The investment case for dividend-paying stocks is as strong as ever. Many dividend-paying stocks continue to boast yields comparable to or higher than US Treasurys, and the case for dividend growth in the years ahead remains favorable. Dividends have a long history as a significant component of total return, and investors will likely continue to press for rising payouts since corporate balance sheets are flush with cash. What should investors consider as they survey the universe of dividend-paying companies? Dividend growth in 2012 was robust, even excluding the year’s special and accelerated dividend payments because of correctly anticipated higher 2013 dividend tax rates. We believe 2013 will be another healthy year for dividend growth, although probably not as robust as the mid-teen percentage increases of 2011 and 2012.

The number of dividend-paying companies continues to grow. Managements have been embracing a balanced approach of returning cash to shareholders, combining dividend growth with, in many cases, share repurchases. Of course, companies may sport impressive dividend yields for a number of reasons, and the question of sustainability is critically important. Pursuing yield for the sake of yield can lead to disappointment, particularly if a high dividend payout leads to a weakening of the franchise. A firm’s ability to grow the dividend over time may be more important than a relatively high current dividend yield, particularly if a high dividend indicates limited future growth potential. In our view, investors attracted to dividend-paying companies as a potential source of yield and total return must assess the value of the dividend relative to the strength of the company.

THE ROLE OF DIVIDENDS

Dividends have garnered increased attention in recent years since equity markets have been particularly volatile. Many key equity indices have traded in a wide range, and the S&P 500® Index and Dow Jones Industrial Average have only recently eclipsed previous record highs from 2000 and 2007. Equity returns from capital gains have been, well, choppy. During the bull market of the 1980s and 1990s, many investors and corporate executives adopted a somewhat one-sided view that capital gains were the principal driver of equity returns. The challenging investment environment that has persisted since 2000 has prompted equity market participants to rethink this position.

Historically, dividends have been a crucial contributor to total return. From the end of 1929 through February 2013, reinvested dividends provided almost half of the S&P 500 Index ’s total return. The S&P 500 returned an estimated 9.4% annually with dividends reinvested, compared to only 5.2% annually in price appreciation alone. In dollar terms, the incremental wealth creation from compounding dividends is striking. Hypothetically, a $100 investment made at the end of 1929 would have become $7,061 by February 2013 based on price change only. However, when adding the compounding effect of dividends, the same $100 investment would have become $178,564. The equity value is 25.3 times greater at the end of the period because of the yield component. While the difference between compounding at 9.4% versus compounding at 5.2% on the surface does not appear so dramatic, the mathematical outcome speaks volumes. Examining a more recent, long-term time frame, from the end of 1979 through February 2013, $100 grew into $3,447, compared to $1,403 from price change alone. 1 While a typical investor would face transaction costs, taxes, fees and other withdrawls relegating these results to the hypothetical category, the mathematical impact of compounding dividends becomes a powerful accompanist to a long-term investor.

STOCKS WITH A YIELD ADVANTAGE?

Today, nearly 50% of S&P 500 companies have dividend yields above the 10-year US Treasury note yield. Since 1980, it has been rare for such a high percentage of S&P 500 companies to offer current yields that exceed

the 10-year US Treasury yield. Dividends have grown at a competitive rate over time and are generally more predictable than annual earnings. Managements tend to be reluctant to cut dividends once announced except under significant fundamental challenges or profound strategic shifts. In the past 20 years, dividends have grown at a 4.7% compound annual rate and have only declined twice—from 2000 to 2001 by 5% and 2009 by 21%. In both instances, the decline was due to recessions and dividend growth began again the following year. Since the most recent 2009 decline, dividend growth has resumed aggressively with rates of 16% and 18% in 2011 and 2012, respectively.

