Four Year Anniversary: It’s not the ’82 bull market, but it sure does look like it

Investors often remember bull markets as days of wine and roses.However, those fond memories are largely based on the latter stages of a bull market during which investors are convinced that there is indeed a bull market underway and that it will never end.They seem to forget that the majority of a bull market is typically characterized by fear and indecision.

Sentiment during the early and middle stages of a bull market is usually clouded by the bad experiences of the prior bear market.Investors are often hesitant to invest in equities for fear of another bear market.Yet, they see higher returns on stocks than the returns they are getting on their more defensive securities.The emotional tug-of-war between fear of another bear market and greed of missing out on higher returns tends to keep most investors sidelined for most of a bull market.

This cycle has certainly been no different.The S&P 500®has produced a total return of more than 140% since the market trough in March 2009, but many investors still do not even believe that a bull market is underway.Investors continue to search for 5% yields and seemingly ignore the much higher total returns that stocks have been producing.

Another 1980s bull market?

We have thought for some time that the current bull market might be one of the strongest of our careers, and could potentially rival the 1980s bull market.Although this current cycle’s construction is quite different from the 1980s bull market, there are many aspects of this market that are curiously similar.

Investors did not fully embrace the 1980s bull market until several years after it began.Institutional investors did not fully appreciate the opportunities in equities until late-1985/early-1986 when oil prices collapsed, and it became clear that inflation was not going to constrain equity returns.Individual investors largely stayed in money market funds and bonds until early-1987 when they were lured into the equity market by January 1987’s 13% one-month return.Individual investors then entered the stock market in droves just in time for the 1987 Crash.

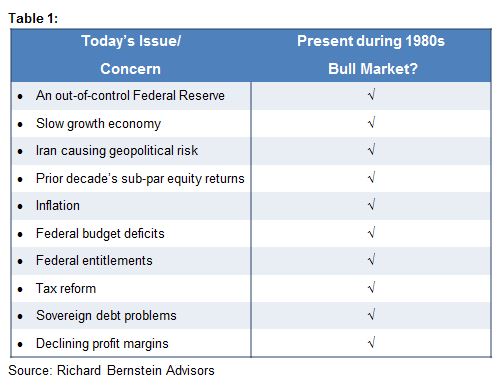

Similar to what is keeping investors on the sidelines during the current bull market, investors stayed out of the 1980s bull market for so long because there were many issues that investors thought were insurmountable.Table 1 highlights some of the issues that caused investors to forego for many years investing in the 1980s bull market.The irony is that they are largely the same as today’s concerns.

Of course, there are subtle differences between the 1980s concerns and today’s.In the 1980s, investors were worried that the Fed might tighten too much.Today, investors are concerned the Fed might ease too much.In the 1980s, it was Democrats who were concerned about budget deficits.Today, it is Republicans.The sovereign debt problems during the 1980s were largely associated with Latin America.Today, such concerns generally focus on Europe.In the 1980s, investors were concerned with Social Security bankrupting the nation.Today, it is Medicare and Medicaid.

Focusing on these differences, though, may miss the point.Investors were scared about a broad range of issues during the 1980s bull market, and the list of concerns is nearly identical to today’s list of concerns.Despite what many might suggest, the uncertainties associated with the current cycle are not unique.

What are the typical signals that a bear market is coming?

There are three classic signs that have historically strongly suggested that a bear market might be nearing.None of those three signs are evident today in the US.These signs are:

- The Fed tightens too much– historically bull markets didn’t end when the Fedstarted to tighten.Rather, they ended after the Fed tightened too much.Aclassic indicator that the Fed has tightened too much is an inverted yield curve(i.e., short-term rates higher than long-term rates).The Fed has indicated thatthey do not anticipate tightening anytime soon, and an inverted yield curveseems years away.

- Significant overvaluation– Our valuation models continue to suggest that themarket is significantly undervalued despite the four-year bull market.Moreimportant though is the high level of uncertainty among investors.Uncertainty,according to classic financial theory, indicates undervaluation.Markets tend tobe overvalued when investors are certain, and undervalued when investors areuncertain.In fact, this is a financial tautology.Most investors would agree thatthere is great uncertainty surrounding the US equity market.Therefore, the USmarket must be undervalued.

- Euphoria/Asset class of choice– It is hard to argue that US equities are theasset class of choice when Wall Street strategists are recommending a historically low equity allocation, pension funds have very low equity allocationsrelative to history, and US equity mutual funds were, until very recently,experiencing net outflows.

These signs are increasingly evident in the emerging markets and, as usual, investors don’t believe the signals apply.However, these signals do not appear within the US equity market.It is somewhat ironic that investors are enamored with the emerging markets despite that those markets are showing the typical signs of risk, but feel the US market is too risky even though the risk signals might be years away.

Bull markets are periods of fear and indecision

Bull markets are typically characterized by fear and indecision.This cycle has been no different from that historical norm.We think investors need to realize that this cycle’s concerns are not unique, and are similar to the fears during the 1980s bull market.In addition, the typical warning signs, although increasingly evident in the emerging markets, seem a long way away in the US.

Accordingly, our portfolios remain bullishly positioned.

© Copyright 2013 Richard Bernstein Advisors LLC. All rights reserved.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in, any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Specifically, and without limiting the generality of the foregoing, before acquiring the shares of any mutual fund, it is your responsibility to read the fund’s prospectus. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is an inherently risky activity, and investors must always be prepared to potentially lose some or all of an investment's value. Past performance is, of course, no guarantee of future results.

© Richard Bernstein Advisors