Short-Duration High-Yield Bonds: An Attractive Solution for a Low-Yield, Rising-Rate Environment

Learn more about this firmFinancial repression has caused historically low yields

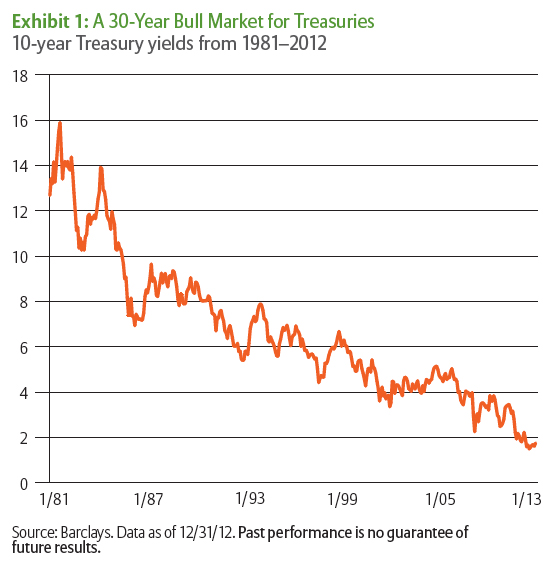

Treasuries have been enjoying a 30-year bull market since the early 1980s, as investors have responded favorably to an economic environment characterized by low inflation and by gross domestic product growth that has been persistently sluggish over the long term.

As Exhibit 1 shows, the long-term decline in the 10-year Treasury yield accelerated in 2008 with the Federal Reserve’s decision to engage in unconventional quantitative easing. The Fed’s actions have kept nominal interest rates lower than what would otherwise be expected, a phenomenon that is a key part of government policies known as “financial repression.”

Less yield when investors need it most

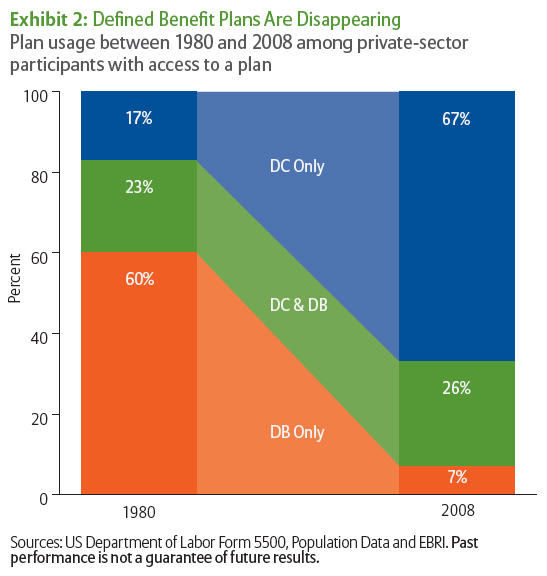

Unfortunately, this unprecedented decline in yields occurred at the same time as a significant and lasting shift to personal responsibility for retirement savings.

Given the well-publicized issues with Social Security and the decision by many companies to switch from defined benefit (DB) to defined contribution (DC) plans (see Exhibit 2), a greater number of employees and millions of baby boomers have been taking greater control of their own destinies.

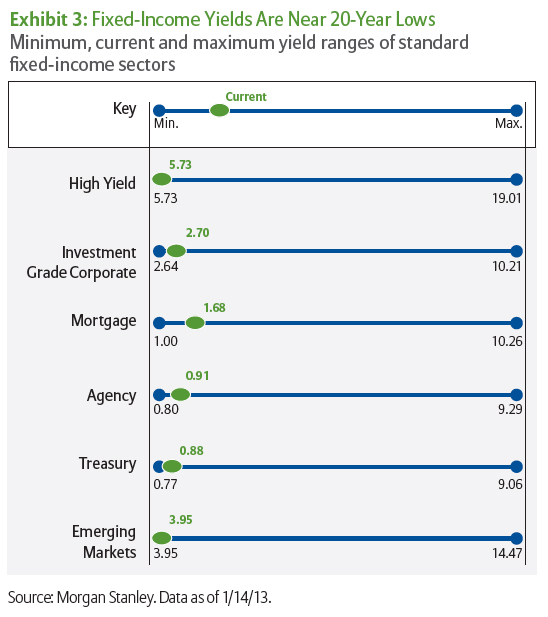

The upshot of this has been an increased focus on yield by individual investors—but as shown in Exhibit 3, every fixed-income asset class is offering yields that are near their 20-year lows. Clearly, Treasury yields have not fallen in a vacuum.

In this context, we see two key questions: Are we coming to the end of the bull market in Treasuries and, if so, what does it mean for other fixed-income sectors? We believe it is time for investors to think about downside protection. As we will demonstrate, investors can reduce their exposure to rising interest rates while still earning an attractive yield by allocating a portion of their portfolios to short-duration high-quality high-yield securities.

Rates could rise as soon as 2013

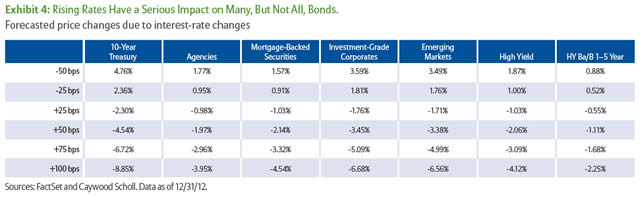

Most Wall Street strategists expect interest rates will finally begin to rise in 2013, with the consensus forecast for a 50-basis-point increase in 10-year Treasury yields this year—reflecting rising inflation expectations brought on by the Federal Reserve’s unconventional monetary policy these past several years. The impact that rising rates will have on the more popular fixed-income sectors is shown in Exhibit 4. Many investors who have stretched for yield by moving out on the Treasury curve will be in for a rude awakening if the consensus forecast proves correct. While the impact of rising rates on bond prices will be felt by most bond investors, it will have a particularly negative effect on those at or near retirement.