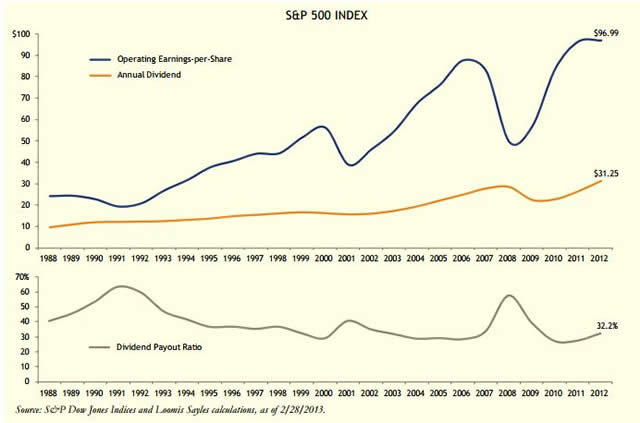

While dividend growth has been impressive recently, dividend payout ratios have been declining because corporate managements have been appropriately influenced by the volatile markets and challenging business conditions of the last 20 years. The dividend payout ratio of operating earnings was 59.3% in 1992 and has declined to only 32.2% in 2012, meaning that companies retained more of their earnings even as dividend payments increased. We believe a dividend payout ratio in the high 30% range, close to the 20-year average, would be reasonable. In the chart below, the volatility of earnings is evident as is the gradual increase in dividend payments and decrease of the dividend payout ratio.

Today, many company managements and investors are rethinking the value of dividends. More than 400 of the S&P 500 companies had a cash dividend at year-end 2012, representing close to 87% of the total index market capitalization. Indicated dividends of S&P 500 companies are about $33.50 compared to the $31.25 paid in 2012. With more dividend increases on tap for 2013, we anticipate high single-digit growth resulting in dividends at the $34.00 level or higher. S&P 500 operating-earnings-per-share growth moderated in 2012 and we expect single-digit earnings growth, on average, in 2013 and 2014. Since we are mid-business cycle, we believe that dividends may grow faster than earnings for the next few years, assuming business conditions remain constructive.

DIVIDENDS APPEAR POISED FOR GROWTH ACROSS SECTORS

Historically, dividend investors may have focused on specific sectors

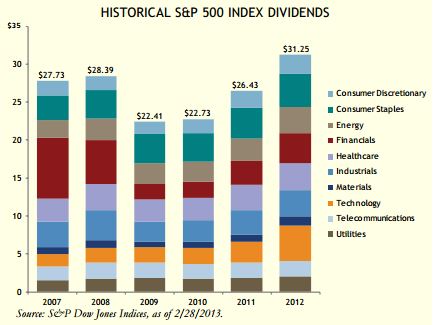

such as financials or utilities. However, we believe viewing the dividend opportunity through this narrow lens distorts the current picture. For example, lower dividends from the financial sector in recent years masked dividend growth in other sectors. Financials, responsible for 29% of S&P 500 dividends near the market peak in 2007, led the most recent decline in S&P 500 dividends, falling from $8.07 in 2008 to just $2.03 in 2009 before

a modest recovery to $3.93 in 2012.

Yet as the chart to the right indicates, a broader survey of the S&P 500 suggests a positive trend in dividend payments has been reestablished. 2012 S&P 500 dividends of $31.25 eclipsed the prior annual record of $28.39 set in 2008, just prior to the financial crisis. Perhaps surprisingly, the technology sector has become the top dividend payer in dollars and cents. Many of the leading large capitalization technology stocks in the Index have come full circle from the late 1990s when dividend payments were viewed as a sign of weakness. Today, many managements embrace the financial discipline required to consistently pay dividends and, obviously, shareholders benefit from receiving cash to help build investment returns.

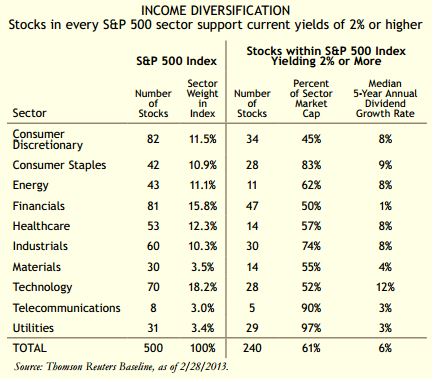

We believe it is possible to build a portfolio of stocks with favorable current income potential that is also diversified across economic sectors. As seen in the chart at above, each of the ten S&P 500 sectors has a material number of stocks yielding 2% 2 or more. These above-average dividend payers represent a fairly large percentage of each sector’s weight in the Index. For example, the consumer discretionary sector holds 82 companies, 34 of which pay a dividend of 2% or greater. These dividend-paying companies constitute 45% of the sector’s weight in the Index. Sectors such as consumer staples, industrials, telecommunications and utilities have a much higher percentage of the sector market capitalization positioned in stocks with yields of 2% or higher. Sixty-one percent of the S&P 500 by market capitalization yields 2% or more.

