The phrase “Great Rotation” has come to mean a sizeable shift in asset allocations from bonds to stocks.We, too, believe that stocks are likely to secularly outperform bonds, but we don’t think that is the “great rotation” about which investors should be concerned.

The most important structural investment decision facing investors is not stock/bond allocation, in our view.Rather, the REAL “great rotation” is likely to be a shift from non-US assets to US assets.Asset performance seems to be well underway, yet most investors appear totally oblivious.

We remain bullish on US equities, but continue to have concerns about emerging market (EM) equities and about non-EM companies whose growth strategies focus on the emerging markets.The standard warning signals of a bull market’s end seem nowhere in sight in the US.The Fed isn’t close to tightening too much, investors’ constant uncertainty and lack of confidence regarding the stock market suggests attractive risk premiums and good value, and there is hardly euphoria for US equities.

However, it remains startling to us that investors still seem enamored with the emerging markets despite that EM stocks have underperformed US stocks for more than five years, and that EM profit fundamentals continue to be among the weakest in the world (almost 60% of EM companies recently reported negative earnings surprises).The US is even becoming a better growth story than the emerging markets.Smaller capitalization US companies are projected to grow earnings 60% faster than are EM companies (35% versus 14% for the next twelve months).

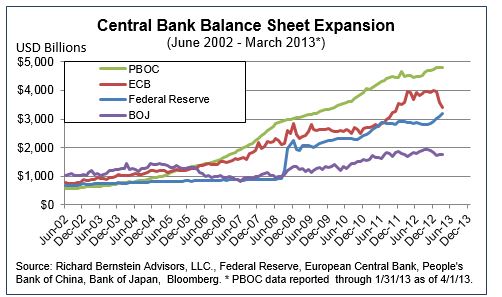

In addition, many of the major emerging markets have serious monetary problems that make the US situation look rather amateurish.India now has the highest inflation rate among emerging and developed markets and their central bank has actually been easing monetary policy.Brazil’s President recently stated that stimulating growth was more important than was controlling inflation despite disturbing inflation trends and lack of productivity within Brazil.China’s lending policies have been so out of control that the balance sheet of the People’s Bank of China is now roughly 50% bigger than the Fed’s (see Chart 1).

Chart 1:

A defensive equity rotation?

There has been considerable commentary recently regarding a “defensive rotation” within the equity market.Defensive sectors, such as Consumer Staples, Health Care, and Utilities, were the best performing S&P 500®sectors during the first quarter.Some observers believe that the outperformance of these defensive sectors suggests that the economy is slowing down and that the bull market is nearing an end.

We think last quarter’s defensive rotation within the S&P 500®points more to the problems larger multi-national companies are having because of the stronger US dollar and economic weakness abroad than to looming deterioration in the US.

As one looks beyond the S&P 500® toward more domestically-oriented universes, the defensive rotation dissipates.In other words, the defensive rotation was most widespread among global companies, and less prevalent among domestic companies.

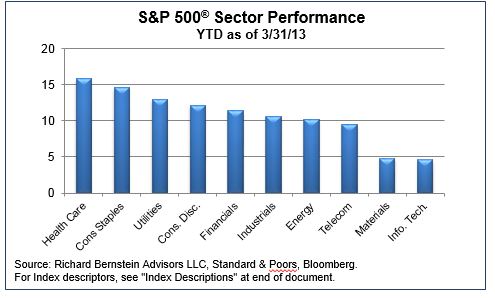

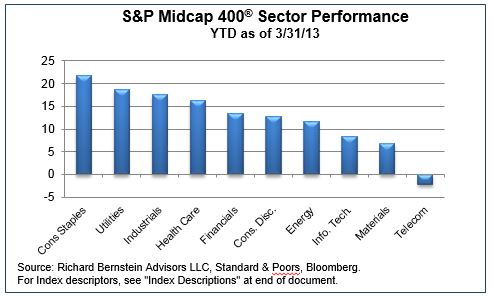

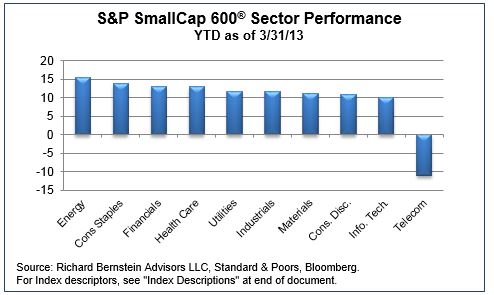

The following three charts show first quarter sector performance for the S&P 500®, the S&P MidCap 400®, and the S&PSmallCap 600®.The S&P 500®companies generally have more foreign exposure than do the S&PMidCap 400®companies, which in turn have more foreign exposure than do the companies within the S&PSmallCap 600®.

