Hyperactive Monetary Policy: The Good, the Bad and the Ugly

- Hyperactive monetary policy (HMP) is in full force as fiscal policy retreats.

- The benefits of HMP outweigh the costs for now.

- Despite cyclical growth, we will likely not achieve escape velocity and eventually the costs will likely overtake the benefits.

The Fed, along with major global central banks, has taken extraordinary measures to safeguard the financial system and jump-start the global economy. It introduced a zero-interest-rate policy (ZIRP) in December 2008, and has boosted its balance sheet from a mere 5% of GDP to more than 20%. Its policies have morphed from the traditional use of policy rates to aggressive quantitative easing (QE), more explicit communications and, more recently, prioritization of its unemployment mandate over its inflation mandate. What are the net benefits and costs of this hyperactive monetary policy (HMP), and how long should we expect them to last?

We believe HMP will last longer than markets expect with the Fed remaining dovish and experimental as unemployment is likely to remain structurally sticky. For the U.S. in 2013, we forecast headline growth of around 2% with modest inflation of about 2%. We expect fiscal stimulus to retreat, with the deficit narrowing to -5.2% of GDP from -6.9% in 2012, and fiscal uncertainty to abate but the onus to remain on the Fed to keep engaged and support the economy. Nevertheless, despite cyclical growth we will likely not achieve escape velocity and eventually the costs of HMP will likely overtake the benefits.

The Good, the Bad and the Ugly: benefits and costs of HMP

An important question for investors is how the continuation of the Fed’s HMP will affect the real economy and financial assets. Answers can be gleaned by assessing costs and benefits of six channels through which monetary policy works. These are inflation, leverage, the dollar, fiscal adjustment, financial stability and policy uncertainty (see Figure 1).

What stands out is that the benefits and costs of HMP are flip sides of the same coin. For example, fostering risk-taking or “animal spirits” is a positive insofar as it jump-starts a flagging economy, but it’s a negative if too much risk-taking leads to financial instability. Let’s assess each in turn:

Good vs. bad inflation

One of the key benefits of HMP is “good” inflation, which results from the reflation of risk assets. The Fed’s compression of real yields, for instance, has been an important factor driving the S&P 500 past its pre-2008 highs. Home prices also have been rising. Both should be supportive of reflating the economy, even though the wealth effect may be lower than it has been historically due to the debt overhang, blockages in the credit transmission mechanism and the weak labor market.

At the same time, however, inflation is probably the biggest long-term cost of HMP. Even though headline and core CPI remain fairly subdued, in the past money creation has been associated with higher inflation. Pump-priming demand is strongly correlated with inflation when supply and structural factors are the main constraints to growth. HMP may also boost financial demand for commodities, raising production costs and reducing China’s global deflationary impact.

So far the balance of risks is weighted towards good inflation; asset price reflation has helped boost confidence, while rising input prices and commodity bubbles are contained for now.

Leverage: higher cyclical consumption vs. misallocation of capital

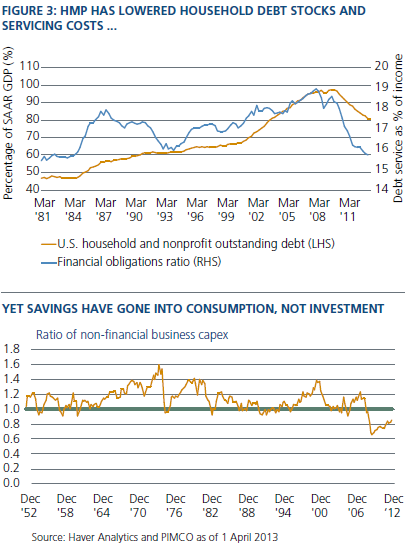

Related to the ability of HMP to generate inflation is the impact of the Fed’s policy on leverage. This works via the impact of inflation and low rates on the real value of the economy’s debt stock, the cost of servicing that debt and the buffer it provides for real adjustment in domestic demand. Debt-stock ratios in the U.S. have come down sharply since the crisis while the debt-service burden for households has reached 30-year lows. The impact on disposable income has been material and helped to mitigate the impact of high unemployment and stagnation in nominal wage growth.

Lower borrowing costs also have meant greater incentives for credit-related growth by corporates and individuals. Yet, so far the evidence suggests that lower borrowing costs have spurred near-term consumption more than long-term investment. It also suggests that savers have been hurt by artificially low returns, which, in turn, disincentivizes long-term capital expenditures by corporates.

Net-net, the impact of HMP on leverage seems to have provided a short-lived boost to demand but, given the misallocation of capital, this is not a foundation for sustained growth.