While an above-average dividend may be attractive to income-oriented investors, dividend growth over time can be more beneficial in generating long-term total return. As shown in the table above, of the 34 higher-yielding stocks within the consumer discretionary sector, the median company had an annual dividend 8% over the past five years. The consumer staples, healthcare and industrials sectors have been among the stronger dividend growers, at 9%, 8% and 8%, respectively. The emerging star of dividend growth is unquestionably the technology sector, boasting a median compound dividend growth rate of 12% over the past five years. As stated above, technology has become the largest dividend paying sector overall; we believe this could continue for a few years since these companies appear to be rethinking capital management policies and favoring dividends as an increasingly important element in the total return equation.NAVIGATING THE UNIVERSE OF DIVIDEND-pAYING COMpANIES

With investors increasingly focused on yield, have dividend-paying stocks become overvalued? There is no simple answer to this question largely because not all dividend-paying stocks are the same. Each company is different, as is its ability to continue to pay or increase its dividend. The universe of dividend-paying stocks is rich and varied, similar to the broad equity market, and needs to be approached in a rigorous manner. If interest rates were to rise dramatically, it would increase the competitiveness of fixed income securities. Our base-case forecast anticipates somewhat higher interest rates over the intermediate term, but not so much of an increase as to make dividend payers less appealing for the long term.

Assessing a company’s ability to continue to pay and grow dividends is a central component of the Loomis Sayles equity research process. Our equity analysts examine a long list of fundamental factors to help determine a dividend outlook. In our view, the strength of a company’s business franchise and consistency of cash flows over time are two of the most important factors. Company managements generally do not want to be in a position of raising a dividend only to reduce it later. As such, companies are often conservative

in setting payout ratios based on the long-term earnings power of the franchise. Other factors integral to a dividend analysis include company balance sheet leverage, merger and acquisition aspirations and, of course, the ability to generate free cash flow over and above that needed for business reinvestment. Smaller, high- growth companies are generally less likely to pay substantial dividends, opting instead to reinvest capital into the company for future growth. More mature companies and those with high free cash flow are often good candidates for healthy dividend payouts.

The analytical challenge of high-dividend-paying companies is determining when the ability to grow a dividend has been curtailed. In our view, companies with strong business models offering competitive dividend yields and an increasing payout rate over time can be among the most compelling equity investments. This can offer the long-term investor an opportunity for strong investment returns from enduring franchises.

1Source: Copyright 2013 Ned Davis Research, Inc. These hypothetical growth examples are provided for illustrative purposes only. They assume dividends and capital gains are reinvested and do not reflect the application of any fees or withdrawals over the entire 84- and 34-year periods, respectively. They do not represent the past or future performance of any Loomis Sayles investment product.Past market experience and returns do not guarantee future results.

2The 2% hurdle rate is a rounded number reflecting the S&P 500 Index dividend yield of 2.11% and the 10-year US Treasury yield of 1.89%, as of 2/28/2013.

Standard & Poor’s 500 (S&P 500®) Index is a registered service mark of McGraw-Hill Companies, Inc.

Copyright 2013 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr. com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/.

Certain other data contained herein is calculated by Ned Davis Research, Inc. (“NDR”) from data proprietary to S&P. Reproduction of data calculated by NDR from S&P proprietary data is prohibited except with prior written permission of NDR and S&P.

The works of authorship contained herein including but not limited to all data, design, text, images, and charts or other data compilations or collective works are owned, except as otherwise expressly stated, by Ned Davis Research, Inc., (“NDR”) or one of its affiliates, Davis, Mendel, Regenstein, or Ned Davis Research Group, or one of their data providers and may not be copied, reproduced, transmitted, displayed, performed, distributed, rented, sublicensed, altered, stored for subsequent use or otherwise used in whole or in part in any manner without the prior written consent of NDR.

Past performance is no guarantee of future results.

Investing in equities involves risks including the risk of loss of principal. Diversification does not ensure future results nor does it guarantee against loss.

Indexes are unmanaged and do not incur fees. It is not possible to invest directly in an index.

This article is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the author only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P., or any portfolio manager. Investment recommendations may be inconsistent with these opinions. There can be no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis do not represent the actual or expected future performance of any investment product. We believe the information, including that obtained from outside sources, to be correct, but we cannot guarantee its accuracy. The information is subject to change at any time without notice.

LS Loomis | Sayles is a trademark of Loomis, Sayles & Company, L.P. registered in the US Patent and Trademark Office.

MALR010325 LEGREV033114

© Loomis Sayles