Protecting portfolios from rising rates

However, Exhibit 4 also shows that there is one asset class that is expected to hold up well in a rising-rate environment: BB/B high-yield securities maturing inside of five years. Why? These securities’ short durations, their wide spreads to Treasuries and their low risk of near-term default can provide a significant cushion compared with other, more rate-sensitive securities.

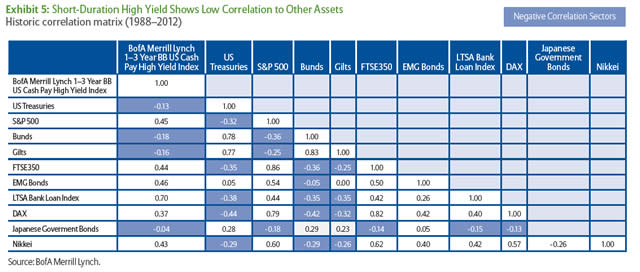

At the same time, focusing on similar securities with less than three-year durations has historically resulted in a portfolio with a negative correlation to global interest rates (see Exhibit 5). Clearly, while owning a high-quality high-yield portfolio concentrated in securities maturing inside of three years results in a slightly less yield compared with a similar portfolio with a slightly longer average life, short-duration yields are still very compelling versus other fixed-income sectors.

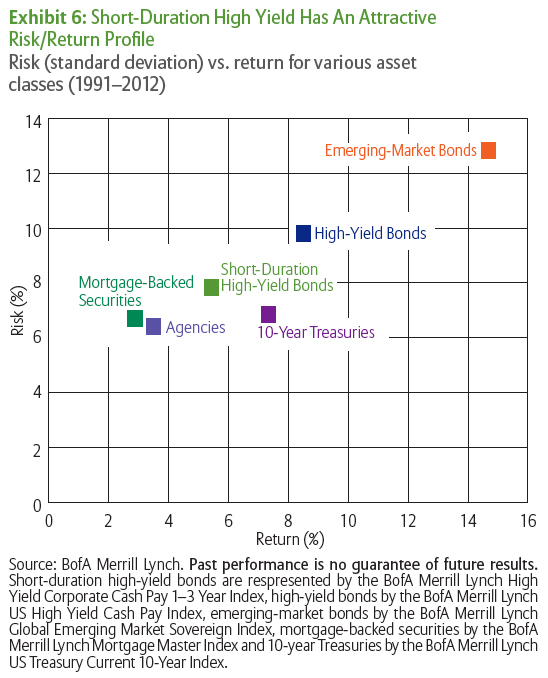

In fact, as Exhibit 6 shows, this short-duration sector of the high-yield market has, over a long time horizon, offered investors very attractive risk-adjusted returns versus emerging market bonds and longer-dated high-yield securities. Accordingly, short-duration high-yield also presents an interesting way to effectively redeploy assets for investors who are worried about overheating markets and think it might be prudent to take some chips off the table.

Conclusion

Investors have enjoyed strong price appreciation in fixed-income assets these past several years—but we have reached the point where the risk/return tradeoff no longer appears to be in the investor’s favor. As a result, we think it is in their best interest to consider paring back exposure to some of the more popular fixed-income sectors and redeploying the proceeds in a diversified portfolio of short-duration high-quality high-yield securities. This action should reduce the expected volatility of the overall portfolio without giving up significant yield.

Eric Scholl and Tom Saake are portfolio manager and managing directors with Allianz Global Investors. They have been working together managing high-yield portfolios since 1992, short-duration high-yield portfolios since 1996 and bank loans since 2005.

A Word About Risk: Bond prices will normally decline as interest rates rise. Equities have tended to be volatile and, unlike bonds, do not offer a fixed rate of return. US government bonds and Treasury bills are guaranteed by the US government and, if held to maturity, offer a fixed rate of return and fixed principal value. High-yield or “junk” bonds have lower credit ratings and involve a greater risk to principal.

This report is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities. The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate.

Past performance is no guarantee of future results. The performance of indexes is not indicative of the past or future performance of any Allianz Global Investors product. Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. It is not possible to invest directly in an index.

Correlation is a statistical measure of how two securities move in relation to each other. Correlation is computed into what is known as the correlation coefficient, which ranges between -1 and +1. Perfect positive correlation (a correlation co-efficient of +1) implies that as one security moves, either up or down, the other security will move in lockstep, in the same direction. Alternatively, perfect negative correlation means that if one security moves in either direction, the security that is perfectly negatively correlated will move by an equal amount in the opposite direction. If the correlation is 0, the movements of the securities are said to have no correlation, it is completely random.

Standard deviation is an absolute measure of volatility measuring dispersion about an average, which, for an index, depicts how widely the returns varied over a certain period of time. The greater the degree of dispersion, the greater the risk.

© 2013 Allianz Global Investors Distributors LLC, 1633 Broadway, New York, NY 10019

AGI-2013-04-03-6445