Impact on the dollar: external competitiveness vs. loss of confidence

The impact of HMP on currencies has gotten significant media attention as a potential devaluation tactic in a global currency war. For the U.S., where exports contribute relatively little to growth, the Fed’s balance sheet expansion has largely been a domestic reflationary tool. Nevertheless, at a time of global QE, HMP has helped on the margin to keep the U.S. competitive. The downside is that the dollar could lose its reserve currency status and face retaliation in the form of capital controls or foreign-exchange (FX) intervention by other central banks.

For now, the risks on the dollar look balanced, with HMP helping U.S. exports and currency retaliation being contained. Moreover, although the amount of dollars held in reserve by nations other than the U.S. has fallen from its peak, dollar holdings remain well above the total of other developed market currencies.

Need for fiscal reform: less appetite for adjustment

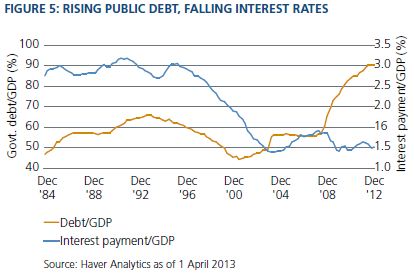

In the first stage of the crisis, the Fed’s ZIRP was the most effective tool in cushioning the economy. Yet even as the focus shifted from crisis containment to fiscal and structural reforms, HMP has remained essential to shore up the economy. The Fed estimates its asset market purchases have helped lower interest rates by one percentage point, which in turn has enabled government spending to be about one percentage point of GDP, all else being equal – a quite significant cushion to real growth in a New Normal environment.

The Fed’s heavy lifting, however, may have reduced the urgency for policymakers to act. The political posturing and negotiations over the debt ceiling in 2011 are an indicator of this.

Financial innovation: jump-starting the economy vs. potential financial instability

One of the initial goals of the Fed’s HMP was to reduce systemic risk after the bankruptcy of Lehman Brothers in September 2008. As the system reset, stability became centered on the “Bernanke put,” the idea that the Fed would do whatever it takes to reflate the economy. This has fostered the return of financial intermediation and innovation, reflected in the pickup of new issuance in all credit sectors.

Still, while easy monetary policy has improved access to capital, an increasingly high percentage of new issuance has been low quality debt (e.g., “covenant lite” loans, which don’t require issuers to meet quarterly standards), which could presage higher default rates and instability.

Policy uncertainty: lower cyclical vs. higher secular policy uncertainty

There is no doubt that the Fed’s actions and forward guidance have gone a long way to reduce cyclical policy uncertainty and lower asset market volatility. However, this has come at the cost of a more challenging exit strategy and the risk that the Fed loses its independence. By the end of 2013, the Fed’s balance sheet will be close to $4 trillion and carry an average duration of six years; a 100 basis point normalization in rates would result in a mark-to-market loss of $240 billion on the Fed’s balance sheet. This sharply increases the risk of political intervention to limit costs or to help Treasury refinancings, for example, by pressure to delay rate hikes.

Taken together, while we expect near-term policy volatility will be contained, higher future political uncertainty will keep medium-term economic volatility high.

Investment implications

Looking at both the benefits and costs, the Fed’s hyperactive monetary policy has helped to boost growth in the short run and backstop the economy from the left-tail risks of the financial crisis. However, this growth has been driven mostly by current consumption and has disincentivized long-term productivity-enhancing capital. On net, it has therefore inhibited the scope of the economy to reach escape velocity in the medium term.

In this environment, interest rate and credit risks are no longer what they used to be. In particular, the term premium of interest rates and credit spreads should compensate not just for current macroeconomic and credit risks, but also for the costs of unwinding hyperactive monetary policies.

In duration space, investors should consider looking for sources of attractive real yields globally and position themselves for higher future inflation.

In credit space, investors should consider not constraining themselves to traditional credit benchmarks, but focus also on rising stars that are investing, delivering and capable of growing earnings even as HMP is unwound.

In currencies, investors should consider focusing on the cleanest dirty shirts in the developed world – those with the strongest balance sheets and current accounts.

Investors globally are enjoying the benefits of HMP. But they also should be prepared for when medium-term costs catch up with the near-term, and short-lived, benefits.

Past performance is not a guarantee or a reliable indicator of future results. Investing in the bond market is subject to certain risks, including market, interest rate, issuer, credit and inflation risk. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Rising stars are securities that have been, or that we believe may be upgraded to investment grade credit quality. The credit quality of a particular security or group of securities does not ensure the stability or safety of the overall portfolio.

Forecasts, estimates, and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fees, and/or other costs. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2013, PIMCO.

© PIMCO

© PIMCO