Taper

If SNL’s Emily Litella worked on Wall Street, she’d probably be asking “What’s all this hubbub about the Fed’s tapir? After all, it’s a fine animal that never hurt anyone on Wall Street.” It would then be pointed out to her that the word was “taper” and not “tapir”. She would politely end her commentary with her famous “Never mind.”

Indeed, it appears to us that investors should take the advice of Gilda Radner’s character to heart. Never mind the taper. A comparison of historical and current fundamentals suggests investors are overly apprehensive regarding the Fed’s taper of quantitative easing.

History repeats

As we have previously written(see hyperlinkhere),the Fed is generally a lagging indicator. Rather than setting monetary policy proactively, the Fed tends to react to the economy.The Fed’s dual mandate is based on monitoring two decidedly lagging indicators, unemployment and inflation, and history clearly shows that the markets tend to be well ahead of the Fed.

The Fed has repeatedly emphasized to investors that its actions in the current cycle will lag the economic data, and that they will tapir – sorry, taper –monetary stimulus as the economy strengthens.We interpret that to mean that because of the severity of the last recession and the on-going deflationary forces within the global economy, the Fed will be happy to lag the economy by even longer than might be normal.

It serves no purpose for the Fed to prematurely reverse their monetary stimulus.The markets’ recent negative reaction at the hint of the Fed reversing policy is a warning that the Fed is unlikely to ignore.The Fed surely already understands that reversing course when the economy is not robust could ruin everything they have accomplished so far.

We still think the Fed will eventually be so slow to tighten that the consensus will be that the Fed is late by the time the Fed actually does reverse course.

The current issue

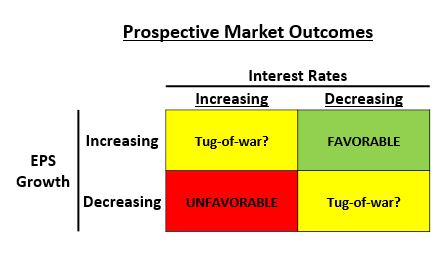

The current market environment can more easily be understood if one examines the relationship between the two main drivers of equity valuation: interest rates and earnings.The matrix below highlights that the combination of falling interest rates and rising earnings growth is generally a good one for equities, and that the opposite combination of rising interest rates and decreasing earnings growth is generally a poor one.Investors usually find it more difficult to assess the outlook for equities in the other two quadrants of the matrix because there is often a battle between the positive effect of one variable and the negative effect of the other.

The past couple of years has been an example of the tug-of-war in the lower right quadrant.The profits cycle has been decelerating since June 2010, but the stock market has nonetheless risen because the positive effects of QE and the accompanying lower interest rates have been more powerful than has been the slowdown in earnings growth.

The recent stock market volatility seems to indicate investors have become fearful that the combination in the lower left quadrant will occur, i.e., the possibility of continued slowing profits growth coupled with increasing interest rates as the Fed reverses QE.

However, we continue to believe that the probability of the combination of the Fed tightening monetary policy and deteriorating fundamentals is extremely low.Rather, we think investors should ultimately be prepared for the exact opposite. It seems more likely that the Fed will eventually be too slow to tighten policy despite a booming economy than prematurely abort the economic recovery.

The wall of worry now includes the fuss over the Fed

The wall of worry continues, as it does through most bull markets.One can now add the Fed prematurely tightening monetary policy to the long list of worries like a double-dip recession, a weak banking system, imminent inflation, the dollar falling, the over-indebted household sector, government deficits, European growth, and emerging market instability.

Bull markets tend to end when investors are certain, and not when there is considerable uncertainty.Certainty and investors’ total confidence in the stock market will eventually return, as it does at all bull market peaks.We’d argue such cycle-ending certainty does not exist today.

So, what’s all this talk about the Fed’s taper?Never mind.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

© Copyright 2013 Richard Bernstein Advisors LLC. All rights reserved.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in, any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Specifically, and without limiting the generality of the foregoing, before acquiring the shares of any mutual fund, it is your responsibility to read the fund’s prospectus. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is an inherently risky activity, and investors must always be prepared to potentially lose some or all of an investment's value. Past performance is, of course, no guarantee of future results.

© Richard Bernstein Advisors