growth characteristics.

Large Cap Value:The Russell 1000 Value Index.The Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 Index companies with lower price-to-book ratios and lower expected growth values.The Russell 1000 Value Index is constructed to provide a comprehensive and unbiased barometer for the large-cap value segment. The Index is completely reconstituted annually to ensure new and growing equities are included and that the represented companies continue to reflect value characteristics

MSCI ACWI®: MSCI All Country World Index (ACWI®).The MSCI ACWI®is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of global developed and emerging markets.

MSCI EM: MSCI Emerging Markets (EM) Index.The MSCI EM Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of emerging markets.

MSCI Europe: MSCI Europe Index.The MSCI Europe Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of developed European markets.

MSCI Japan: MSCI Japan Index.The MSCI Japan Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Japan.

Gold:Gold Spot USD/oz Bloomberg GOLDS Commodity.The Gold Spot price is quoted as US Dollars per Troy Ounce.

Commodities:S&P GSCI® Index.The S&P GSCI® seeks to provide investors with a reliable and publicly available benchmark for investment performance in the commodity markets, and is designed to be a “tradable” index. The index is calculated primarily on a world production-weighted basis and is comprised of the principal physical commodities that are the subject of active, liquid futures markets.

REITS:THE FTSE NAREIT Composite Index.The FTSE NAREIT Composite Index is a free-float-adjusted, market-capitalization-weighted index that includes all tax qualified REITs listed in the NYSE, AMEX, and NASDAQ National Market.

3-Mo T-Bills:BofA Merrill Lynch 3-Month US Treasury Bill Index.TheBofA Merrill Lynch 3-Month US Treasury Bill Index is comprised of a single issue purchased at the beginning of the month and held for a full month.The Index is rebalanced monthly and the issue selected is the outstanding Treasury Bill that matures closest to, but not beyond, three months from the rebalancing date.

Long-term Treasury Index:BofA Merrill Lynch 15+ Year US Treasury Index.TheBofAMerrill Lynch 15+ Year US Treasury Index is an unmanaged index comprised of US Treasury securities, other than inflation-protected securities and STRIPS, with at least $1 billion in outstanding face value and a remaining term to final maturity of at least 15 years.

Intermediate Treasuries (5-7 Yrs):TheBofAMerrill Lynch 5-7 Year US Treasury Index

TheBofA Merrill Lynch 5-7 Year US Treasury Index is a subset of TheBofA Merrill Lynch US Treasury Index (an unmanaged Indexwhich tracks the performance of US dollar denominated sovereign debt publicly issued by the US government in its domestic market).Qualifying securities must have at least one year remaining term to final maturity, a fixed coupon schedule and a minimum amount outstanding of $1 billion. including all securities with a remaining term to final maturity greater than or equal to 5 years and less than 7 years.

Municipals:BofA Merrill Lynch US Municipal Securities Index.TheBofA Merrill Lynch US Municipal Securities Index tracks the performance of USD-denominated, investment-grade rated, tax-exempt debt publicly issued by US states and territories (and their political subdivisions) in the US domestic market.Qualifying securities must have at least one year remaining term to final maturity, a fixed coupon schedule, and an investment-grade rating (based on an average of Moody’s, S&P and Fitch).Minimum size requirements vary based on the initial term to final maturity at the time of issuance.

High Grade Corporates:BofAMerrill Lynch 15+ Year AAA-AA US Corporate Index.TheBofA Merrill Lynch 15+ Year AAA-AA US Corporate Index is a subset of theBofA Merrill Lynch US Corporate Index (an unmanaged index comprised of USD-denominated, investment-grade, fixed-rate corporate debt securities publicly issued in the US domestic market with at least one year remaining term to final maturity and at least $250 million outstanding) including all securities with a remaining term to final maturity of at least15 years and rated AAA through AA3, inclusive.

U.S. High Yield:BofA Merrill Lynch US Cash Pay High Yield Index.TheBofA Merrill Lynch US Cash Pay High Yield Index tracks the performance of USD-denominated, below-investment-grade-rated corporate debt, currently in a coupon-paying period, that is publicly issued in the US domestic market.Qualifying securities must have a below-investment-grade rating (based on an average of Moody’s, S&P and Fitch) and an investment-grade-rated country of risk (based on an average of Moody’s, S&P and Fitch foreign currency long-term sovereign debt ratings), at least one year remaining term to final maturity, a fixed coupon schedule, and a minimum amount outstanding of $100 million.

EM Sovereign: The BofAMerrill Lynch US Dollar Emerging Markets Sovereign Plus Index

TheBofA Merrill Lynch US Dollar Emerging Markets Sovereign Plus Index tracks the performance of US dollar denominated emerging market and cross-over sovereign debt publicly issued in the eurobondor US domestic market. Qualifying countries must have a BBB1 or lower foreign currency long-term sovereign debt rating (based on an average of Moody’s, S&P and Fitch). Countries that are not rated, or that are rated “D” or “SD” by one or several rating agencies qualify for inclusion in the index but individual non-performing securities are removed. Qualifying securities must have at least one year remaining term to final maturity, a fixed or floating coupon and a minimum amount outstanding of $250 million. Local currency debt is excluded from the Index.

© Copyright 2013 Richard Bernstein Advisors LLC.All rights reserved.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in, any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Specifically, and without limiting the generality of the foregoing, before acquiring the shares of any mutual fund, it is your responsibility to read the fund’s prospectus. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is an inherently risky activity, and investors must always be prepared to potentially lose some or all of an investment's value.Past performance is, of course, no guarantee of future results.