- The Fed is likely to lag the markets, as they do in most cycles.The markets will probably anticipate the Fed reversing QE.The Fed will surprise few investors.

- The Fed should reverse QE in a yield curve-neutral way, in our view.Steepening the curve risks perversely stimulating the economy by making carry trades and loan spreads more profitable.

- This cycle will probably end as do most cycles. The Fed will be behind the curve, play catch-up, tighten too much, invert the curve, and cause a recession.That end result, however, is probably quite far in the future.

The Fed has clearly raised the issue of reversing their policy of quantitative easing, and investors have become more anxious.However, one should remember that the Fed is generally a lagging indicator, and that a tightening of monetary policy is unlikely so long as the overall economic growth and inflation remain anemic.

Investors also seem to be missing the basic point that their own high levels of anxiety are one of the reasons the Fed is unlikely to begin reversing policy anytime soon.The Fed doesn’t want to prematurely tighten monetary policy which might cause the financial markets to quickly reverse, the cost of capital to simultaneously rise, and investor and business confidence to rapidly decrease.

History suggests that changes to monetary policy lag most cycles, and instances during which the Fed negatively shocked the markets have been rare.The economy will dictate policy to the Fed, and our guess is that the Fed will eventually tighten only when a strong and broad consensus forms that the economy can withstand a tightening cycle.That surely doesn’t seem to be the case today.

The Fed historically lags the markets

It is somewhat curious that investors think the Fed is a leading indicator because history demonstrates that the Fed is typically a lagging indicator.It makes sense that the Fed is a lagging indicator because they focus primarily on inflation and the unemployment rate.Both inflation and the unemployment rate are classic lagging indicators of the US economy.

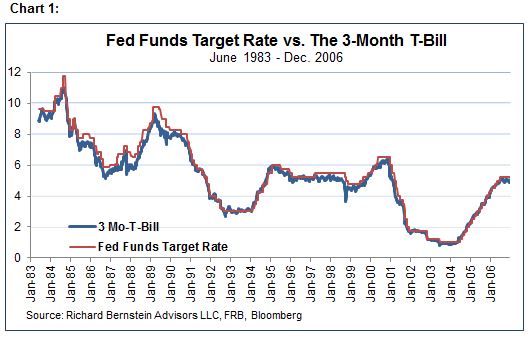

Chart 1 shows the historical relationship between the Fed Funds target rate and the three-month t-bill rate for the roughly twenty-five year period prior to the recent credit bubble.The three-month bill rate generally led the target rate demonstrating that the markets are generally ahead of the Fed with respect to the tightening or easing of monetary policy.

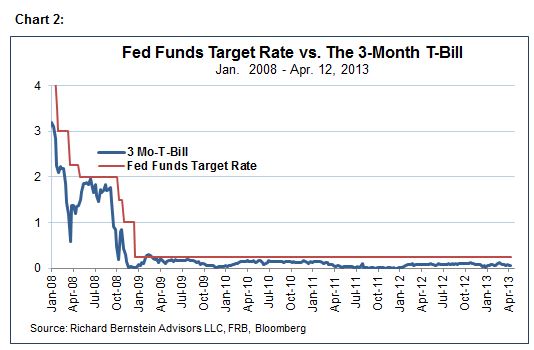

Chart 2 shows the current relationship between the 3-month bill rate and the Fed Funds target.The bill rate has not meaningfully increased, which argues that short-term interest rates, at least, are not set to rise.If the bill rate were to start meaningfully increasing, it might signal a significant change in monetary policy at the short end of the yield curve.

Extricating from QE and the possible unexpected results

Investors should consider two aspects to the Fed unwinding quantitative easing.First, will the central bank lead or lag the economy.In other words, will they anticipate sustainable growth or will they react to it?The analysis above and the Fed’s own statements suggest that Fed policy, whether at the short-end or long-end of the yield curve, are likely to lag the cycle.

If the Fed’s policies will indeed be reactive, then the markets will give plenty of warning that a tightening of policy at the long end of the curve might occur.As mentioned, a consensus will likely form that the Fed is “behind the curve”.

Second, investors should consider how the unwinding QE might affect the overall economy.In this respect, the thinking so far seems somewhat naïve to us.Most investors, and we believe the Fed itself, believe that the economy will necessarily slow if the Fed begins to reverse QE by selling longer-dated bonds and steepening the yield curve.We think it is more likely that the Fed might perversely stimulate the economy by improving the profitability on loans and carry trades.The combination of improved business confidence and improved lending margins seems likely to stimulate the economy rather than slow it.

Playing catch-up once again to the inevitable end story

The Fed believes that reversing QE will slow the economy.However, a steeping yield curve and stronger business confidence argue otherwise.If we are correct, then the Fed could once again be forced to play catch-up to the markets during the mid- and late-cycle.

As most cycles mature, the Fed typically realizes that their policies have been too accommodative for the maturity of the cycle.Production bottlenecks and shortages become more frequent, and inflation pressures begin to build.The Fed then rushes to tighten monetary policy in an attempt to make up for the earlier hesitancy to tighten.The traditional end result has been that the Fed’s late-cycle aggressive policies go to far (i.e., they over-tighten policy), the yield curve inverts, and a recession follows.

This cycle seems poised to follow that historical pattern.The Fed remains fearful of tightening too early and has told investors that they will react to the economy’s strength.Their reaction time will probably be slow as well.If our contention that reversing QE might stimulate the economy is correct, then the frequency and magnitude of Fed tightening is likely to accelerate as they realize they’ve created a monster.Their rush to equalize monetary policy with the strength in the economy could lead them to over-tighten and invert the yield curve.A recession would probably follow, and the cycle would end in a very traditional manner.

Near-term investors seem overly worried.When it’s time to worry, they’ll likely be complacent.

Our sentiment work indicates that investors seem too worried about the near-term effects of a tightening of monetary policy.However, we think the Fed will be slow to tighten, and we’re not sure their tightening efforts will succeed.We anticipate, however, that investors’ fears today will morph into confidence which will, in turn, transform into the overconfidence that characterizes every late-cycle environment.

Investors generally ignore the warning signals of inverted yield curves.Instead of following the powerful historical signal, they get caught up in the bullish moment.Late-2006/early-2007 was the last example.

This cycle’s construction has been different, but most cycle’s constructions are unique.Was the 1982 bull market, with massive and unprecedented interest rate cuts constructed any more unusually than today’s bull market?Was the 1991 bull market in the aftermath of the S&L crisis and the RTC constructed any more unusually than today’s bull market?As we’ve pointed out many times, fear and indecision are the cornerstones of bull markets, and it is certainly the cornerstone of the present one.

Will this bull market end any differently than have other bull markets?We doubt it.

When the curve inverts and the consensus is that the inversion doesn’t matter, that’s probably when investors should worry.Until that occurs, we think it will ultimately pay to be bullish.

© Copyright 2013 Richard Bernstein Advisors LLC. All rights reserved.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in, any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Specifically, and without limiting the generality of the foregoing, before acquiring the shares of any mutual fund, it is your responsibility to read the fund’s prospectus. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is an inherently risky activity, and investors must always be prepared to potentially lose some or all of an investment's value. Past performance is, of course, no guarantee of future results.

© Richard Bernstein Advisors