Chart 2 shows the performance for the S&P 500®companies is indeed quite defensive.The best performing sectors in the first quarter were Health Care, Consumer Staples, and Utilities, all of which are classic defensive sectors.They are closely followed, however, by early-cycle sectors (Consumer Discretionary and Financials), which also outperformed the overall market.

Chart 3 shows sector performance for the S&PMidCap 400®universe.Again, this universe is more domestically-oriented than is the S&P 500®, which is dominated by larger, multi-national companies.Consumer Staples and Utilities did lead mid cap companies during the first quarter, but note that Industrials crept up to third place ahead of Health Care.Thus,cyclicals performed a bit better among mid cap stocks than among larger caps.

Chart 4 depicts sector performance for the S&PSmallCap 600®universe.This universe is incrementally more domestic than the S&PMidCap 400®universe, and is considerably more domestic than is the S&P 500®.Incrementally domestic sector performance again had an incrementally more cyclical bent to it.The best performing sector was Energy, and Financials ranked third.

Technology was among the worst performing sectors regardless of size.Technology is historically the most foreign exposed sector, and the sector’s consistently poor relative ranking regardless of size might similarly reflect concerns regarding non-US growth.

We are not trying to overstate our case.Clearly, first quarter sector performance was less cyclical than was that in the prior quarter.However, we think a closer inspection of the data suggests that equity investors’ fears might not be US-focused.

Chart 2:

Chart 3:

Chart 4:

Global asset performance supported the REAL “great rotation”

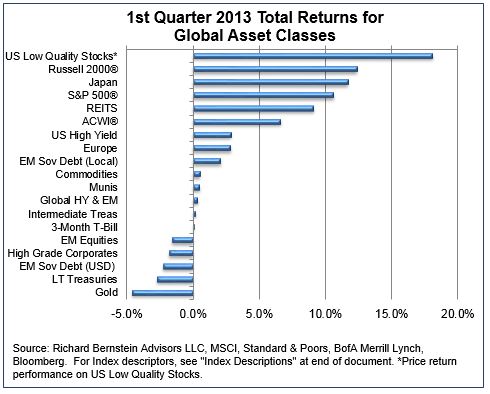

Global asset class performance during the first quarter seemed to support our notion of the REAL “great rotation”.Chart 5 shows first quarter performance for a broad range of global asset classes.Interesting, the best performers were US low quality stocks, which tend to be the most economically sensitive group of stocks within the US market.Smaller stocks, here depicted by the Russell 2000®Index, finished second.

It is hard for us to see how the market is forecasting that US economy is in jeopardy when the stocks that are typically the most sensitive to the domestic economy, namely lower quality and smaller stocks, led global asset performance.By contrast, EM equities, those perhaps most sensitive to the global economy, finished toward the bottom of the performance derby.

The same performance comparison was evident within the global debt markets.US high yield outperformed EM debt both in local currency and in US dollars.If the outlook for the US economy was indeed worse than that for the global economy, then one would expect economically-sensitive US bonds (i.e., US high yield) to underperform bonds more sensitive to the global economy (i.e., EM debt).

Moreover, if the US economy were indeed going to materially weaken, one wouldn’t expect to see long-term US treasury bonds near the bottom of the list.The performance comparison between lower quality stocks, smaller company stocks, high yield bonds, and treasuries is rather startling given the consensus view that the US economy is teetering on the brink of another recession.

Chart 6:

The REAL “great rotation” continues

US stocks have been outperforming emerging market stocks for more than five years.Yet, few investors seem to recognize that a “great rotation” is underway from global equities to US equities.In some cases, the US is even a better growth story than are the emerging markets.

The consensus seems to be that the US economy is on the brink of a serious slowdown.However, both asset class performance during the first quarter and US sector performance among domestically-focused companies do not support that consensus view.It is true that defensive stocks led larger capitalization US performance, but that performance appears to be tied to larger companies’ exposure to Europe and emerging markets.

The REAL “great rotation” seems intact and on-going.

© Copyright 2013 Richard Bernstein Advisors LLC. All rights reserved.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in, any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Specifically, and without limiting the generality of the foregoing, before acquiring the shares of any mutual fund, it is your responsibility to read the fund’s prospectus. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is an inherently risky activity, and investors must always be prepared to potentially lose some or all of an investment's value. Past performance is, of course, no guarantee of future results.

© Richard Bernstein Advisors